Introduction

Nebraska homeowners insurance rates are the prices people pay to protect their homes with insurance in Nebraska. These rates matter because they affect your monthly or yearly budget and your peace of mind. Whether you are buying your first home or reviewing your current policy, understanding how rates work can help you make smarter choices. This article explains what Nebraska homeowners insurance rates are, how they are set, and why they can change. You will also see real-life examples, common mistakes to avoid, and answers to popular questions, all explained in clear and simple language.

Table of Contents

Table of Contents

What is nebraska homeowners insurance rates?

Nebraska homeowners insurance rates are the cost you pay for an insurance policy that protects your home and belongings.

These rates usually cover:

- Damage to your house from fire, wind, or hail

- Theft or damage to personal items

- Liability if someone gets hurt on your property

The rate is often shown as a yearly amount, but many people pay it monthly. The exact price depends on several factors, including where you live and the type of home you own.

Do you know What is Home Insurance?

How does nebraska homeowners insurance rates work?

Nebraska homeowners insurance rates are based on risk. Insurance companies look at how likely it is that they will need to pay for a claim.

Here is the basic process:

- You share details about your home, like its age, size, and location.

- The insurance company reviews risks, such as storms or fire history in your area.

- They estimate the cost to repair or rebuild your home if something happens.

- Based on this information, they set your rate.

If your home is seen as higher risk, the rate is usually higher. Lower risk homes often get lower rates.

Real-life example

Imagine a homeowner in Omaha with a single-family house worth $250,000.

- The insurance company estimates it would cost $220,000 to rebuild the home.

- The annual homeowners insurance rate is $1,800.

- This breaks down to about $150 per month.

Now compare this to a similar home in a rural area with fewer storm claims. That homeowner might pay $1,300 per year instead. The difference shows how location and risk can affect Nebraska homeowners insurance rates.

Why is nebraska homeowners insurance rates important?

Nebraska homeowners insurance rates are important because they affect both your finances and your protection.

Good rates help you:

- Plan your monthly and yearly budget

- Protect your biggest investment, your home

- Avoid large out-of-pocket costs after unexpected damage

If you choose a policy only based on price, you may miss important coverage. Understanding rates helps you balance cost and protection in a smart way.

Do you know What Does AOB Stand for in Insurance?

Pros and cons of nebraska homeowners insurance rates

Pros

- Provides financial protection for your home

- Helps cover repair or replacement costs

- Offers liability coverage for accidents

Cons

- Rates can increase after claims or storms

- Homes in high-risk areas may cost more to insure

- Policies may have limits or exclusions

Knowing both sides helps you set realistic expectations and choose wisely.

Do you know What’s loss of Coverage in Home insurance?

Common mistakes people make

Many homeowners misunderstand how insurance rates work. Here are some common mistakes to avoid:

- Choosing the cheapest policy without checking coverage

- Underestimating how much it costs to rebuild a home

- Forgetting to review or update the policy each year

- Assuming all damage is automatically covered

Avoiding these mistakes can save money and stress later.

Why Nebraska Homeowners Face Unique Insurance Costs

If you own a home in Nebraska, you’ve probably noticed that your insurance bill looks different from what friends in other states pay. There’s a good reason for that. Nebraska consistently ranks as one of the most expensive states for homeowners insurance in the entire country -2. Understanding why rates are higher here helps you make sense of your premium and take control of what you pay.

This guide goes beyond the basics to explore the specific factors driving Nebraska homeowners insurance rates, how your individual choices affect your premium, and the practical steps you can take to find affordable coverage without sacrificing protection.

Where Nebraska Ranks Nationally for Home Insurance Costs

The numbers tell a clear story about Nebraska’s place in the national insurance landscape. Multiple sources confirm that Nebraska homeowners pay some of the highest premiums in the United States.

