Introduction

One of the most common questions new and future homeowners ask is: how much is home insurance? The answer depends on several factors, but understanding the basics can help you budget smarter and avoid overpaying.

Home insurance protects your house, belongings, and finances if something unexpected happens. While prices vary across the U.S., this guide explains the average cost of homeowners insurance, what affects your rate, and how you can lower your premium.

Table of Contents

Table of Contents

What Is the Average Cost of Home Insurance in the U.S.?

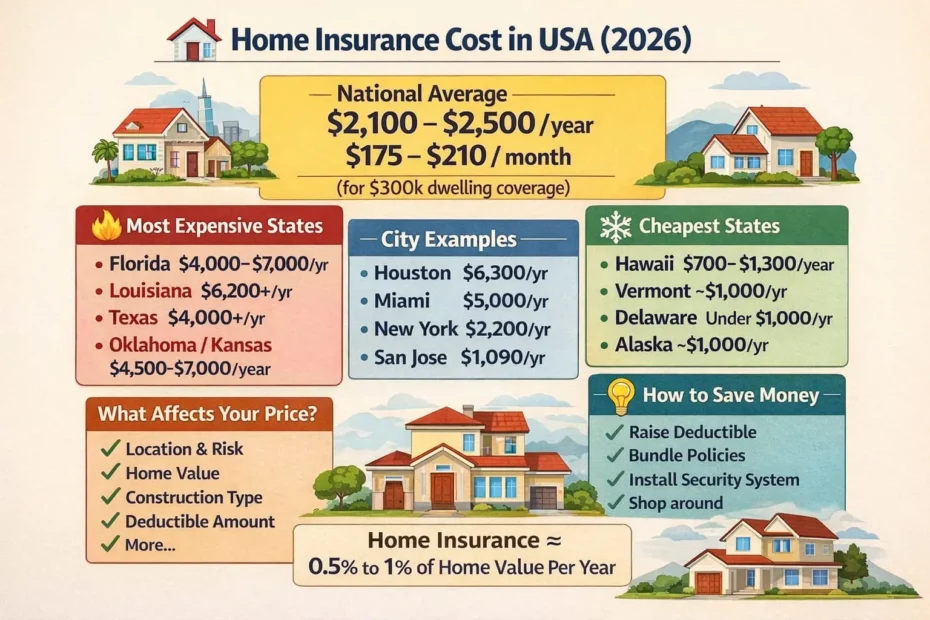

In the United States, the average homeowners insurance cost is usually between $1,200 and $2,000 per year for a standard policy. That works out to about $100 to $170 per month.

However, your actual price could be lower or much higher depending on where you live and the type of home you own.

Homes in areas with high risks—such as hurricanes, wildfires, or severe storms—often have higher insurance rates.

What Does Home Insurance Cost Cover?

Your premium pays for several types of protection, including:

- Dwelling coverage – Repairs or rebuilding your home

- Personal property coverage – Replaces belongings after theft or damage

- Liability protection – Covers injuries or property damage you’re responsible for

- Additional living expenses – Pays for temporary housing if your home becomes unlivable

The more coverage you choose, the higher your insurance cost will be.

Do you know What Is Loss of Use Coverage?

