Introduction:

If you own a home in the United States, there’s an overwhelming chance that your insurance policy is an HO-3 insurance policy—even if you’ve never heard the term before. Often referred to as a “Special Form” policy, the HO-3 is the gold standard of home insurance, striking a balance between comprehensive protection and affordability.

However, “standard” doesn’t mean “simple.” Understanding the nuances of your HO-3 coverage is the best way to avoid costly surprises when disaster strikes. This guide will break down everything you need to know, from what is covered and what is excluded to smart money-saving tips that keep your biggest investment safe.

Table of Contents

Table of Contents

What Is an HO-3 Insurance Policy?

An HO-3 insurance policy is a form of homeowners insurance that offers “open peril” (or “all-risk”) coverage for the structure of your home and “named peril” coverage for your personal belongings.

- For Your House: The dwelling is protected against any risk that is not specifically listed as an exclusion in the policy. If it’s not written in the contract as “not covered,” it’s covered.

- For Your Belongings: Your furniture, clothes, and electronics are covered only if they are damaged by perils specifically named in the policy (like fire or theft).

This hybrid approach is why the HO-3 is the most common homeowners insurance policy in the US. It offers robust protection for your home’s structure while keeping premiums manageable.

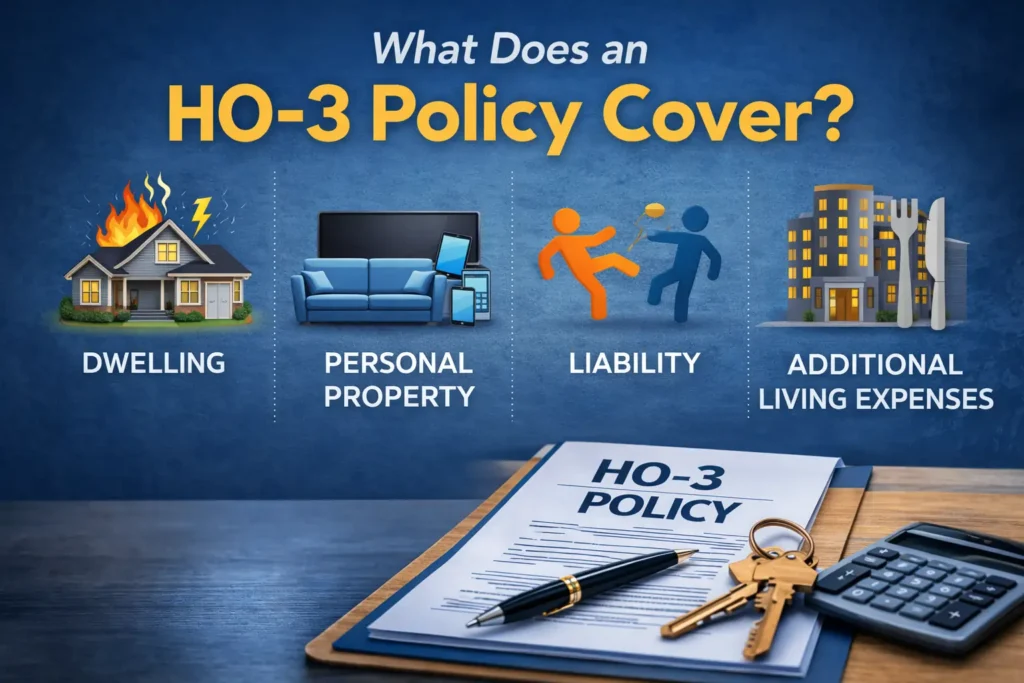

What Does an HO-3 Policy Cover?

An HO-3 policy is actually a package of several different coverages bundled into one. These are identified by the letters A, B, C, D, E, and F on your “Declarations Page” (the first page of your policy).

