Introduction

Florida is a beautiful state with sunny beaches, warm weather, and a growing population. But living in the Sunshine State also comes with unique risks. Hurricanes, flooding, car accidents, and rising property costs all play a role in how much insurance you truly need.

If you have ever wondered how much insurance you should carry in Florida, you are not alone. Millions of residents ask the same question every year. This article will walk you through the different types of insurance you need in Florida, how much coverage makes sense, and how to avoid common mistakes that could leave you unprotected when it matters most.

Whether you are a new resident, a first-time homeowner, or simply trying to understand your options, this guide will give you clear and practical answers.

What Is Insurance and Why Does It Matter in Florida?

Insurance is a contract between you and an insurance company. You pay a regular amount of money, called a premium. In return, the company agrees to help pay for certain losses or damages.

Think of insurance as a safety net. If something bad happens, like a car crash or a hurricane damaging your home, insurance helps cover the cost so you do not have to pay for everything out of your own pocket.

In Florida, insurance is especially important because of several factors:

- Florida has one of the highest rates of car accidents in the United States.

- The state is highly vulnerable to hurricanes, tropical storms, and flooding.

- Healthcare costs continue to rise across the country, including in Florida.

- Florida law requires certain types of insurance coverage for drivers and, in some cases, for homeowners with a mortgage.

- The cost of home repairs and rebuilding after storms can be extremely high.

- Florida has a large population of retirees who need specific types of health and life coverage.

Understanding the basics of insurance helps you make smart financial decisions. It also ensures you are following Florida law.

Insurance in Florida is not just about meeting legal requirements. It is about protecting your family, your home, your car, and your financial future. Without proper coverage, a single unexpected event could wipe out your savings or put you in serious debt.

The types of insurance most Florida residents need include auto insurance, homeowners insurance, flood insurance, health insurance, and sometimes life insurance or umbrella insurance. Each one serves a different purpose, and the amount of coverage you need depends on your personal situation.

Let us break down each type so you can understand exactly what you need and how much is enough.

How Does Insurance Work in Florida?

Table of Contents

Table of Contents

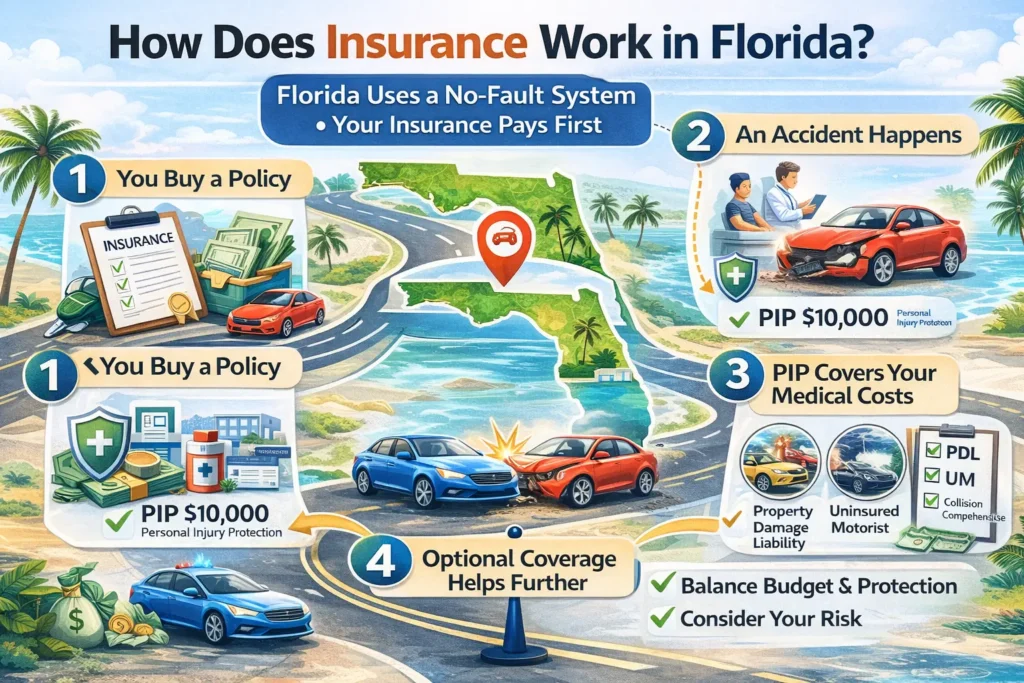

Insurance in Florida works similarly to other states, but there are some important differences. Here is a simple step-by-step breakdown of how the process works:

Step 1: Choose the Type of Insurance You Need

Start by identifying the risks you face. If you own a car, you need auto insurance. If you own a home, you need homeowners insurance. If you live in a flood zone, you likely need flood insurance too.

