Introduction

Buying a new car is exciting. You drive it home, it smells fresh, and everything feels perfect. But that new-car shine fades fast—literally. The moment you leave the dealership, the vehicle can lose 15–25% of its value in the first year. If something bad happens—like a serious accident or theft—your standard auto insurance only pays what the car is worth right then, not what you paid or still owe. That’s where gap insurance comes in. It covers the “gap” between the insurance payout and your remaining loan or lease balance.

For most new-car buyers who finance or lease, this small add-on can prevent a big financial headache. New cars depreciate the quickest, so the risk is highest in the first 2–3 years. Understanding the real cost of gap insurance helps you decide whether it’s worth the extra few dollars a month. In this guide, we’ll break down exactly what gap insurance is, how it functions, typical prices you’ll see in 2025–2026, a realistic example with numbers, why it matters so much for new vehicles, the clear pros and cons, frequent mistakes people make, answers to the questions shoppers ask most often, and practical next steps so you can make a confident choice.

What Is Gap Insurance on a New Car?

Table of Contents

Table of Contents

Gap insurance (Guaranteed Asset Protection) is an optional coverage that pays the difference between:

- The actual cash value (ACV) your primary auto insurer pays if the car is declared a total loss, and

- The amount you still owe on your auto loan or lease.

New cars are especially vulnerable because depreciation hits hardest right after purchase. A $40,000 sedan might be worth only $30,000–$32,000 after 12 months and 12,000 miles—even if it’s in perfect condition. If that car gets totaled, standard collision or comprehensive coverage pays the lower ACV. Without gap, you’re responsible for the rest of the loan.

Important facts:

- Gap only applies to covered total losses (collision, comprehensive claims like theft, fire, flood—not mechanical breakdowns).

- It’s most valuable when you have a small down payment, long loan term (60–84 months), or negative equity rolled in from a trade-in.

- Lenders and leasing companies frequently require it when your down payment is under 20% or when the loan-to-value ratio is high.

- You can usually buy it for the life of the loan, but many people drop it once the car’s value catches up to (or exceeds) the balance.

Think of it as a safety net specifically designed for the rapid value drop that almost every new car experiences.

How Does Gap Insurance Work?

The mechanics are simple once you see them in sequence.

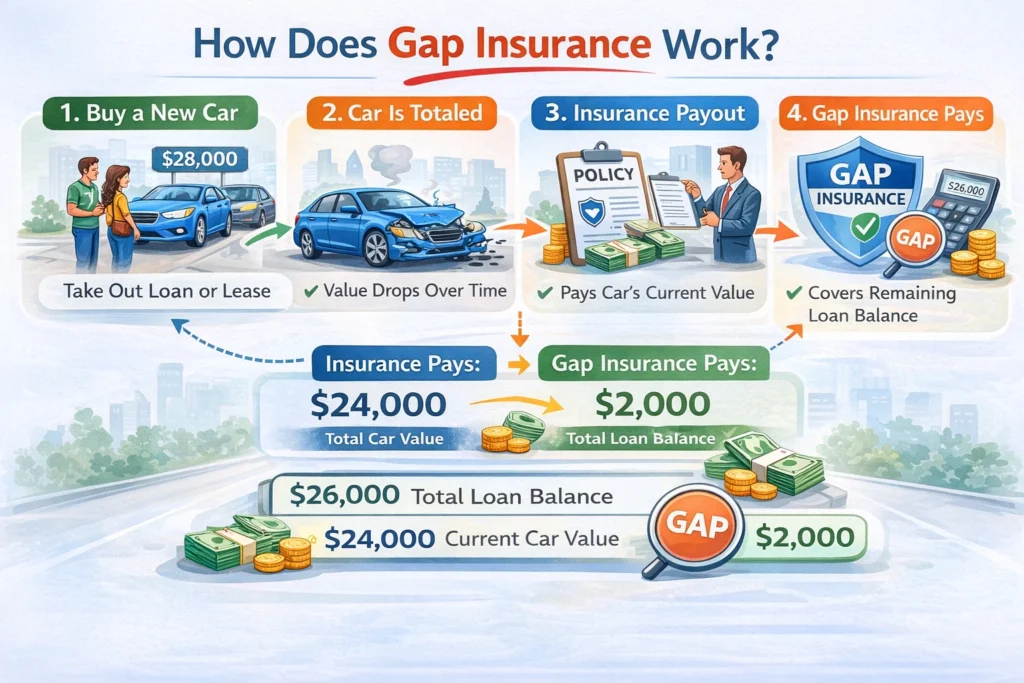

- Purchase and finance the vehicle. You agree on a price—let’s say $38,000 including taxes and fees. You put $3,000 down and finance $35,000 at 6% interest over 72 months.

- Depreciation begins immediately. Industry data shows new cars lose about 20% in year one, then 10–15% per year after that. By month 12 your $38,000 car might have an ACV of only $29,500–$31,000 (Kelley Blue Book or NADA guides set these figures).

- A covered loss occurs. Another driver rear-ends you, or hail damages the car beyond repair. The adjuster declares it a total loss. Your collision/comprehensive policy pays the current ACV—say $30,000—minus your deductible.

- The gap appears. You still owe $33,200 on the loan. The primary insurance payout leaves $3,200 unpaid (plus any deductible you already paid).

- Gap insurance steps in. If you have the coverage, the gap provider sends a check for $3,200 (or more, depending on policy details) directly to the lender. The loan is paid off in full.

