Introduction

If you own a home, protecting it is one of your biggest financial responsibilities. Homeowners insurance helps with that, and one of its most important parts is dwelling coverage. This is the coverage that helps pay to repair or rebuild your house if it is damaged by events like fire, storms, or vandalism.

Many homeowners don’t fully understand what dwelling coverage includes, how much they need, or how claims actually work. That confusion can lead to being underinsured when disaster strikes. This guide explains dwelling coverage in simple terms, shows how it works, and helps you avoid common mistakes so you can better protect your home and your budget.

Table of Contents

Table of Contents

What is dwelling coverage?

Dwelling coverage is the part of your homeowners insurance policy that protects the physical structure of your home. If your house is damaged or destroyed by a covered event, this coverage helps pay to repair or rebuild it.

Think of it as protection for the building itself, not the things inside it.

What dwelling coverage usually includes

Dwelling coverage often protects:

- The walls, roof, and foundation

- Built-in cabinets and countertops

- Plumbing and electrical systems

- Heating and cooling systems

- Built-in appliances like furnaces and water heaters

- Attached structures such as garages, decks, or porches

If these parts of your home are damaged by a covered risk, your policy may help pay for repairs or rebuilding.

Do you know what is home ho-3 policy?

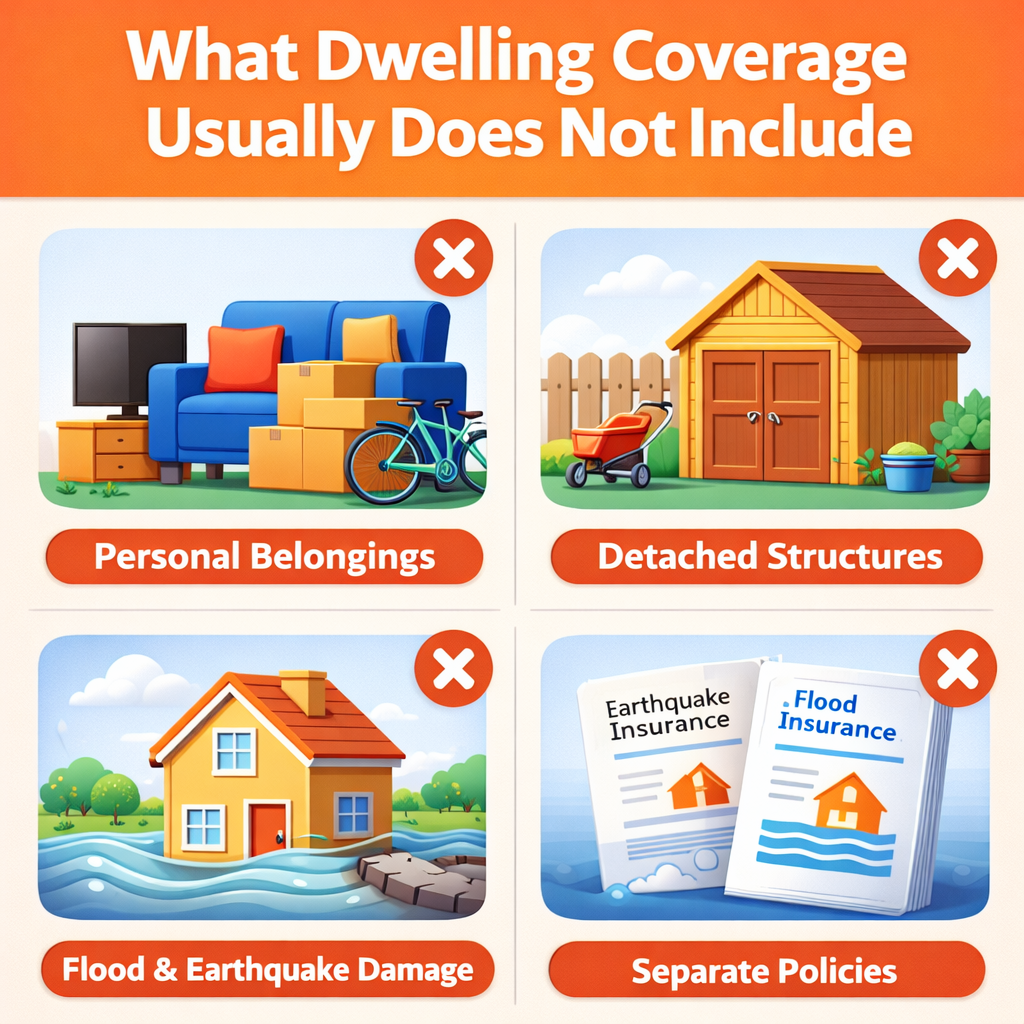

What dwelling coverage usually does NOT include

It’s just as important to know what is not covered:

- Furniture, clothing, and electronics (covered by personal property insurance)

- Detached structures like sheds or fences (covered by other structures coverage)

- Flood damage (requires separate flood insurance)

- Earthquake damage (requires separate earthquake coverage in many areas)

- Normal wear and tear or poor maintenance

Dwelling coverage is focused only on the structure and built-in parts of your house.

