Introduction:

Loss of use coverage is a part of your homeowners insurance or renters insurance that helps pay for extra living expenses if your home becomes temporarily uninhabitable due to a covered loss.

In simple words:

If you cannot live in your home because of damage from a covered event (like fire or storm), loss of use coverage pays for your temporary living costs.

This coverage is also known as:

Additional Living Expenses (ALE)

Coverage D (in homeowners insurance)

Table of Contents

Table of Contents

Why Loss of Use Coverage Is Important

Imagine this situation:

Your house catches fire, and repairs will take three months. You cannot live there during that time.

Without loss of use coverage, you would have to pay for:

Hotel rent

Extra food costs

Transportation

Laundry

Temporary housing

With loss of use coverage, your insurance company helps cover these extra expenses, so your life can continue normally while repairs are made.

Do you know what is avarage price of home insurence in ma?

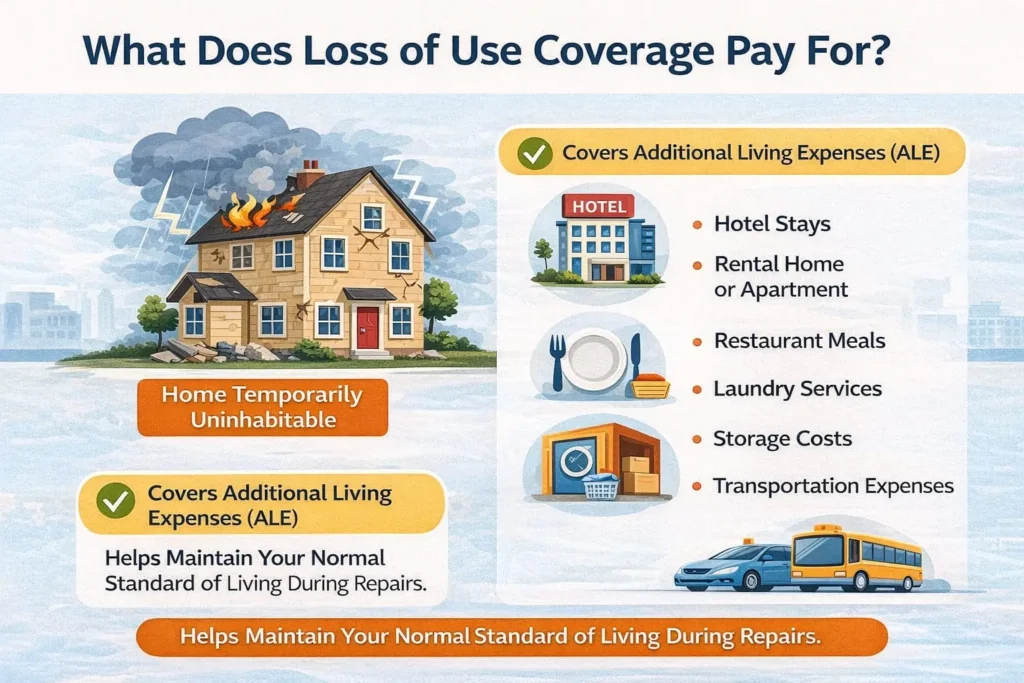

What Does Loss of Use Coverage Pay For?

Loss of use coverage pays for expenses above your normal living costs.

Common Expenses Covered

- Temporary Housing

Hotel stays

Rental apartments

Short-term housing - Increased Food Costs

Eating out more often

Loss of access to your kitchen - Transportation Costs

Extra travel expenses due to relocation

Longer commute distances - Laundry and Storage

Laundromat services

Storage fees for personal belongings - Pet Boarding (in some cases)

If pets cannot stay in temporary housing

Important: Insurance pays the difference, not your normal expenses.

Example of How Loss of Use Coverage Works

Let’s say:

Your normal monthly rent: $800

Temporary rental cost:$1,200

Extra food expenses: $300

Your insurance may cover:

$400 (extra rent)

$300 (extra food)

Total covered:$700

You still pay what you normally would have paid.

Do you know How to write an appeal letter to insurence companay?

What Events Trigger Loss of Use Coverage?

Loss of use coverage only applies if your home becomes unlivable due to a covered peril.

Common Covered Events

- Loss of use coverage only applies if your home becomes unlivable due to a covered peril.

- Common Covered Events

- Fire or smoke damage

- Storms (wind, hail)

- Lightning

- Explosion

- Water damage from burst pipes

- Vandalism

- Events Usually NOT Covered

- Floods (unless you have flood insurance)

- Earthquakes (unless separately insured)

- Poor maintenance

- Normal wear and tear

- Always check your policy details.