1. Coverage A: Dwelling Coverage (Your House)

This is the most important part of the policy. It covers the physical structure of your home—the walls, roof, and built-in appliances. Because it is open-peril coverage, your home is protected against sudden and accidental damage from almost any source, including the standard 16 perils:

- Fire or lightning

- Windstorm or hail

- Explosion

- Riot or civil commotion

- Damage from aircraft or vehicles

- Smoke

- Vandalism or malicious mischief

- Theft

- Volcanic eruption

- Falling objects

- Weight of ice, snow, or sleet

- Accidental discharge or overflow of water or steam (from plumbing, HVAC, or appliances)

- Sudden and accidental tearing apart, cracking, burning, or bulging of a steam or hot water system

- Freezing of plumbing systems

2. Coverage B: Other Structures

This covers structures on your property that are not attached to your main house, such as:

- Detached garages

- Sheds and tool sheds

- Fences

- Guest houses

- Driveways and sidewalks

Typically, this coverage is set at 10% of your Dwelling (Coverage A) limit.

Do you know What are the top rated home insurence provider in usa?

3. Coverage C: Personal Property Coverage

This covers your belongings—furniture, electronics, clothing, and sports equipment. Unlike your dwelling, this is “named-perils” coverage. It is only covered if damaged by one of the perils listed above (like fire, theft, or wind).

Important Note: There are often sub-limits on high-value items. For example, a standard HO-3 might only cover $1,500 for jewelry loss or $2,500 for silverware theft. If you own expensive engagement rings or art, you will likely need a special endorsement (a “rider” or “floater”).

4. Coverage D: Additional Living Expenses (ALE)

If a covered disaster (like a fire) makes your home uninhabitable, ALE coverage pays for the extra costs of living elsewhere while your home is being repaired.

- What it covers: Hotel bills, restaurant meals, pet boarding, and temporary rental costs.

- What it doesn’t cover: Your normal mortgage payment or utility bills.

5. Coverage E: Personal Liability Protection

This is one of the most critical parts of your HO-3 policy. It protects you if someone is injured on your property or if you accidentally cause damage to someone else’s property.

- Medical bills: If a guest falls on your steps, this pays their hospital bills (usually regardless of fault).

- Legal defense: If you are sued, the insurance company pays for your lawyers and court costs.

- Judgments: If you are found liable, the policy pays for the settlement up to your coverage limit (usually $100,000 to $500,000).

6. Coverage F: Medical Payments to Others

This is a “no-fault” coverage that pays for minor medical expenses for guests injured on your property, regardless of who was at fault. It helps resolve small issues before they become lawsuits.

What Is NOT Covered by an HO-3 Policy? (Exclusions)

While HO-3 coverage is broad, it is not a blank check. Insurance is designed for sudden and accidental damage, not for maintenance issues or catastrophic earth movements. Here is what is usually excluded:

The “Big Two” Catastrophes

- Flood Damage: Rising water from rivers, storms surges, or heavy rain seeping through the foundation is never covered by a standard HO-3. You need a separate flood insurance policy through FEMA’s NFIP or a private insurer.

- Earthquake Damage: Shifting, sinking, or trembling earth is excluded. You need separate earthquake insurance or an endorsement.

Maintenance-Related Issues

- Wear and Tear: Roofs get old, paint peels, pipes rust. Insurance covers sudden failure, not gradual deterioration.

- Pest Infestations: Termites, bed bugs, rodents, and carpenter ants are your responsibility.

- Mold, Rot, or Fungi: Generally excluded unless it is the direct result of a covered peril (like a burst pipe that was suddenly fixed). “Long-term” leaks that cause mold are not covered.

- Sewer or Drain Backups: If the city sewer line backs up into your basement, it is usually excluded unless you purchase a specific Water Backup Endorsement.

Do you know How Much Dose home insurence Cost in usa?

Intentional Acts

- Intentional Damage: If you or a family member intentionally damages the home, it is not covered.

- Acts of War or Nuclear Hazard: Standard exclusions in almost all insurance contracts.