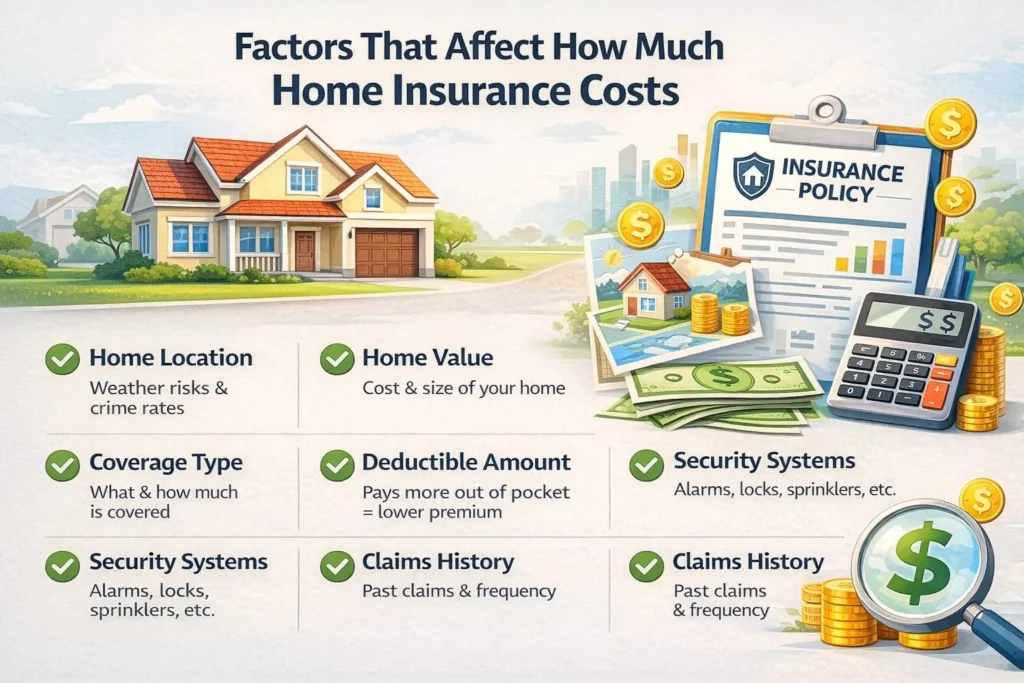

Factors That Affect How Much Home Insurance Costs

Insurance companies look at many details when setting your rate.

1. Location of Your Home

Where you live is one of the biggest price factors. Insurers consider:

- Crime rates

- Weather risks

- Distance from fire stations

- Local building costs

For example, coastal homes may cost more to insure because of hurricane risk.

2. Home Value and Size

Larger homes and homes that cost more to rebuild usually have higher premiums. Insurance is based on rebuilding cost, not market value.

3. Deductible Amount

Your deductible is what you pay before insurance kicks in.

- Higher deductible = Lower monthly premium

- Lower deductible = Higher premium

4. Age and Condition of the Home

Older homes with outdated plumbing, wiring, or roofs often cost more to insure. Upgraded systems can sometimes lower your rate.

5. Claims History

If you’ve filed multiple claims in the past, insurers may see you as higher risk, which can raise your premium.

Do you know Home Insurance Claim Adjuster Secret Tactics?

Real-Life Cost Example

Let’s say you own a $300,000 home in a low-risk suburban area.

- Annual premium: $1,500

- Monthly cost: About $125

- Deductible: $1,000

If a covered storm causes $10,000 in damage, you would pay the $1,000 deductible, and insurance may cover the remaining $9,000.

Without insurance, you would likely pay the full amount yourself.

How to Lower Your Home Insurance Cost

You don’t have to accept the first quote you get. Here are ways to save:

- Bundle policies (home + auto)

- Increase your deductible if you can afford it

- Install safety features like smoke detectors and security systems

- Shop around and compare quotes from multiple insurers

- Maintain your home to reduce risk of damage

Even small discounts can add up over time.

Do you know is Homeowners Insurance Cover Mold-2026?

Why Understanding Home Insurance Cost Matters

Knowing how much homeowners insurance costs helps you:

- Plan your monthly housing budget

- Choose the right coverage limits

- Avoid being underinsured

- Make better decisions when buying a home

Insurance is not just another bill — it protects your finances from major, unexpected expenses.

Breaking Down Home Insurance Premiums: What You’re Really Paying For and How to Spot Savings

When you receive your home insurance bill, it’s easy to see it as just another monthly expense. But behind that number is a detailed calculation that reflects your specific situation, your choices, and the risks insurance companies are willing to accept. Understanding exactly what goes into your premium helps you make informed decisions and identify savings opportunities you might otherwise miss.