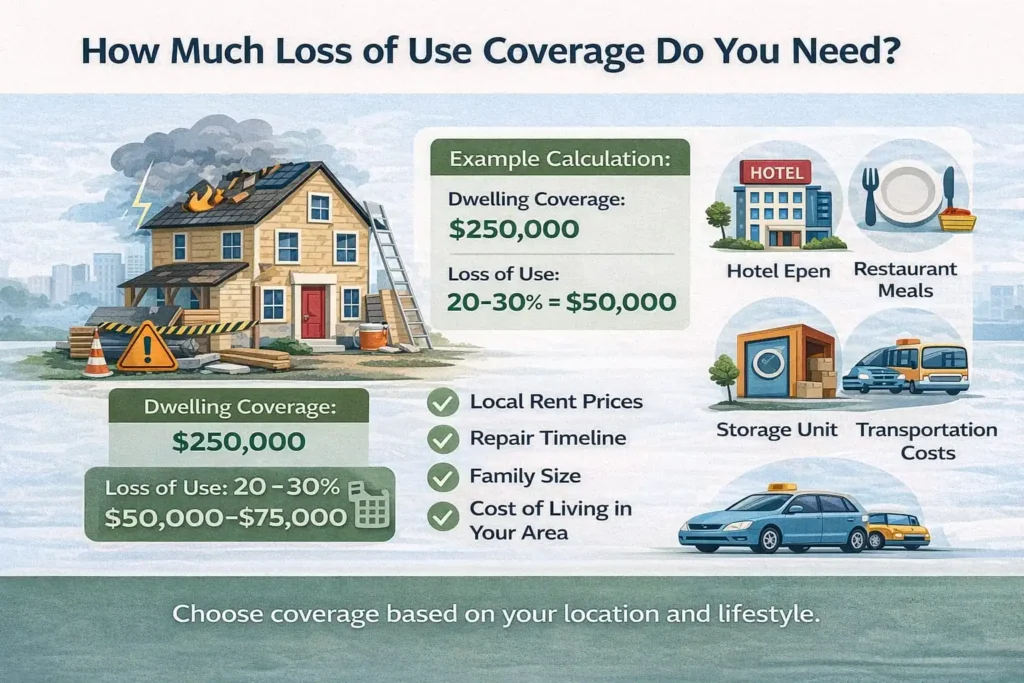

Loss of Use Coverage in Homeowners Insurance

In homeowners insurance, loss of use coverage is usually labeled as Coverage D.

How Much Coverage Do You Get?

Most policies provide:

20% to 30% of your dwelling coverage

Example:

Dwelling coverage:$200,000

Loss of use coverage:$40,000–$60,000

Loss of Use Coverage in Renters Insurance

Renters insurance also includes loss of use coverage, even though you don’t own the property

Do you know What Is Dwelling Coverage in Home Insurance?

What It Covers for Renters

- Temporary housing

- Food expenses

- Storage costs

- This is extremely valuable for renters who may not have emergency savings.

Loss of Use Coverage vs Property Damage

Many people confuse these two.

Coverage Type

What It Covers

Property Damage

Repair or replacement of home

Loss of Use

Living expenses during repairs

They work together, not separately.

How Long Does Loss of Use Coverage Last?

Coverage lasts until:

- Your home is repaired, or

- You reach your policy limit

- It does not last forever.

Insurance companies expect you to:

- Find reasonable housing

- Avoid unnecessary expenses

- How to File a Loss of Use Coverage Claim

Step-by-Step Process

- Contact your insurance company immediately

- Ask if your situation qualifies

- Keep all receipts

- Track your normal vs extra expenses

- Submit documents on time

Tip: Always save receipts—insurance will not pay without proof.

Common Mistakes to Avoid

- Not Reading Policy Limits

Many people assume unlimited coverage—this is false. - Choosing Luxury Housing

Insurance pays for reasonable living expenses, not luxury upgrades. - Forgetting Receipts

No receipts = no reimbursement.

Do you know are the common people mistakes while chosing the home insurence?

How Much Loss of Use Coverage Do You Need?

Ask yourself:

- How expensive is rent in your area?

- How long repairs could take?

- Do you have dependents or pets?

- If you live in a high-cost city, consider increasing your coverage.

- Is Loss of Use Coverage Required by Law?

❌ No, it is not legally required.

✅ But it is strongly recommended, especially for:

Renters

Renters

Homeowners in disaster-prone areas

How to Increase Loss of Use Coverage

You can:

- Increase dwelling coverage

- Add policy endorsements

- Upgrade to premium plans

- Always compare cost vs benefit.

- Loss of Use Coverage and AdSense-Friendly Content Note

Does Loss of Use Coverage Have a Time Limit?

While many people assume coverage lasts “as long as needed,” policies often state:

Coverage applies for the shortest time required to repair or replace the property using reasonable speed.