Florida has specific requirements for some of these, which we will cover in detail below.

Step 2: Compare Insurance Providers

Florida has many insurance companies. Some are national brands, and others are Florida-only companies. It is smart to compare quotes from at least three to five providers before choosing one.

Look at more than just the price. Pay attention to the coverage limits, deductibles, customer reviews, and how the company handles claims. A cheap policy that does not pay out when you need it is not a good deal.

Step 3: Select Your Coverage Amounts

Each type of insurance lets you choose how much coverage you want. Higher coverage means better protection, but it also means a higher premium. You need to find the right balance between what you can afford and what will protect you adequately.

In Florida, certain minimums are required by law. However, those minimums are often not enough to fully protect you. We will go over recommended amounts for each type of insurance.

Step 4: Pay Your Premium

Once you select a plan, you pay your premium. This can be monthly, quarterly, or annually. Most people choose monthly payments because it is easier to budget.

Keep in mind that missing a payment can cause your policy to lapse, which means you would be uninsured. In Florida, driving without insurance can lead to fines and license suspension.

Step 5: File a Claim When Needed

If something happens, like a car accident or storm damage, you contact your insurance company and file a claim. The company reviews your claim, and if it is covered under your policy, they help pay for the repairs or losses.

The amount you receive depends on your coverage limits and your deductible, which is the amount you pay out of pocket before the insurance kicks in.

Step 6: Review and Update Your Coverage Regularly

Your insurance needs can change over time. Maybe you bought a new car, moved to a new home, or had a baby. It is a good habit to review your policies at least once a year and make adjustments as needed.

In Florida, this is especially important because insurance rates and requirements can change frequently due to new laws and weather-related risks.

Types of Insurance You Need in Florida and How Much Coverage to Carry

Let us go through each major type of insurance Florida residents should consider.

Auto Insurance in Florida

Florida law requires all drivers to carry the following minimum auto insurance:

- Personal Injury Protection (PIP): $10,000

- Property Damage Liability (PDL): $10,000

Florida is a no-fault state. This means your own PIP coverage pays for your medical bills after an accident, regardless of who caused it.

However, these minimums are very low. Here is what most experts recommend:

- Bodily Injury Liability: $100,000 per person and $300,000 per accident. Florida does not require this, but it protects you if you injure someone else in an accident. Without it, you could be personally responsible for their medical bills.

- Uninsured/Underinsured Motorist Coverage: $100,000 per person and $300,000 per accident. Florida has a high number of uninsured drivers. This coverage protects you if you are hit by someone who does not have enough insurance.

- Collision Coverage: Enough to cover the value of your car. This pays for damage to your car from an accident.

- Comprehensive Coverage: Enough to cover the value of your car. This pays for damage from things like theft, vandalism, or falling objects.

If you only carry the state minimums, you are taking a big risk. A serious accident could easily cost more than $10,000 in property damage or medical bills. Without adequate coverage, you could end up paying thousands of dollars out of pocket.

Homeowners Insurance in Florida

Florida does not legally require homeowners insurance. However, if you have a mortgage, your lender will almost certainly require it.

Even if you own your home outright, homeowners insurance is strongly recommended. Here is what a standard policy typically covers:

- Dwelling Coverage: This pays to repair or rebuild your home if it is damaged. You should carry enough to cover the full replacement cost of your home, not just the market value.

- Personal Property Coverage: This covers your belongings, like furniture, electronics, and clothing. A typical recommendation is 50 to 70 percent of your dwelling coverage amount.

- Liability Coverage: This protects you if someone is injured on your property. Most experts recommend at least $300,000 to $500,000 in liability coverage.

- Additional Living Expenses: This pays for temporary housing if your home is uninhabitable after a covered event.

In Florida, homeowners insurance is more expensive than in most other states. This is largely because of the risk of hurricanes. Some policies may exclude wind damage or have separate hurricane deductibles, so read your policy carefully.