This guide takes you deeper into the world of home insurance pricing, explaining the components of your premium, regional cost differences, and the specific strategies that actually lower what you pay.

The Anatomy of Your Home Insurance Premium

Every dollar of your home insurance premium serves a purpose. Insurance companies collect premiums from all policyholders to create a pool of money that pays for claims, operating expenses, and profits. Understanding where your money goes helps you see why rates vary between companies and locations.

Loss Costs

The largest portion of your premium pays for future claims. Insurers study years of data to predict how much they’ll likely pay out for homes like yours in your area. If your neighborhood has experienced frequent hail damage claims, your premium reflects that historical pattern.

Reinsurance

Insurance companies buy their own insurance to protect themselves from catastrophic events. After major hurricanes or wildfires, insurers collect from reinsurers to help pay all the claims. These reinsurance costs get passed down to policyholders, which is why rates often rise across entire states after a disaster year.

Operating Expenses

Your premium also covers the cost of running the insurance company—employee salaries, office locations, customer service centers, and the technology that processes payments and claims. Companies with efficient operations can often offer lower rates.

Profit Margin

Insurance companies are businesses that need to make money to stay in business. A small portion of every premium goes toward profit for shareholders or reinvestment into the company.

Regional Cost Differences Across the United States

Home insurance prices vary dramatically depending on where you live. Understanding these differences helps you set realistic expectations and recognize whether a quoted rate is reasonable for your area.

Highest-Cost States

States prone to natural disasters consistently see the highest average premiums. Louisiana, Florida, Texas, Oklahoma, and California frequently top the lists for expensive home insurance. Coastal properties face hurricane and windstorm risks, while parts of the Midwest deal with frequent tornadoes and hail. Wildfire-prone areas of California and the West carry their own price premiums.

Lowest-Cost States

States with milder weather patterns and lower population density often enjoy the most affordable rates. Oregon, Idaho, Utah, Wisconsin, and parts of the Pacific Northwest typically see below-average premiums. These areas experience fewer catastrophic weather events, and rebuilding costs tend to be more moderate.

Urban vs. Rural Differences

City homes sometimes cost less to insure because they’re closer to fire stations and have better access to emergency services. However, urban areas with higher crime rates may see increased theft and vandalism claims that push prices up. Rural homes face opposite trade-offs—lower crime but longer emergency response times and potentially higher rebuilding costs due to fewer local contractors.

The Deductible Balancing Act

Your choice of deductible is one of the most powerful tools for controlling your premium, but it requires careful thought about your financial situation.

How Deductibles Affect Premiums

Raising your deductible from $500 to $1,000 can lower your premium by roughly 15 to 25 percent. Moving up to a $2,500 deductible might save even more—sometimes 30 percent or higher. These savings add up year after year.

The Risk You Take

The trade-off is obvious: you’ll pay more out of pocket if something happens. The question isn’t just whether you can afford the higher deductible today. It’s whether you could write that check tomorrow after a storm damages your roof or a fire destroys your kitchen.

Finding Your Comfort Zone

A good approach is to set your deductible at an amount you could cover from emergency savings without borrowing money. For many families, this sweet spot falls between $1,000 and $2,500. The premium savings from going higher than that might not be worth the financial strain of a larger out-of-pocket payment during an already stressful time.

Discounts That Actually Make a Difference

Insurance companies advertise many discounts, but some save more money than others. Knowing which discounts offer real savings helps you prioritize your efforts.

Loyalty and Bundling Discounts

Staying with the same company for multiple years often triggers loyalty discounts. Bundling home and auto insurance with one carrier typically saves 10 to 25 percent on both policies. This is consistently one of the largest available discounts.

Protective Device Discounts

Installing monitored burglar alarms, fire sprinklers, and whole-home backup generators can qualify for discounts. The key word is “monitored”—systems that automatically alert a central station or emergency services provide more savings than unmonitored local alarms.