HO-3 vs. HO-1, HO-2, and HO-5: What’s the Difference?

Understanding where the HO-3 fits in the market helps you realize why it is so popular.

| Policy Type | Nickname | Structure Coverage | Belongings Coverage | Best For |

|---|---|---|---|---|

| HO-1 | Basic Form | Named Peril (very limited) | Named Peril | Rarely used/obsolete. |

| HO-2 | Broad Form | Named Peril (more than HO-1) | Named Peril | Older homes or strict budgets. |

| HO-3 | Special Form | Open Peril | Named Peril | The vast majority of homeowners. |

| HO-5 | Comprehensive Form | Open Peril | Open Peril | High-value homes; more expensive. |

The Takeaway: The HO-3 upgrades your house to “Open Peril” protection, which is why most lenders and agents recommend it. The HO-5 extends that same broad protection to your sofa and TV, but it costs significantly more.

5 Smart Tips for HO-3 Policyholders

Don’t just buy the policy and forget it. Being a smart homeowner means actively managing your coverage.

1. Insure for the Rebuild Cost, Not the Market Value

Your home might be worth $500,000 on the real estate market, but the cost to rebuild it after a total loss might only be $300,000 (or it could be higher due to supply costs).

- Action: Review your Coverage A limit annually. Is it enough to cover current construction costs in your area?

2. Consider Replacement Cost vs. Actual Cash Value

Standard HO-3 policies pay for Replacement Cost Value (RCV) for your house, but often pay Actual Cash Value (ACV) for your belongings unless you upgrade.

- ACV: Reimburses you for the value of the item minus depreciation. (A 10-year-old TV gets you very little money).

- RCV: Reimburses you for the cost to buy a new TV of similar kind and quality.

- Action: Check if your “Coverage C” is RCV. If not, paying a little extra to upgrade is usually worth it.

3. Add Critical Endorsements (Endorsements)

Because the HO-3 excludes so much, you can buy back coverage with endorsements. The most important ones to ask your agent about are:

- Sewer and Water Backup: Inexpensive and essential for finished basements.

- Service Line Coverage: Covers the cost to repair the water or gas line from your house to the street.

- Ordinance or Law Coverage: If your old home is damaged and must be rebuilt to current building codes, this pays the extra cost. (This is often automatically included in modern HO-3 policies, but check the limit).

4. Create a Home Inventory

In the chaos following a fire or burglary, you won’t remember every shirt or pan you own.

- Action: Walk through your home with your phone and video record every drawer and closet. Open the pantry. Store this video in the cloud or with a relative. This is the single best tool for settling a personal property claim quickly.

5. Bundle for Discounts

Insurance companies love loyalty.

- Action: If you have an HO-3 policy, ask about bundling your auto insurance with the same company. This can save you 10-25% on both policies.

Why Understanding Your HO-3 Policy Matters

Insurance is a contract of adhesion—meaning you adhere to the terms. If you don’t know what those terms are, you might find yourself paying out of pocket for a loss you assumed was covered.

Reading your policy before a disaster helps you:

- Avoid Denied Claims: You won’t be shocked to learn a flood isn’t covered.

- Budget Better: You can plan for the separate flood or earthquake premiums.

- Protect Valuables: You can schedule that engagement ring before it gets lost, not after.

- Sleep Easier: You’ll have the confidence that your biggest asset is properly protected.

Your home is more than just a roof—it’s your sanctuary and your financial foundation. Make sure your HO-3 insurance policy is as strong as the home it protects.

How to Maximize Your HO-3 Claim: A Step-by-Step Strategy Guide

Filing an insurance claim is a stressful experience, but knowing the mechanics of your HO-3 insurance policy beforehand can transform a potential financial disaster into a manageable inconvenience. The key to a successful claim lies not in luck, but in preparation and understanding the “invisible” aspects of your coverage that most homeowners overlook.