Average Annual Premiums Compared

| Data Source | Nebraska Average Annual Premium | National Average | Nebraska’s National Rank |

|---|---|---|---|

| Quote.com | $5,652 | Varies by state | #1 most expensive |

| Kin Insurance | $5,127 | $3,303 | Top 5 most expensive |

| InsuredBetter | $2,554 | $1,211 | Among highest |

| Syracuse.com/Bankrae | Over $6,000 | $2,424 | #1 or #2 most expensive |

Note: Premium variations between sources reflect different dwelling coverage amounts, deductible assumptions, and policy types used in each analysis.

These numbers might look alarming at first glance, but they make more sense when you understand what drives them. Nebraska’s position at the top of national rankings isn’t random—it reflects real risks that insurance companies must account for when pricing policies.

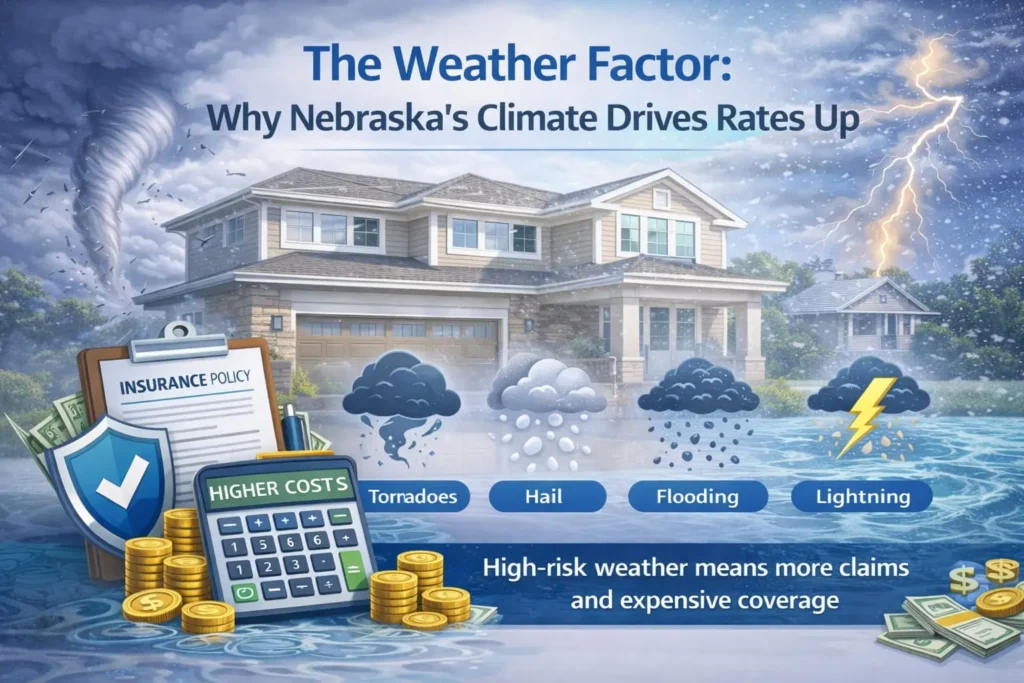

The Weather Factor: Why Nebraska’s Climate Drives Rates Up

Severe Storms and Hail Risk

Nebraska sits in the heart of Tornado Alley, where warm, moist air collides with cooler systems to create powerful storms. This geography comes with consequences for homeowners -2-7.

Hail damage is particularly significant for Nebraska homeowners. Hailstorms can destroy roofs, dent siding, break windows, and damage outdoor equipment in minutes. When a hailstorm moves through a populated area, insurance companies may receive thousands of claims at once. Those claim costs get spread across all policyholders in the region through future rate adjustments -1.

High winds accompanying thunderstorms and tornadoes add another layer of risk. Wind can tear off shingles, topple trees onto houses, and destroy detached structures like garages and sheds. Homes throughout Nebraska face this exposure regardless of whether they’re in cities or rural areas -1.

Frequency of Weather Events

What makes Nebraska different from other storm-prone states is the frequency of damaging weather. Some regions face one major hurricane every few years or occasional wildfires. Nebraska experiences severe thunderstorm and hail events multiple times each year during spring and summer -1-2.

This frequency means insurance companies pay claims in Nebraska more regularly than in many other states. Regular claim payments lead to higher base rates for everyone.

