Introduction

Many people in the United States visit urgent care centers when they need quick medical help but do not want to go to the emergency room. But one big question often comes up: how much does an urgent care visit cost without insurance?

This topic matters because medical bills can be stressful, especially if you do not have health coverage. Knowing the possible costs ahead of time helps you plan, avoid surprises, and make smarter decisions about your health and your budget.

In this guide, you will learn what urgent care is, how pricing works, real-life cost examples, common mistakes people make, and practical tips to manage expenses without insurance.

What is an Urgent Care Visit Cost Without Insurance?

An urgent care visit cost without insurance refers to the amount you pay out of pocket when you receive treatment at an urgent care clinic and do not have health insurance coverage.

Urgent care centers treat medical problems that need quick attention but are not life-threatening.

Common reasons people visit urgent care include:

- Minor infections

- Fever or flu symptoms

- Sprains or small fractures

- Cuts that may need stitches

- Ear or throat pain

- Mild allergic reactions

Without insurance, you pay the full price yourself instead of sharing the cost with an insurance company.

Typical base visit costs usually include:

- Check-in and evaluation

- Examination by a healthcare provider

- Basic medical advice or treatment

However, extra services like X-rays or lab tests often cost more.

Do You Know What Is How Long Does It Take to Insure a Car?

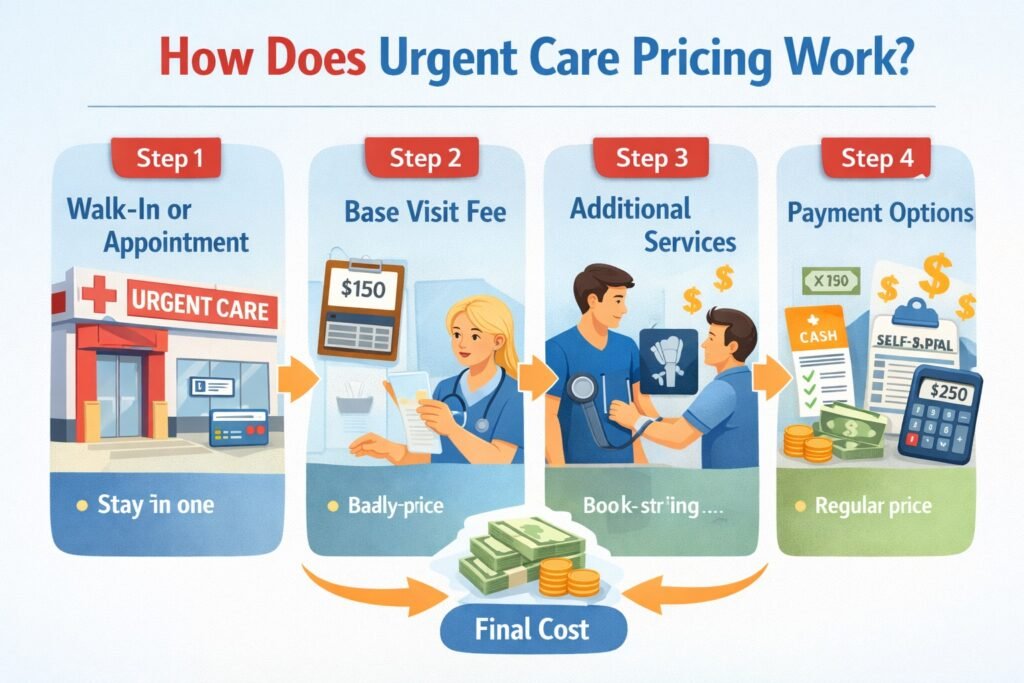

How Does Urgent Care Pricing Work?

Understanding how urgent care pricing works can help you avoid confusion when you receive a bill.

Here is a simple step-by-step explanation:

Step 1: Walk-In or Appointment

Most urgent care clinics allow walk-ins. When you arrive, staff will ask for identification and payment information. If you do not have insurance, they usually explain self-pay pricing.

Step 2: Base Visit Fee

You pay a standard visit fee. This covers:

- Medical evaluation

- Basic diagnosis

- Provider consultation

This fee often ranges between $100 and $200 depending on location.

Step 3: Additional Services

If your condition needs more care, extra charges may apply, such as:

- Lab testing

- Blood work

- X-rays

- Medications given at the clinic

- Procedures like stitches or splints

Each service adds to the total bill.