A typical Florida homeowner pays between $3,000 and $10,000 per year for insurance, depending on the location, age of the home, and coverage amounts. Homes in coastal areas or flood zones tend to cost more to insure.

Flood Insurance in Florida

Here is something many people do not realize: standard homeowners insurance does not cover flood damage.

In Florida, this is a critical gap. The state is one of the most flood-prone in the country. Even areas that are not in a designated flood zone can experience flooding from heavy rain or tropical storms.

If you live in a FEMA-designated high-risk flood zone and have a federally backed mortgage, flood insurance is required. But even if it is not required for you, it is highly recommended.

You can purchase flood insurance through the National Flood Insurance Program (NFIP) or through private insurers. Here are the coverage limits through the NFIP:

- Building Coverage: Up to $250,000 for residential properties

- Contents Coverage: Up to $100,000

If your home is worth more than $250,000, you may need a supplemental private flood policy to cover the difference.

The average cost of flood insurance in Florida ranges from about $700 to over $2,000 per year, depending on your flood zone and the elevation of your home.

Many Floridians skip flood insurance because they think their area is safe. But more than 40 percent of NFIP flood claims come from outside high-risk flood zones. It is worth the investment.

Health Insurance in Florida

Health insurance is essential for everyone, but Florida does not have a state mandate requiring you to carry it. The federal individual mandate penalty was reduced to zero starting in 2019.

However, going without health insurance is risky. A single hospital visit can cost tens of thousands of dollars.

Here are some options for health insurance in Florida:

- Employer-Sponsored Insurance: If your employer offers health insurance, this is often the most affordable option.

- Marketplace Plans: You can buy health insurance through the federal Health Insurance Marketplace at Healthcare.gov. Depending on your income, you may qualify for subsidies that lower your monthly premium.

- Medicaid: If your income is very low, you may qualify for Medicaid, which provides free or low-cost health coverage.

- Medicare: If you are 65 or older, or if you have certain disabilities, you may qualify for Medicare.

When choosing a health plan, consider the following:

- Monthly premium

- Deductible

- Out-of-pocket maximum

- Network of doctors and hospitals

- Prescription drug coverage

A good health insurance plan should cover major medical expenses without leaving you with crushing bills. Aim for a plan with a reasonable deductible and an out-of-pocket maximum that you could afford in a worst-case scenario.

Life Insurance

Florida does not require life insurance, but it can be an important part of your financial plan, especially if you have dependents.

Life insurance pays a benefit to your beneficiaries if you pass away. There are two main types:

- Term Life Insurance: Covers you for a specific period, like 10, 20, or 30 years. It is more affordable and straightforward.

- Whole Life Insurance: Covers you for your entire life and builds cash value over time. It is more expensive.

A common recommendation is to carry life insurance equal to 10 to 15 times your annual income. For example, if you earn $50,000 per year, you might want $500,000 to $750,000 in coverage.

This ensures your family can maintain their standard of living, pay off debts, and cover future expenses like college tuition if something happens to you.

Umbrella Insurance

Umbrella insurance provides extra liability coverage beyond what your auto and homeowners policies offer. It kicks in when you exceed the limits of your other policies.

For example, if you cause a car accident and the other person’s medical bills total $500,000, but your auto insurance only covers $300,000, an umbrella policy would cover the remaining $200,000.

Umbrella policies are relatively affordable. A $1 million umbrella policy typically costs between $150 and $300 per year.

This type of insurance is especially valuable if you have significant assets to protect, such as a home, savings, or investments.

Do You Know What Is How Much Is Gap Insurance on a New Car?

Real-Life Example: How Much Insurance Does a Typical Florida Family Need?

Let us look at a realistic example to put everything into perspective.

Meet the Johnsons. They are a family of four living in Tampa, Florida. Here is their situation:

- They own a home valued at $350,000.

- They have two cars, each worth about $25,000.

- Their combined household income is $90,000 per year.

- They live in a moderate flood risk zone.

- They have two young children.

