Introduction

Buying a new car or replacing an old one is exciting, but it also comes with practical tasks. One important step is transferring your car insurance to the new vehicle. Many drivers in the United States wonder how much this process costs and whether there are extra fees involved. Understanding this can help you avoid surprises and keep your coverage active without gaps.

This article explains how much it costs to transfer insurance to another car, how the process works, and what factors affect the price. You will also learn common mistakes to avoid and simple tips to make the transition smooth and affordable.

What is the Cost to Transfer Insurance to Another Car?

Table of Contents

Table of Contents

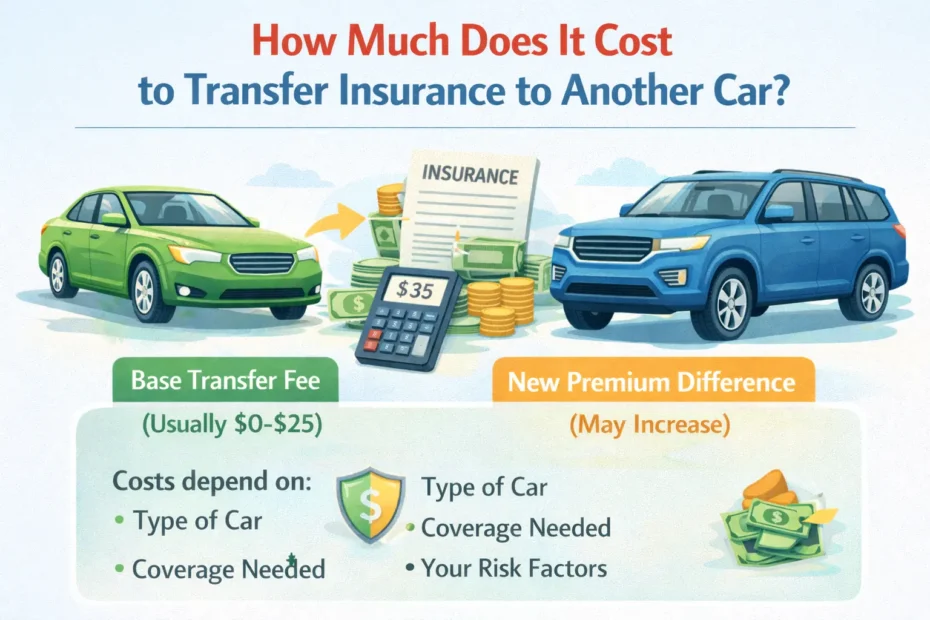

The cost to transfer insurance to another car refers to the amount you may pay when you replace one insured vehicle with another on your existing auto insurance policy.

In many cases, the transfer itself is free. However, your total insurance cost may change depending on the new car and your risk profile.

Here’s what usually happens:

- Your insurance company removes the old car from your policy.

- The new vehicle is added to the same policy.

- Your premium is recalculated based on the new car.

Possible costs involved include:

- Policy adjustment fees (usually $0–$25)

- Changes in monthly premium

- Additional coverage upgrades if required

The biggest cost difference usually comes from the type of car you insure, not the transfer process itself.

How Does the Cost to Transfer Insurance to Another Car Work?

The process is simple and usually takes less than one day. Below is a step-by-step explanation.

Step 1: Contact Your Insurance Company

Call or log into your insurer’s website and inform them you are changing vehicles. You will need basic details about the new car.

Step 2: Provide Vehicle Information

You may be asked for:

- Vehicle Identification Number (VIN)

- Make, model, and year

- Purchase date

- Mileage and usage

Step 3: Coverage Review

The insurer checks whether your current coverage fits the new vehicle. For example, a financed car may require full coverage.

Step 4: Premium Recalculation

Your insurance company calculates the updated rate based on:

- Car value

- Repair costs

- Safety features

- Theft risk

Step 5: Pay Any Difference

You may:

- Pay extra if the new car costs more to insure, or

- Receive a small refund if it costs less.

Once completed, your insurance continues without interruption.

Real-Life Example

Let’s look at a realistic situation.

Sarah owns a 2014 sedan insured for $110 per month. She sells it and buys a newer 2022 SUV.

When she transfers her insurance:

- Transfer fee: $0

- New monthly premium: $145

- Difference: $35 more per month

Why did the price increase?

- The SUV has a higher market value.

- Repair costs are more expensive.

- Comprehensive and collision coverage limits increased.

In another case, Mike switches from a sports car to a used compact car.

- Old premium: $180 per month

- New premium: $120 per month

- Result: He saves $60 monthly.

These examples show that the vehicle type matters more than the transfer itself.

Do You Know What Is How Much Does Lawn Care Insurance Cost?