Step 4: Payment Options

Many urgent care centers require payment the same day. Some clinics offer:

- Upfront discounts

- Self-pay packages

- Payment plans

Step 5: Final Cost

Your total cost depends on:

- The treatment you receive

- Clinic pricing

- City or state

- Complexity of care

Real-Life Example

Let’s look at a realistic situation to understand costs better.

Example 1: Simple Illness Visit

Sarah develops a sore throat and fever. She visits urgent care without insurance.

Her bill may look like this:

- Base visit fee: $140

- Strep throat test: $35

- Prescription (pharmacy cost separate): $15

Total urgent care cost: about $175

Example 2: Minor Injury

Mike twists his ankle while playing sports.

His visit includes:

- Evaluation fee: $160

- X-ray: $120

- Ankle wrap and support: $30

Total cost: around $310

Example 3: Cut Requiring Stitches

A child gets a deep cut needing stitches.

Possible charges:

- Visit fee: $150

- Procedure (stitches): $180

- Supplies and cleaning: $40

Total cost: about $370

These examples show that costs vary widely depending on treatment needs.

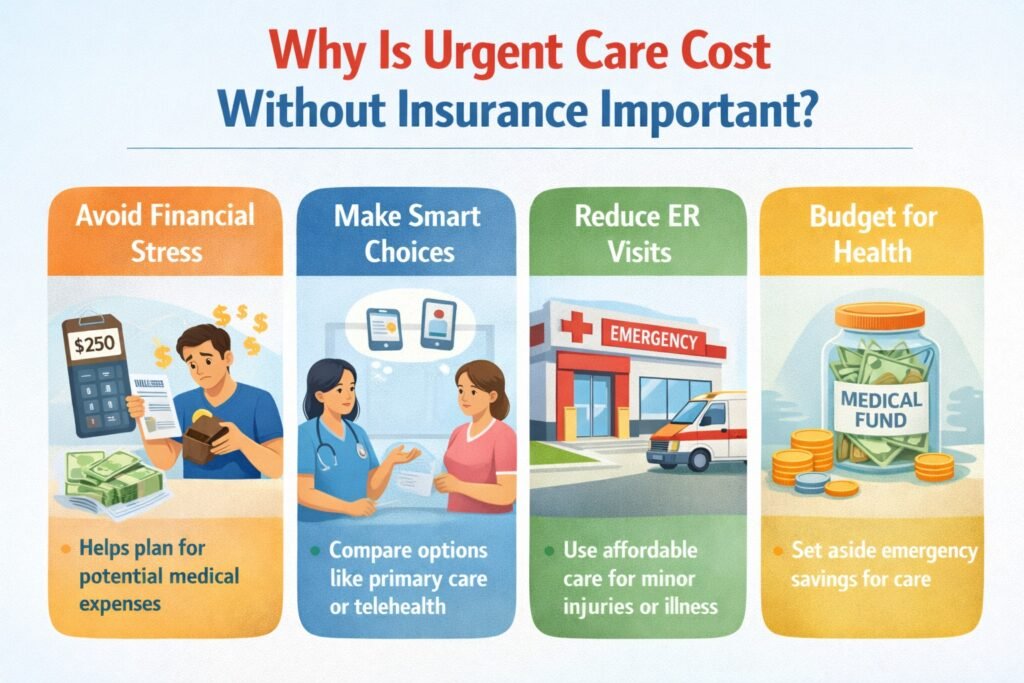

Why Is Urgent Care Cost Without Insurance Important?

Table of Contents

Table of Contents

Understanding costs before visiting urgent care can make a big difference in your financial planning.

Here’s why it matters:

Helps Avoid Financial Stress

Unexpected medical bills can cause anxiety. Knowing average prices helps you prepare.

Supports Better Healthcare Choices

You can compare urgent care with other options like primary care clinics or telehealth services.

Prevents Emergency Room Overuse

Emergency rooms are much more expensive. Urgent care is often a safer financial choice for minor issues.

Encourages Early Treatment

When people understand pricing, they are more likely to seek treatment early instead of waiting until a problem worsens.

Improves Budget Planning

Families without insurance can set aside emergency savings for medical needs.

Average Urgent Care Costs by State (Without Insurance)

One of the biggest factors affecting urgent care pricing is location. Healthcare costs vary significantly across the United States due to differences in rent, wages, state regulations, and demand.

Here’s a general idea of how pricing may differ:

High-Cost States

States like:

- California

- New York

- Massachusetts

- Washington

Self-pay urgent care visits may range from $150 to $300+ for a basic visit, before additional services.