Here is what their insurance might look like:

Auto Insurance (for two cars):

- Bodily Injury Liability: $100,000 per person / $300,000 per accident

- Property Damage Liability: $50,000

- PIP: $10,000 (required)

- Uninsured Motorist: $100,000 / $300,000

- Collision and Comprehensive: Full coverage on both cars

- Estimated annual cost: $4,000 to $6,000

Homeowners Insurance:

- Dwelling Coverage: $350,000 (full replacement cost)

- Personal Property: $175,000 (50 percent of dwelling)

- Liability: $300,000

- Hurricane Deductible: 2 percent of dwelling coverage ($7,000)

- Estimated annual cost: $4,000 to $7,000

Flood Insurance:

- Building Coverage: $250,000

- Contents Coverage: $100,000

- Estimated annual cost: $800 to $1,500

Health Insurance:

- Employer-sponsored plan for the family

- Estimated annual cost (employee share): $6,000 to $12,000

Life Insurance:

- Term life policy for each parent: $500,000 each (about 10 times half their income)

- Estimated annual cost: $600 to $1,200 for both policies

Umbrella Insurance:

- $1 million umbrella policy

- Estimated annual cost: $200 to $350

Total estimated annual insurance cost for the Johnsons: $15,600 to $28,050

That might seem like a lot, but consider this: a single hurricane could cause $200,000 or more in damage to their home. A serious car accident could result in $500,000 in medical bills. Without insurance, these events could bankrupt the family.

Insurance is not just a monthly bill. It is a financial shield that protects everything you have worked hard to build.

Why Is Knowing How Much Insurance You Need in Florida So Important?

Understanding your insurance needs in Florida is crucial for several reasons.

Protection from Natural Disasters

Florida faces hurricanes, tropical storms, flooding, and even sinkholes. These events can cause massive damage to homes and property. Without the right insurance, you could lose everything.

In 2022 alone, Hurricane Ian caused over $100 billion in damage across Florida. Many families who were underinsured struggled to rebuild.

Financial Security

Insurance prevents unexpected events from draining your savings or putting you in debt. Medical bills, car repairs, and home damage can add up fast. With proper coverage, you share that financial burden with your insurance company.

Legal Compliance

Florida requires minimum auto insurance for all drivers. If you are caught without it, you could face fines, license suspension, and even vehicle impoundment.

Mortgage lenders also require homeowners insurance and, in many cases, flood insurance. Failing to maintain these policies could put your loan in default.

Peace of Mind

Knowing you have adequate insurance lets you focus on living your life without constant worry. If a storm rolls in or you are involved in an accident, you know you have a plan in place.

Protecting Your Family

If you have a spouse, children, or other dependents, your insurance choices directly affect their well-being. Life insurance, health insurance, and adequate auto coverage all play a role in keeping your family safe and financially stable.

Pros and Cons of Carrying More Insurance in Florida

Like most financial decisions, choosing how much insurance to carry involves trade-offs. Here is a balanced look at the pros and cons.

Pros:

- Greater financial protection in the event of a major loss

- Less out-of-pocket expense after an accident, storm, or health issue

- Compliance with Florida law and mortgage requirements

- Protection of your assets, including your home and savings

- Peace of mind for you and your family

- Better coverage for lawsuits and liability claims

- Ability to recover faster after a disaster

Cons:

- Higher monthly or annual premiums

- May be paying for coverage you never use

- Can be confusing to understand all the different policy types and options

- Some policies have exclusions that may not be obvious at first

- Florida insurance rates are among the highest in the nation, making comprehensive coverage expensive

- Deductibles can still be high, especially for hurricane-related claims

- Shopping for and comparing insurance takes time and effort

The key is to find the right balance. You do not want to be overinsured and waste money, but you definitely do not want to be underinsured and face financial ruin after a major event.

Common Mistakes People Make with Insurance in Florida

Even well-intentioned people make mistakes when it comes to insurance. Here are some of the most common ones to watch out for.

Mistake 1: Only Carrying the State Minimum Auto Insurance

Florida’s minimum requirements of $10,000 in PIP and $10,000 in property damage liability are extremely low. A fender bender can easily exceed $10,000 in damage. A serious accident with injuries could cost hundreds of thousands of dollars. If your coverage falls short, you are personally responsible for the rest.

Many financial experts recommend carrying at least $100,000/$300,000 in bodily injury liability and $50,000 or more in property damage liability.

Mistake 2: Assuming Homeowners Insurance Covers Floods

This is one of the most common and costly misunderstandings in Florida. Standard homeowners insurance policies do not cover flood damage. You need a separate flood insurance policy.

Many homeowners only realize this after a flood has already damaged their property. By then, it is too late.