- You’re free to start over. No lingering payments on a wrecked car. Any leftover settlement money (rare, but possible) goes toward your next vehicle.

You can purchase gap three main ways:

- Through your existing auto insurer (usually cheapest—added as an endorsement).

- From the dealership at signing (convenient but often most expensive).

- Through your lender or credit union (mid-range price, sometimes rolled into the loan).

Most policies let you cancel once you no longer need it, and many refund unused premium if paid upfront.

Real-Life Example with Realistic Numbers

Meet Alex, a 29-year-old teacher in a mid-sized U.S. city. In early 2025 he buys a new compact crossover for $36,500 out-the-door. He trades in his old car (worth $8,000, but he owes $11,000), so negative equity of $3,000 rolls into the new loan. Down payment: $1,500. Financed amount: $38,000 over 72 months at 7.2% interest.

Six months later—8,500 miles on the odometer—the crossover is worth approximately $27,800 according to current valuation tools.

One rainy evening a distracted driver crosses the center line and hits Alex head-on. Airbags deploy, the frame is bent, and the car is totaled. Alex’s insurer (a major national company) pays $27,800 ACV minus his $500 deductible = $27,300 to the lender.

Loan balance at that point: $35,900.

Without gap insurance Alex would owe $8,600 out of pocket to clear the loan—on top of medical co-pays, rental car costs, and shopping for a replacement vehicle while still making payments on nothing.

Luckily, Alex added gap through his insurer for $6.40 per month ($77 per year). The gap policy covers the full $8,600 difference. The lender receives payment in full within two weeks. Alex pays zero toward the old loan, uses his uninsured/underinsured motorist settlement for medical bills, and starts looking for a used replacement without the weight of old debt.

Total cost of protection over six months: about $38. That $38 saved him over $8,500.

Do yo know what is How Much Is Car Insurance Per Month in NJ?

Why Is Gap Insurance Important for New-Car Buyers?

New vehicles lose value faster than almost any other major purchase. The first 12–36 months are when you’re most likely to be “upside down”—owing more than the car is worth. Gap insurance acts as financial protection during exactly that window.

Benefits in everyday terms:

- Prevents surprise five- or six-figure debt after a total loss.

- Keeps monthly cash flow intact—no forced payments on a car you can’t drive.

- Protects credit score (unpaid auto loans hurt scores for years).

- Gives breathing room to replace the vehicle without panic.

- Often required by lenders anyway, so you’re not choosing between paying extra or risking denial.

For people who put 10% or less down, choose 72+ month terms, or roll negative equity, the protection is almost essential. Even with larger down payments, a single bad crash can create a painful gap of $5,000–$15,000. The tiny premium is usually a fraction of one month’s car payment.

Pros and Cons of Gap Insurance on a New Car

Pros:

- Very affordable when purchased through your auto insurer—typically $3–$10 per month.

- Can save thousands (or tens of thousands) in a total-loss situation.

- Provides peace of mind during the highest-risk depreciation period.

- Easy to cancel and often refundable when no longer needed.

- Widely available and simple to add to an existing policy.

Cons:

- Unnecessary if you make a large down payment (20–30%) and pay extra principal each month.

- Dealership pricing is frequently inflated—$500–$1,200 one-time fees vs. $50–$150/year from an insurer.

- Doesn’t cover every expense (gap policies usually exclude custom parts, extended warranties, or late fees).

- Some people forget to cancel it after the loan balance drops below ACV and pay for coverage they no longer need.

For the majority of new-car financings, the pros strongly outweigh the cons—especially in the first few years.

Common Mistakes People Make

Shoppers and new owners trip over the same issues again and again. Here are the most frequent ones, explained gently so you can sidestep them:

- Believing standard auto insurance pays off the entire loan. It pays only current market value—gap fills everything else.

- Accepting the dealership’s gap quote without shopping around. Dealer markups are common and can be 5–10× higher than insurer rates.

- Skipping gap because “I drive carefully.” No one plans for the other driver’s mistake—accidents happen every day.

- Keeping gap coverage for the full loan term even after the vehicle is no longer upside down. Check values yearly and drop it to save money.

- Assuming negative equity from a trade-in doesn’t count. Rolled-over debt increases the gap dramatically—make sure coverage includes it.

A quick call to your insurer or a valuation check can prevent these slip-ups.

Frequently Asked Questions (FAQs)

How much does gap insurance usually cost on a new car in 2025–2026? Through your auto insurance company, expect $25–$120 per year—most commonly $4–$9 per month. Dealership or lender versions often charge $400–$950 as a single fee added to the loan.

Is gap insurance from the dealer a bad deal? Not always bad, but usually much more expensive. The same coverage through your insurer is almost always cheaper. Compare quotes before signing.

Do I need gap insurance if I put 20% down? Probably not. A large down payment usually keeps you from being upside down for long. Run the numbers with your loan amortization schedule.

Can I get gap insurance after I buy the car? Yes—in most cases you have 30–90 days from purchase (varies by insurer and state). Some companies allow it later, but premiums may be higher.

Conclusion

Gap insurance on a new car is a low-cost way to protect yourself from the harsh reality of rapid depreciation. For a typical financed new vehicle, you’re looking at $50–$100 per year (often less) through your regular auto insurer—money well spent if an accident happens in those first couple of years when you owe far more than the car is worth.

The smartest move is to get quotes from your current insurance provider first, compare them to any dealer or lender offer, and decide based on your down payment, loan length, and comfort level with risk. Check your car’s value against the loan balance every 12 months so you can drop the coverage the moment it’s no longer needed.