Insurance companies may monitor:

- Repair progress

- Contractor timelines

- Housing choices

Delays caused by homeowner decisions may not extend coverage.

How Claims Payments Are Made

There are generally two payment methods:

1. Reimbursement Model

You pay first.

You submit receipts.

Insurance reimburses approved amounts.

2. Direct Payment to Hotel or Landlord

In some cases, insurers can directly pay temporary housing providers.

Always ask your adjuster which method applies to your claim.

Tax Implications of Loss of Use Payments

In most cases, insurance reimbursements for additional living expenses are not taxable income, because they are considered compensation for a loss — not profit.

However, if you receive reimbursement exceeding your actual expenses, consult a tax professional.

Special Considerations for High-Cost Areas

If you live in:

- Major metropolitan areas

- Coastal cities

- High-rent regions

Temporary housing can be extremely expensive.

Standard 20–30% dwelling limits may not be enough.

In such cases, consider:

- Extended loss of use endorsements

- Guaranteed replacement cost policies

- Higher dwelling limits

Planning ahead prevents underinsurance.

Loss of Use Coverage for Condo Owners

If you own a condominium, your HOA master policy covers common areas, but your condo insurance (HO-6 policy) typically includes loss of use coverage for your unit.

It may cover:

- Temporary housing

- Additional living expenses

- Loss of rental income (if applicable)

Always review your condo association agreement to understand coverage gaps.

What Happens If Repairs Take Longer Than Expected?

Delays can happen due to:

- Contractor shortages

- Permit delays

- Supply chain issues

- Severe weather

If delays are beyond your control, speak with your insurer. Some companies may grant limited extensions depending on circumstances.

Communication is key.

When Loss of Use Coverage Does NOT Apply — Even If Damage Exists

Even if your home has damage, coverage may not apply if:

- The home is still considered livable

- You choose to move out voluntarily

- Damage is cosmetic only

- Repairs are optional improvements

Insurance companies determine habitability based on safety standards, not convenience.

How to Prepare Before Disaster Strikes

The best time to review your policy is before you need it.

Here are smart preparation steps:

- Review your Coverage D limit annually.

- Keep digital copies of your policy.

- Understand your deductible.

- Maintain an emergency fund.

- Document normal monthly living expenses for comparison later.

Preparation reduces stress during emergencies.

Questions to Ask Your Insurance Agent

To fully understand your protection, ask:

- What is my current loss of use limit?

- Is it percentage-based or time-based?

- Are there daily limits?

- Does my policy include fair rental value?

- Can I increase my Coverage D?

Clear answers prevent confusion during claims.

The Psychological Benefit of Loss of Use Coverage

Financial protection is only part of the value.

When families are displaced after a disaster, stress levels increase dramatically. Knowing that temporary housing and essential expenses are covered provides emotional stability during a difficult time.

Insurance is not just about rebuilding walls — it’s about maintaining normal life during disruption.

Cost of Adding or Increasing Loss of Use Coverage

Increasing dwelling coverage automatically increases loss of use limits (since it’s percentage-based in most policies).

The additional premium is often modest compared to the protection gained.

For example:

- Increasing dwelling coverage by $50,000 may slightly raise your premium but also raise your Coverage D limit proportionally.

Always request a quote before making changes.

Do you know How to save on home Insurence?

Is Loss of Use Coverage Worth It?

For most homeowners and renters, the answer is yes.

Temporary displacement can cost thousands per month.

Without coverage, expenses such as:

- Rent

- Food

- Utilities

- Storage

- Transportation

must come entirely from personal savings.

Loss of use coverage acts as a financial bridge during recovery.

Key Takeaways

- Loss of use coverage protects your lifestyle, not your structure.

- It activates only after covered perils make your home unlivable.

- It covers extra costs — not your regular expenses.

- Coverage limits matter more than most people realize.

- Proper documentation ensures smoother claims.

Understanding these details helps you make informed insurance decisions and avoid unexpected financial burdens.

Frequently Asked Questions (FAQs)

What is loss of use coverage in simple words?

It pays for extra living expenses if you cannot live in your home due to covered damage.

Is loss of use coverage the same as additional living expenses?

Yes. They mean the same thing.

Does loss of use coverage cover hotel stays?

Yes, if your home is unlivable due to a covered loss.

Does renters insurance include loss of use coverage?

Yes, most renters insurance policies include it.

Does loss of use coverage cover floods?

No, unless you have separate flood insurance.

How long can I use loss of use coverage?

Until repairs are complete or policy limits are reached.

Do I need receipts for reimbursement?

Yes, receipts are required.

Final Thoughts

Loss of use coverage is one of the most overlooked but valuable parts of an insurance policy. It protects your lifestyle, not just your property.

Whether you are a homeowner or renter, understanding this coverage can save you thousands of dollars during unexpected disasters.