Beyond Weather: Other Factors Affecting Nebraska Rates

While weather gets most of the attention, several other factors contribute to Nebraska’s insurance costs.

Rising Construction and Material Costs

Inflation has pushed up the price of everything needed to repair or rebuild homes. Lumber, roofing materials, siding, drywall, and labor all cost more today than they did just a few years ago -1-8.

When materials cost more, insurance companies must increase premiums to maintain enough money to pay claims. A roof that cost $8,000 to replace five years ago might cost $12,000 today. Those higher claim payments get reflected in everyone’s premiums -1.

Aging Housing Stock

Many Nebraska homes were built decades ago. Older homes often have outdated electrical systems, aging plumbing, and original roofing materials. These features increase the risk of fires, water damage, and weather-related claims -1-7.

Insurers factor in home age when setting rates. An older home that hasn’t been updated may cost significantly more to insure than a newer home with modern systems, even if they’re side by side in the same neighborhood.

Claims History Concentration

When an area experiences widespread storm damage, insurance companies pay out large sums. To recover those funds and maintain financial stability, insurers often request rate increases from state regulators. Because Nebraska faces regular severe weather, these rate adjustments happen more frequently than in milder climates .

How Your Choices Affect Your Nebraska Home Insurance Rate

While you can’t change where you live or the state’s weather patterns, you have significant control over other factors that influence your premium.

Coverage Limits and Deductibles

| Choice | Effect on Premium | Trade-Off |

|---|---|---|

| Higher dwelling coverage limit | Increases premium | More protection if home is destroyed |

| Higher deductible | Decreases premium | More out-of-pocket when filing claim |

| Replacement cost coverage | Increases premium | Full reimbursement for damaged items |

| Actual cash value coverage | Decreases premium | Reimbursement minus depreciation |

Deductible strategy matters. Choosing a higher deductible is one of the most effective ways to lower your premium. However, you must be sure you can afford that amount if disaster strikes. A good rule is to set your deductible at an amount you could pay from emergency savings without borrowing -4.

Home Safety and Maintenance

Insurance companies reward homeowners who reduce risk. Specific actions that may lower your Nebraska rate include:

- Roof upgrades: Impact-resistant roofing materials designed to withstand hail can qualify for discounts.

- Storm shutters or impact-resistant windows: These reduce wind damage risk.

- Sump pumps and water sensors: These prevent water damage from basement flooding.

- Security systems: Monitored burglar alarms and smoke detectors reduce theft and fire risk.

- Electrical and plumbing updates: Modern systems are less likely to fail and cause damage.

Credit Score Impact

In most states, including Nebraska, insurance companies use credit-based insurance scores when setting rates. Homeowners with higher credit scores typically pay less for coverage than those with lower scores, even when everything else about their home is identical .

Improving your credit score by paying bills on time, reducing debt, and avoiding unnecessary credit applications can lead to better insurance rates over time.

City-by-City Rate Differences in Nebraska

Rates vary not just by state but by specific location within Nebraska. Insurance companies analyze claim patterns at the city and even neighborhood level.

Omaha Home Insurance Costs

| Home Value | $500 Deductible | $1,000 Deductible | $2,000 Deductible |

|---|---|---|---|

| $200,000 | $2,292 | $2,135 | $1,923 |

| $300,000 | $3,097 | $2,884 | $2,598 |

| $400,000 | $4,086 | $3,805 | $3,428 |

| $600,000 | $6,351 | $5,914 | $5,328 |

Source: MFP Community Home Insurance Survey -6

Lincoln Home Insurance Costs

| Home Value | $500 Deductible | $1,000 Deductible | $2,000 Deductible |

|---|---|---|---|

| $200,000 | $1,827 | $1,694 | $1,522 |

| $300,000 | $2,467 | $2,288 | $2,055 |

| $400,000 | $3,252 | $3,016 | $2,709 |

| $600,000 | $5,062 | $4,695 | $4,217 |

Source: MFP Community Home Insurance Survey -6

Lincoln’s rates run noticeably lower than Omaha’s in this comparison, demonstrating how local risk factors and claim histories create price differences even within the same state.