Mistake 3: Not Reviewing Your Policy Each Year

Your life changes, and your insurance should change with it. If you renovate your home, buy a new car, have a baby, or change jobs, your coverage needs may be different. Failing to update your policies can leave gaps in your protection.

Set a reminder to review all of your insurance policies at least once a year, or whenever a major life event occurs.

Mistake 4: Choosing the Cheapest Policy Without Reading the Details

A low premium is attractive, but it often means less coverage, higher deductibles, or more exclusions. Always read the full policy document and understand what is covered and what is not before you sign up.

Pay special attention to hurricane deductibles in Florida. These are often calculated as a percentage of your dwelling coverage rather than a flat dollar amount, which can mean a much higher out-of-pocket cost than you expect.

Mistake 5: Skipping Umbrella Insurance

Many people think umbrella insurance is only for wealthy individuals. In reality, it is affordable and provides an extra layer of protection that can save you from financial disaster. If you are ever sued for more than your auto or homeowners policy covers, an umbrella policy fills the gap.

For just a few hundred dollars a year, you can add $1 million or more in additional liability coverage.

Mistake 6: Not Understanding Your Deductible

Your deductible is the amount you pay out of pocket before your insurance starts covering costs. In Florida, hurricane deductibles can be particularly high. For example, a 2 percent hurricane deductible on a $400,000 home means you pay the first $8,000 of hurricane damage yourself.

Make sure you have enough savings to cover your deductible if you ever need to file a claim.

Mistake 7: Ignoring Sinkhole Coverage

Parts of Florida, especially Central Florida, are prone to sinkholes. Standard homeowners insurance may not cover sinkhole damage. Some policies cover catastrophic ground cover collapse but not all types of sinkhole activity.

If you live in an area with a history of sinkholes, ask your insurance agent about adding sinkhole coverage to your policy.

Frequently Asked Questions (FAQs)

What is the minimum car insurance required in Florida?

Florida requires all drivers to carry at least $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). However, these minimums are very low and may not be enough to cover the costs of a serious accident. Most experts recommend carrying much higher limits, including bodily injury liability and uninsured motorist coverage.

Do I need flood insurance in Florida if I am not in a flood zone?

While flood insurance is only required if you live in a FEMA-designated high-risk flood zone and have a federally backed mortgage, it is strongly recommended for all Florida residents. Flooding can happen anywhere, not just in high-risk areas. In fact, a significant percentage of flood insurance claims come from properties outside designated flood zones.

How much homeowners insurance do I need in Florida?

You should carry enough dwelling coverage to fully rebuild your home at current construction costs. This is called the replacement cost, and it may be different from your home’s market value. You should also have adequate personal property coverage, liability coverage of at least $300,000, and a separate flood insurance policy.

Is life insurance required in Florida?

No, Florida does not require anyone to carry life insurance. However, if you have dependents who rely on your income, life insurance is an important way to protect their financial future. A common guideline is to carry 10 to 15 times your annual income in term life insurance.

Why is insurance so expensive in Florida?

Florida insurance rates are among the highest in the nation for several reasons. The state faces frequent hurricanes and tropical storms, which drive up homeowners insurance costs. Florida also has a high rate of car accidents and insurance fraud, which affects auto insurance premiums. Additionally, the cost of construction materials and labor for repairs has risen significantly in recent years.

Can I bundle my insurance policies to save money?

Yes, many insurance companies offer discounts when you bundle multiple policies together, such as auto and homeowners insurance. Bundling can save you anywhere from 5 to 25 percent on your premiums. It also simplifies your insurance management since you deal with one company for multiple policies.

Conclusion

Figuring out how much insurance you need in Florida does not have to be overwhelming. The key is to understand the risks you face, know what the state requires, and then go beyond the minimums to truly protect yourself and your family.

At a minimum, make sure you have auto insurance that goes well beyond the state requirements, homeowners insurance that covers the full replacement cost of your home, and a separate flood insurance policy. Consider adding health insurance, life insurance, and an umbrella policy to round out your coverage.

Florida is a wonderful place to live, but it comes with unique challenges. Hurricanes, floods, and high accident rates mean that having the right insurance is not optional. It is essential.

Take the time to review your current policies, compare quotes from multiple providers, and make sure you are not leaving gaps in your coverage. A little effort now can save you from major financial hardship down the road.

The best insurance plan is one that fits your specific needs, protects your assets, and gives you confidence that you and your loved ones are covered no matter what comes your way.