The “Proof of Loss” Trap

When damage occurs, your insurance company will require a “Proof of Loss” document—essentially a sworn statement detailing the damage and its value. This is where many HO-3 policyholders stumble. Because your dwelling is covered on an “open peril” basis, the burden of proof is technically on the insurer to prove an exclusion applies. However, the burden of documenting the value is on you.

Actionable Tip: Do not rely on memory. Immediately after a loss, take extensive photos and videos before any cleanup begins. Create a written list of damaged items, including brands, model numbers, and approximate purchase dates. This documentation is your best defense against a lowball settlement.

Navigating the Depreciation Game

One of the most misunderstood aspects of an HO-3 policy is the difference between Actual Cash Value (ACV) and Replacement Cost Value (RCV). Most standard HO-3 policies settle claims on a “replacement cost basis” for your home, but personal property claims often start at ACV.

Here is how the process actually works:

- The Initial Check: You will likely receive an initial check for the ACV of your damaged belongings. For a five-year-old roof, this means the insurer deducts for age and wear.

- The Depreciation Holdback: The amount deducted is called “depreciation.” The insurance company holds this money back.

- Recovering the Depreciation: Once you actually repair or replace the item, you submit receipts to the insurer. They then release the “holdback” (depreciation) to you. This process is called “recoverable depreciation.”

Smart Strategy: Do not cash the first check and assume the matter is closed. Understand that the full replacement cost is only paid out after the work is done. Budget accordingly and keep every single receipt.

Do you know What are the Common Home insurence Mistakes?

The “Ordinance or Law” Loophole

Imagine your home suffers a minor kitchen fire. You have HO-3 coverage, so you assume you are fully protected. However, when the contractor begins repairs, they inform you that current building codes require you to upgrade the electrical wiring or add seismic bracing to the foundation. This added cost can be tens of thousands of dollars.

Your standard HO-3 policy may have a small allowance for this, often only 10% of your dwelling coverage, which may not be enough. This is known as “Ordinance or Law” coverage.

Proactive Measure: Check your policy declarations page for “Coverage OL.” If the limit seems low (or if it’s not listed at all), call your agent. Increasing this limit is relatively inexpensive but can save you from financial ruin if your home must be rebuilt to modern, stricter codes.

Why You Should Never Accept the First Offer

Insurance adjusters are professionals who handle claims daily. You, likely, do not. The first settlement offer from an insurance company is often a starting point for negotiation, not a final verdict.

If you receive a low offer, you have the right to:

- Hire a Public Adjuster: They work for you, not the insurance company, and can re-evaluate the damage.

- Get Your Own Contractor Quotes: Do not rely solely on the adjuster’s estimate. Independent contractor bids can provide leverage.

- Review the Policy Language: Understand the difference between “damage” and “cosmetic” issues. Some policies exclude cosmetic damage to things like roofs (e.g., matching shingles).

Frequently Asked Questions (FAQs)

Q1: Is an HO-3 policy required by law?

No, state laws do not require you to have homeowners insurance. However, if you have a mortgage, your lender will require you to carry an HO-3 (or similar) policy to protect their investment.

Q2: Does HO-3 cover roof leaks?

It depends on the cause of the leak. If a tree falls on the roof during a storm, yes. If the shingles are 20 years old and just worn out, no. The damage must be sudden and accidental, not due to wear and tear.

Q3: How do I know if I have an HO-3?

Look at the “Declarations Page” of your policy. It will usually state the form type (HO-3) in the top corner. If you are unsure, call your insurance agent and ask.

Q4: Does HO-3 cover mold?

Generally, no—unless the mold was caused by a “covered peril” that you took immediate steps to fix. For example, if a pipe bursts and you dry everything out immediately but a small patch of mold appears, it might be covered. If you had a slow leak for months, it will be denied.

Q5: What is the difference between HO-3 and HO-4?

An HO-3 is for homeowners. An HO-4 is a “Renters Insurance” policy for tenants.