Strategies to Lower Your Nebraska Home Insurance Rate

Comparison Shopping Matters

Insurance rates vary significantly between companies for the same home. Getting quotes from multiple insurers ensures you’re not overpaying. Independent agents who represent several companies can make this process easier by shopping for you.

Bundle for Savings

Combining home and auto insurance with the same company typically saves 10 to 25 percent on both policies. This bundling discount is one of the largest available and applies year after year .

Review Your Policy Annually

Your insurance needs change over time. Reviewing your policy each year helps you -4:

- Confirm your dwelling coverage still matches rebuild costs

- Remove coverage you no longer need

- Add endorsements for new valuables or home improvements

- Qualify for new discounts based on home upgrades

Ask About Specific Discounts

Insurance companies offer many discounts that homeowners don’t know about. Common discounts that may apply to Nebraska homeowners include :

- New home discount (homes less than 10 years old)

- Claims-free discount

- Mature homeowner discount (retirees and older adults)

- Protective device discounts (alarms, sprinklers, generators)

- Roof condition discounts

Understanding Rate Increases and What to Do About Them

Why Rates Go Up

Nebraska homeowners sometimes see premium increases even when they haven’t filed claims. Common reasons include :

- Industry-wide rate adjustments after major disaster years

- Rising construction costs in your area

- Changes in your home’s risk profile (aging roof, etc.)

- Inflation adjustments to coverage limits

Responding to Increases

When your premium increases, don’t just accept it. Take these steps -4:

- Call your agent and ask why the increase happened

- Ask if any new discounts apply to your situation

- Request quotes from other companies for comparison

- Consider adjusting your deductible if you can afford higher out-of-pocket costs

- Ask about home improvements that might lower your rate

Comparison Table: Nebraska vs. Neighboring States

| State | Average Annual Premium (Approx.) | Primary Risk Factors |

|---|---|---|

| Nebraska | $5,100 – $5,700 | Severe storms, hail, tornadoes -2-4 |

| Kansas | $4,000 – $4,300 | Tornado Alley, wind, hail -2-4 |

| Iowa | $2,800 – $3,000 | Storms, flooding -4 |

| South Dakota | $3,800 – $3,900 | Winter storms, hail -4 |

| Colorado | $3,800 – $4,600 | Wildfires, hail -2-4 |

| Missouri | $3,500 – $3,700 | Storms, tornadoes -4 |

Nebraska’s rates stand out even compared to nearby states with similar weather patterns, reflecting the frequency and severity of claims in the state.

Final Thoughts on Nebraska Homeowners Insurance Rates

Nebraska homeowners face unique challenges when it comes to insurance costs. The state’s position in Tornado Alley, frequency of severe weather, and rising construction costs all contribute to premiums that rank among the nation’s highest.

However, understanding these factors puts you in a stronger position to manage your costs. By making smart choices about coverage limits, deductibles, home maintenance, and safety upgrades, you can find the right balance between protection and affordability.

Take time each year to review your policy, compare quotes from multiple companies, and ask your agent about discounts. A little attention now can save hundreds of dollars over time while ensuring your home and belongings stay properly protected against whatever Nebraska weather sends your way.

Frequently asked questions (FAQs)

Do Nebraska homeowners insurance rates change every year?

Yes, rates can change due to inflation, claims in your area, or changes to your home.

Are rates higher in cities or rural areas?

It depends. Cities may have higher theft risk, while rural areas may face different weather risks.

Can I lower my homeowners insurance rate?

Often yes. Improving home safety or comparing policies may help reduce costs.

Conclusion

Nebraska homeowners insurance rates are the cost of protecting your home against common risks. These rates depend on your home, location, and overall risk level. By understanding how rates work, you can make better decisions and avoid surprises. Take time to review your policy, understand what you are paying for, and make sure it fits your needs. A well-chosen insurance policy is not just an expense, but a smart step toward long-term security.