Mid-Range Cost States

States such as:

- Texas

- Florida

- Arizona

- Illinois

Typical base visits may fall between $110 and $220.

Lower-Cost States

In some Midwest or Southern states:

- Arkansas

- Oklahoma

- Alabama

- Kansas

Base visit fees may start closer to $90–$150.

Keep in mind: these are general estimates. Individual clinic pricing may vary.

Urgent Care vs Emergency Room: A Detailed Cost Comparison

Many uninsured patients struggle with this decision: urgent care or ER?

Here’s a clearer breakdown:

| Service Type | Average Cost Without Insurance |

|---|---|

| Urgent Care (basic visit) | $100–$250 |

| Urgent Care with X-ray | $250–$400 |

| Emergency Room (minor issue) | $1,000–$2,500+ |

| Emergency Room (with tests) | $2,000–$5,000+ |

Emergency rooms charge facility fees, specialist fees, and hospital overhead — even for minor conditions.

Urgent care centers are typically privately owned clinics with lower operating costs, which helps keep prices down.

Rule of thumb:

If the condition is not life-threatening, urgent care is usually the more affordable option.

Telehealth vs Urgent Care Without Insurance

Telehealth services have grown significantly in recent years. For uninsured patients, this can be a cost-saving alternative.

Telehealth Cost (Without Insurance)

- $40–$90 per visit (average range)

Telehealth is ideal for:

- Minor infections

- Cold and flu symptoms

- Skin rashes

- Prescription refills

- Allergies

However, telehealth cannot perform:

- X-rays

- Blood tests

- Physical procedures

- Stitches

If your issue may require imaging or hands-on treatment, urgent care is more appropriate.

How to Reduce Urgent Care Costs Without Insurance

If you don’t have health insurance, there are still ways to lower your medical expenses.

1. Ask for Self-Pay Pricing

Many clinics offer discounted “self-pay” rates. Some even publish flat fees on their website.

Always ask:

“What is your self-pay rate for today’s visit?”

2. Request an Itemized Estimat

Before agreeing to additional services, ask:

- How much will this test cost?

- Is this procedure necessary today?

- Are there alternative options?

Transparency helps you avoid surprise bills.

3. Use Community Health Clinics

Federally Qualified Health Centers (FQHCs) offer care based on income.

They may provide:

- Sliding-scale fees

- Lower-cost prescriptions

- Basic lab work

These clinics can be significantly cheaper than urgent care.

4. Compare Clinics Online

Search:

“urgent care self pay cost near me”

Some clinics advertise transparent pricing.

Prices can vary by $50–$200 in the same city.

5. Consider Discount Medical Plans

Medical discount programs are not insurance, but they may provide reduced rates at participating clinics for a monthly membership fee.

This may be helpful if you expect multiple visits per year.

Prescription Costs After Urgent Care

Many patients forget that urgent care bills are only part of the expense.

Prescription medications can add:

- $10–$30 for generic antibiotics

- $40–$100+ for brand-name drugs

- $100+ for specialty medications

To save money:

- Ask for generic versions

- Use pharmacy discount apps

- Compare prices between pharmacies

Sometimes one pharmacy may charge significantly less than another.

Payment Plans and Financial Assistance

If you cannot pay the full bill upfront, ask the clinic:

- Do you offer payment plans?

- Can I split payments over 3–6 months?

- Are there hardship discounts?

Some clinics partner with third-party financing services.

Never ignore a bill — communication is key.

When Urgent Care Is NOT the Best Financial Choice

Even though urgent care is cheaper than ER visits, it may not always be the lowest-cost option.

Situations where urgent care may not be ideal:

- Routine physical exams

- Ongoing chronic condition management

- Preventive screenings

- Vaccinations

Primary care providers often charge less for scheduled visits.

If you do not have insurance, building a relationship with a local primary care clinic can reduce long-term costs.

Hidden Costs People Don’t Consider

Many uninsured patients only think about the base visit fee. However, other costs may include:

- Follow-up appointments

- Repeat lab testing

- Specialist referrals

- Physical therapy

- Additional imaging

For example:

A simple ankle sprain may require:

- Initial urgent care visit

- Follow-up X-ray

- Orthopedic consultation

Total cost can exceed $600–$1,000 without insurance.

Planning for possible follow-up care is important.

Is It Worth Getting Health Insurance to Avoid Urgent Care Costs?