Mature Homeowner Discounts

Retirees and older homeowners who spend more time at home often qualify for discounts. The reasoning is simple: someone home more often is more likely to notice a small fire, detect a water leak early, or prevent a burglary.

Claims-Free Discounts

Years without filing a claim build what’s called a loss-free history. Many insurers reward this with gradually increasing discounts. One claim can reset this progress, which is another reason to think carefully before filing small claims.

New Home Discounts

Homes less than ten years old with modern electrical, plumbing, and HVAC systems qualify for better rates. New construction follows updated building codes and uses materials that meet current safety standards.

How Insurance Scores Affect Your Rate

Many homeowners don’t realize that their credit history influences their insurance premium. Insurance companies use something called an insurance score, which is similar but not identical to a traditional credit score.

What Insurers Look For

Insurance scores predict the likelihood of filing a claim. Studies show a correlation between certain credit behaviors and claim frequency. Payment history, outstanding debt, credit history length, and new credit applications all factor into the calculation.

Improving Your Insurance Score

The same habits that build good credit also improve your insurance score. Paying bills on time, keeping debt manageable, and avoiding unnecessary credit applications all help. Unlike a credit check for a loan, insurance inquiries don’t typically harm your score.

States That Restrict Credit Use

Some states limit or prohibit using credit information in insurance pricing. California, Maryland, and Massachusetts have restrictions, while other states allow insurers to fully consider credit history. If you live in a state that allows credit scoring, maintaining good credit directly lowers your premium.

When Premiums Increase Unexpectedly

Sometimes your home insurance bill arrives higher than last year with no obvious explanation. Understanding common reasons for increases helps you respond appropriately.

Industry-Wide Rate Adjustments

After a year with major disasters like hurricanes or wildfires, insurance companies across entire regions raise rates to recover losses and pay for reinsurance. These increases affect everyone, even homeowners who never filed a claim.

Inflation and Construction Costs

When lumber, labor, and materials become more expensive, the cost to rebuild your home rises. Insurance companies automatically adjust coverage limits to keep pace with inflation, which increases your premium. This protects you from being underinsured but does raise your bill.

Changes in Your Personal Risk Profile

Adding a trampoline, getting a dog, or letting your home fall into disrepair can trigger premium increases. Insurers may also run periodic checks and discover that your roof is now twenty years old or that you’ve filed multiple claims.

What to Do About Increases

When your premium rises, call your agent and ask why. Sometimes they can explain the specific reason. Other times, they can shop for better rates with other companies. An increase doesn’t mean you’re stuck paying more—it means it’s time to compare options.

The True Cost of Being Underinsured

Saving money on premiums by choosing lower coverage limits might feel smart today, but the long-term risk deserves careful consideration.

The Gap Between Market Value and Rebuild Cost

Your home might sell for $300,000, but rebuilding it after a total loss could cost $400,000 because of demolition, debris removal, and current construction prices. Insuring for market value leaves you $100,000 short.

Coinsurance Penalties

Some policies include coinsurance clauses that penalize you for being underinsured. If you insure your home for only 70 percent of its rebuild cost when the policy requires 80 percent, your claim payment gets reduced by a percentage too.

Personal Property Gaps

Underestimating the value of your belongings is easy. Adding up everything in every room often surprises people. Being underinsured on personal property means accepting less money to replace your furniture, clothing, and electronics.

FAQs About Home Insurance Costs

Is home insurance included in my mortgage?

It’s usually paid through your mortgage escrow account, but it’s still your separate insurance policy.

Why did my home insurance go up this year?

Rates can rise due to inflation, higher building costs, increased local risks, or past claims.

Is cheaper home insurance better?

Not always. Lower prices may mean less coverage or higher deductibles.

How often should I compare rates?

It’s smart to shop around every 1–2 years to make sure you’re still getting a good deal.