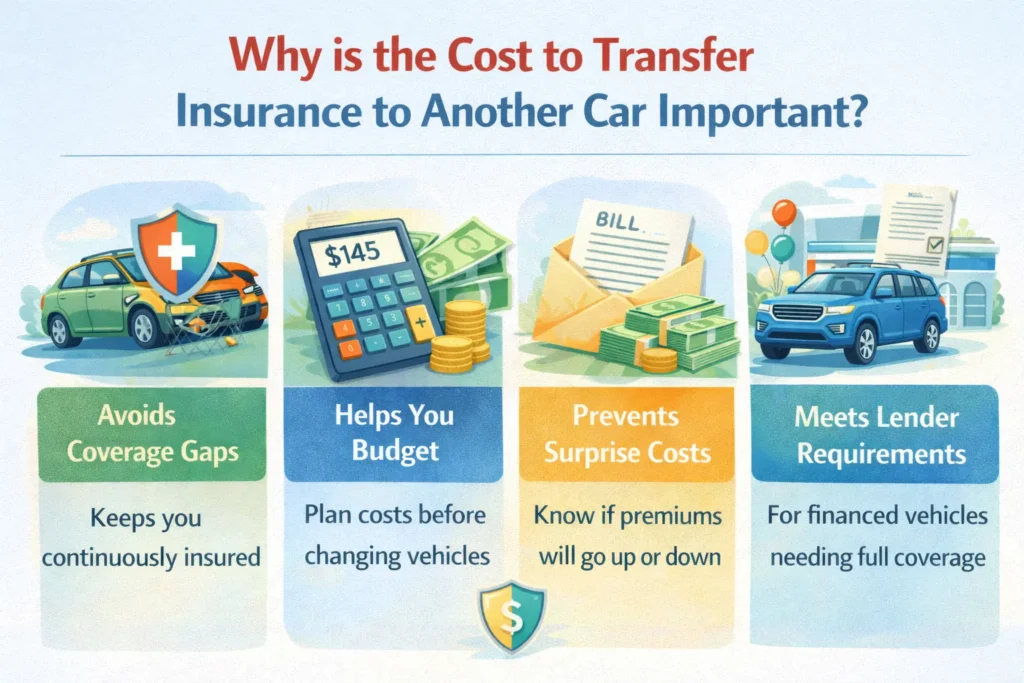

Why is the Cost to Transfer Insurance to Another Car Important?

Understanding this cost helps drivers make smarter financial decisions.

Here’s why it matters:

- Prevents coverage gaps that could leave you uninsured.

- Helps you budget before buying a new vehicle.

- Avoids surprise premium increases.

- Ensures your lender requirements are met if the car is financed.

- Keeps your driving record continuous, which may protect discounts.

Many people focus only on the car price but forget insurance changes. Knowing the potential cost ahead of time helps you choose a vehicle that fits your budget long term.

Pros and Cons of Transferring Insurance to Another Car

Pros

- Quick and easy process

- Usually no cancellation needed

- Maintains your insurance history

- May qualify for loyalty discounts

- Avoids new policy setup paperwork

Cons

- Premium may increase unexpectedly

- Some vehicles require higher coverage

- Small administrative fees may apply

- Limited time window after buying a car

Overall, transferring insurance is usually simpler and cheaper than starting a completely new policy.

Common Mistakes People Make

Many drivers misunderstand how insurance transfers work. Here are common mistakes to avoid:

- Waiting too long to notify the insurer

Some drivers assume coverage automatically transfers. Always confirm immediately. - Not checking the new premium first

A newer car may cost much more to insure. - Dropping coverage before adding the new vehicle

This can create a coverage gap. - Ignoring coverage requirements

Lenders often require full coverage for financed cars. - Forgetting to remove the old vehicle

You might continue paying for a car you no longer own.

Taking a few minutes to review your policy can prevent these problems.

Frequently Asked Questions (FAQs)

Does it cost money to transfer car insurance to another car?

Usually, no. Most insurers allow free transfers, but your premium may change based on the new vehicle.

Can I drive my new car before transferring insurance?

Many companies offer a short grace period, but you should contact your insurer immediately to confirm coverage.

Will my insurance go up when I change cars?

It depends on the vehicle. Newer, faster, or more expensive cars typically cost more to insure.

How long does it take to transfer insurance?

In most cases, it can be completed within minutes online or during a short phone call.

Conclusion

Transferring insurance to another car is a normal part of buying or replacing a vehicle, and the process is usually simple. While the transfer itself often costs little or nothing, your insurance premium may increase or decrease depending on the car you choose.

Before purchasing a vehicle, it’s smart to request an insurance quote so you understand the full cost of ownership. Acting quickly, reviewing coverage carefully, and asking questions can help you avoid surprises. With the right preparation, transferring insurance can be smooth, affordable, and stress-free.