If you frequently need medical care, insurance may actually save you money.

Consider:

- How often you visit clinics

- Whether you take regular medications

- Your risk for accidents or chronic illness

Even a basic marketplace plan may reduce urgent care copays to $30–$75 instead of $200+.

However, if you rarely use medical services, self-pay urgent care may be manageable.

This depends on your personal risk tolerance and financial situati

Preventive Care Can Reduce Urgent Care Visits

Many urgent care visits happen due to preventable issues.

Here are ways to reduce visits:

- Stay updated on vaccinations

- Practice safe sports habits

- Maintain regular health checkups

- Address minor symptoms early

- Keep a basic first-aid kit at home

Small preventive actions can save hundreds of dollars.

How Employers and Membership Clinics Can Help

Some employers offer:

- On-site clinics

- Direct primary care memberships

- Discounted urgent care partnerships

Direct Primary Care (DPC) memberships typically cost:

- $50–$100 per month

These memberships often include:

- Unlimited primary visits

- Discounted labs

- Lower urgent care referrals

This can be valuable for families without traditional insurance.

Red Flags to Watch Out For

Not all urgent care centers operate the same way.

Watch for:

- Lack of transparent pricing

- Pressure to accept unnecessary tests

- Vague billing explanations

- High “facility fees”

Choose clinics with:

- Clear pricing policies

- Good online reviews

- Professional staff

Being informed protects your finances

Long-Term Financial Planning for Medical Expenses

If you are uninsured, consider creating a small medical emergency fund.

Suggested goal:

- $500–$1,000 set aside for urgent health needs

Even saving $20–$50 per month can build a cushion.

Unexpected medical bills are one of the top causes of financial stress in the U.S. Preparing in advance reduces anxiety.

Key Takeaways for U.S. Patients

- Basic urgent care visits typically cost $100–$250 without insurance.

- Additional services increase total costs quickly.

- Urgent care is far cheaper than emergency rooms for non-life-threatening conditions.

- Telehealth may be the most affordable option for minor issues.

- Always ask about pricing before treatment.

- Compare clinics in your area.

- Consider payment plans if needed.

Being proactive and asking questions can save you hundreds of dollars.

Final Expert Advice

As someone experienced in insurance and healthcare cost structures, here’s the most important advice:

- Never ignore symptoms that may become serious.

- Choose the appropriate level of care.

- Ask about pricing before agreeing to services.

- Consider insurance if you frequently need care.

- Plan financially for unexpected health needs.

Healthcare costs in the U.S. can be complex, but with preparation and knowledge, you can make informed decisions that protect both your health and your budget.

Understanding Why Urgent Care Prices Vary So Much

One of the most confusing parts of paying for urgent care without insurance is the wide price difference between clinics. Two facilities located just a few miles apart may charge very different rates for the same service. This happens because urgent care centers are privately operated businesses. Each clinic sets its own pricing structure based on overhead costs, staffing, equipment, and local competition.

For example, clinics located near major hospitals or in busy urban centers often have higher operating costs. Rent, staff wages, and medical equipment expenses directly affect what patients pay. In smaller suburban or rural areas, pricing may be slightly lower.

Before choosing a clinic, it can be helpful to check their website or call ahead and ask about self-pay rates. A five-minute phone call may save you a significant amount of money.

The Role of Facility Fees

Some urgent care centers charge what is called a “facility fee.” This is an additional charge for using the clinic’s medical space and equipment. Not every urgent care clinic charges this fee, but when they do, it can increase your bill noticeably.

If you see a higher-than-expected total, ask for a detailed breakdown. Understanding each charge allows you to identify what you are actually paying for and ensures there are no billing errors.

How Medical Complexity Impacts Cost

The more complex your condition, the higher the cost is likely to be. A simple sore throat evaluation will cost much less than a visit requiring imaging, injections, or procedures.

Healthcare providers must consider:

- Time spent evaluating you

- Medical supplies used

- Diagnostic tools required

- Risk level of your condition

If your case requires additional monitoring or treatment, it naturally increases the clinic’s resources, which raises the bill.

Weekend and After-Hours Pricing

Some urgent care clinics extend their hours into evenings and weekends. While this convenience is helpful, certain clinics may charge slightly higher rates for extended-hour services.

If your condition can safely wait until standard business hours, you may want to compare pricing options.

The Financial Impact of Repeat Visits

A common financial challenge for uninsured patients is repeat visits. If symptoms do not improve, you may need to return for follow-up care. Without insurance, each visit is another out-of-pocket expense.

