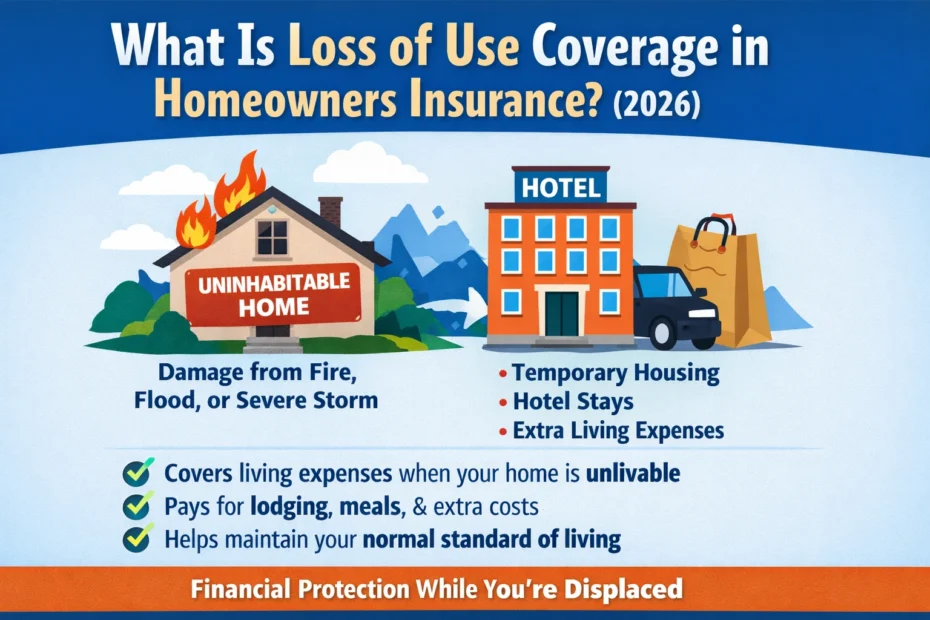

When disaster strikes your home—like a fire, storm, or water damage—your property may become temporarily uninhabitable. This is where loss of use coverage comes into play. It is a crucial part of most homeowners insurance policies in the United States, designed to protect you financially when you cannot live in your home due to covered damages.

Table of Contents

Understanding Loss of Use Coverage

Loss of use coverage, also known as additional living expenses (ALE), helps pay for the extra costs of living elsewhere while your home is being repaired. These expenses go beyond your normal living costs and may include:

- Temporary housing or hotel stays

- Meals if you cannot cook at home

- Laundry and other day-to-day expenses

- Storage of your belongings if your home is uninhabitable

For example, if a fire damages your kitchen and you cannot cook meals, loss of use coverage may reimburse hotel bills and dining out costs for the duration of repairs.

Do you know is home insurence cover burst pipe?

How Loss of Use Coverage Works

Loss of use coverage is not unlimited. Most policies set a coverage limit, either as a percentage of your dwelling coverage (often 20%) or a fixed dollar amount. For example, if your home insurance policy covers $300,000 for your house, your loss of use coverage may provide up to $60,000 for living expenses.

The duration of coverage depends on the time required to restore your home to a livable condition. Insurance companies typically require proof of expenses, so it’s important to keep all receipts for temporary housing, meals, and other costs.

Do you know Dose home insure cover Water Damage From Appliances?

Common Scenarios Covered

Loss of use coverage generally applies when the home becomes uninhabitable due to covered perils. These may include:

- Fire damage

- Water damage from burst pipes

- Storms or hail

- Vandalism or theft

It’s important to note that damage from floods or earthquakes is usually excluded unless you have separate policies for those perils.

How to Maximize Your Loss of Use Coverage

- Know your policy limits – Check your homeowners insurance to see how much ALE coverage you have.

- Document expenses carefully – Keep receipts, invoices, and photos of the damaged property.

- Notify your insurer promptly – Immediate communication helps speed up approval.

- Consider additional coverage – If you live in a disaster-prone area, consider increasing your ALE coverage.

Why Loss of Use Coverage Is Important

Loss of use coverage can save homeowners thousands of dollars during repairs. Without it, you would have to cover temporary living costs out-of-pocket, which can quickly add up. It also provides peace of mind, knowing that your insurance policy helps you maintain your lifestyle while your home is being restored.

Tips to Maximize Your Loss of Use Coverage

- Know Your Policy: Understand your ALE limits and any exclusions.

- Keep Records: Save all receipts for temporary lodging, meals, and other expenses.

- Notify Your Insurer Quickly: Prompt notification speeds up claim approval.

- Consider Higher Coverage: If you live in areas prone to disasters, request higher ALE limits.

- Coordinate With Contractors: Ensure your home repair timeline aligns with your temporary living arrangement.

Do you know How to Write an Appeal Letter to an Insurance Company?

Additional Benefits of Loss of Use Coverage

- Peace of Mind: You don’t need to worry about paying extra out-of-pocket costs.

- Financial Stability: Helps prevent unexpected bills from derailing your budget.

- Flexibility: Provides the freedom to choose temporary housing that suits your family’s needs.

- Pet Coverage: Some policies include boarding costs for pets displaced by home damage.

Common Misconceptions About Loss of Use Coverage

- “It covers everything automatically” – Not true; it only applies to covered perils.

- “It lasts forever” – Coverage lasts until your home is restored or within policy limits.

- “You don’t need to document expenses” – Always keep receipts; insurers require proof.

Why Loss of Use Coverage Is Essential

Without loss of use coverage, homeowners would have to pay out-of-pocket for hotels, meals, and other necessities. These costs can add up quickly during repairs or reconstruction.

Having this coverage ensures you can maintain your lifestyle, even when your home is temporarily unlivable.

Do you know how much is home insurence cost in ma?

Final Thoughts

In the United States, loss of use coverage is a vital part of homeowners insurance. It ensures you are not financially burdened if your home becomes temporarily unlivable due to a covered event. Always review your policy carefully, understand your limits, and keep thorough documentation of all related expenses. By doing so, you can protect your home, your finances, and your family’s well-being.

FAQs About Loss of Use Coverage

1. Does loss of use coverage pay for pets?

Yes, some policies include pet boarding expenses if your home is uninhabitable.

2. Is hotel accommodation fully covered?

It is covered up to your policy limit. Keep receipts for reimbursement.

3. Can I claim meals and utilities?

Yes, extra meals and essential utilities are typically reimbursable.

4. How long does coverage last?

Coverage lasts until your home is repaired or rebuilt, within policy limits.