To reduce repeat visits:

- Carefully follow discharge instructions

- Complete prescribed medications

- Monitor symptoms closely

- Schedule follow-up care only when medically necessary

Taking recovery instructions seriously can prevent additional expenses.

Children’s Urgent Care Costs

Parents often worry about urgent care expenses for children. Pediatric urgent care pricing is generally similar to adult visits, but some specialized pediatric centers may charge slightly more due to child-specific equipment and staffing.

If your child frequently needs care, it may be worth researching family health coverage options to reduce long-term costs.

Can Urgent Care Send Bills to Collections?

If a medical bill goes unpaid for a long period, it may eventually be sent to collections. This can negatively impact your credit score.

If you are unable to pay the full amount immediately:

- Contact the billing department

- Request a payment plan

- Explain your financial situation

Most clinics prefer structured payments over unpaid balances.

The Importance of Cost Transparency in Healthcare

Healthcare pricing transparency has become more important in recent years. Patients are increasingly encouraged to ask questions about cost before receiving services.

As a patient without insurance, you have the right to ask:

- What will this cost today?

- Are there lower-cost treatment options?

- Is this test absolutely necessary?

Clear communication protects your finances and ensures informed medical decisions.

Planning Ahead for Seasonal Illnesses

Certain times of year, such as flu season, see a rise in urgent care visits. If you know that seasonal illnesses affect your household regularly, planning ahead financially can reduce stress.

Consider setting aside funds during low-expense months so you are prepared when medical needs arise.

When Urgent Care May Actually Save You Money

While medical expenses can feel overwhelming, urgent care often prevents larger bills down the road. Early treatment of infections, minor injuries, or illnesses can stop complications from developing.

Delaying care to avoid a $150 bill could lead to a hospital visit costing thousands. Seeking timely care may be the more financially responsible decision in the long run.

Final Thoughts on Managing Urgent Care Costs Without Insurance

Navigating healthcare without insurance requires awareness, planning, and proactive communication. While urgent care visits are not free, they remain one of the more affordable medical options for non-emergency situations in the United States.

The key is to:

- Compare prices

- Ask questions

- Understand services before agreeing

- Prepare financially for unexpected care

When you approach urgent care with knowledge and preparation, you can reduce stress, control expenses, and make confident decisions about your health.

Pros and Cons of Urgent Care Without Insurance

Pros

- Usually cheaper than emergency room visits

- Fast service with shorter wait times

- No appointment required in most cases

- Transparent self-pay pricing at many clinics

- Convenient evening and weekend hours

Cons

- Costs must be paid out of pocket

- Prices vary widely between clinics

- Extra services increase bills quickly

- Not suitable for serious emergencies

- Follow-up care may cost extra

Common Mistakes People Make

Many patients unknowingly increase their medical expenses. Here are common mistakes to avoid.

1. Not Asking About Prices First

Some people feel uncomfortable discussing cost. Asking upfront can prevent surprises.

2. Choosing Urgent Care for Non-Urgent Issues

Routine checkups are often cheaper at primary care clinics.

3. Ignoring Self-Pay Discounts

Many clinics offer reduced rates if you pay immediately.

4. Assuming All Clinics Charge the Same

Prices can differ by $50–$150 even within the same city.

5. Skipping Follow-Up Instructions

Ignoring care advice may lead to another visit, increasing total costs.

Frequently Asked Questions (FAQs)

How much does urgent care usually cost without insurance?

Most visits range between $100 and $250 for basic care. Costs increase if tests or procedures are needed.

Is urgent care cheaper than the emergency room?

Yes. Emergency room visits can cost hundreds or even thousands of dollars, while urgent care is usually far less expensive.

Can I negotiate urgent care bills?

Some clinics allow payment plans or discounts for self-pay patients. It never hurts to ask politely.

Do urgent care centers require payment upfront?

Many clinics request payment during the visit, especially for patients without insurance.

Conclusion

An urgent care visit without insurance can cost anywhere from about $100 to $400 or more, depending on the treatment you need. While this may seem expensive, it is usually much cheaper than visiting an emergency room for non-life-threatening problems.

The key takeaway is simple: always ask about pricing, understand what services are included, and choose the right level of care for your situation. Planning ahead and knowing your options can help you protect both your health and your finances.

By staying informed, you can use urgent care services wisely and avoid unnecessary medical expenses while still getting the care you need.