How does dwelling coverage work?

Dwelling coverage works by helping you recover financially after your home is damaged by a covered event. Here’s how the process usually works, step by step.

Step 1: You choose a dwelling coverage limit

When you buy a policy, you select a coverage limit. This is the maximum amount your insurer will pay to rebuild your home.

This number should be based on rebuilding cost, not the market value of your home. Market value includes the land and location, while dwelling coverage is about construction costs.

Step 2: A covered event damages your home

Covered events (also called perils) often include:

- Fire and smoke

- Windstorms and hail

- Lightning

- Explosions

- Vandalism

- Damage from vehicles or aircraft

If one of these events damages your home’s structure, dwelling coverage may apply.

Step 3: You file an insurance claim

After the damage, you contact your insurance company and file a claim. You may need to provide:

- Photos or videos of the damage

- A description of what happened

- A list of damaged areas

Step 4: An adjuster inspects the damage

The insurance company sends an adjuster to inspect your home. The adjuster estimates the cost to repair or rebuild the damaged parts of your house.

Step 5: You pay your deductible

Your deductible is the amount you pay out of pocket before insurance starts paying. For example, if your deductible is $1,500, you pay that amount first.

Step 6: Insurance pays the rest (up to your limit)

After your deductible, the insurance company pays for covered repairs up to your dwelling coverage limit. If costs go beyond that limit, you may have to pay the extra yourself.

Real-life example

Let’s look at a simple example.

Maria owns a home insured with:

- $350,000 in dwelling coverage

- A $2,000 deductible

A severe windstorm tears off part of her roof and damages an exterior wall. The total repair cost is $28,000.

Here’s what happens:

- Maria files a claim with her insurer.

- The adjuster confirms the damage is from a covered windstorm.

- Maria pays her $2,000 deductible.

- The insurance company pays the remaining $26,000.

Without dwelling coverage, Maria would have had to pay the full $28,000 herself. This example shows how dwelling coverage can protect homeowners from major financial stress.

Do you know what is AOB in home insurence?

Why is dwelling coverage important?

Dwelling coverage is important because rebuilding a home is very expensive. Even a small fire or storm can cause tens of thousands of dollars in damage.

It protects your biggest investment

For many people, their home is their most valuable asset. Dwelling coverage helps protect that investment if something unexpected happens.

It protects your savings

Without insurance, you might have to use savings, take out loans, or go into debt to pay for repairs. Dwelling coverage helps reduce that risk.

It helps you recover after disasters

Major events like fires, tornadoes, or hurricanes can make a home unlivable. Dwelling coverage helps make rebuilding possible.

Mortgage lenders usually require it

If you have a mortgage, your lender almost always requires dwelling coverage. This protects both you and the lender from large financial losses.

Do you know How to write an appeal letter insurence?

Pros and cons of dwelling coverage

Pros

- Helps pay to repair or rebuild your home

- Covers many common risks like fire and storms

- Protects your financial stability

- Often required for a mortgage

Cons

- Does not cover floods or earthquakes

- You must pay a deductible

- Coverage limits may not keep up with rising construction costs

- Excludes damage from poor maintenance

Dwelling coverage is essential, but it’s important to understand its limits.

Common mistakes people make

Many homeowners make simple mistakes that can lead to big problems later.

1. Insuring for market value instead of rebuild cost

Your home’s market value includes land and location. Dwelling coverage should be based on how much it would cost to rebuild the structure only.

2. Not updating coverage after renovations

If you remodel your kitchen or add a room, your rebuild cost goes up. If you don’t increase your dwelling limit, you could be underinsured.

3. Assuming all disasters are covered

Standard policies usually do not cover floods or earthquakes. Many homeowners learn this only after damage happens.

4. Choosing a high deductible without planning

A higher deductible lowers your premium, but you must be able to afford that amount if you file a claim.

5. Ignoring local building cost increases

Labor and materials can get more expensive over time. If your policy limit stays the same for years, it may no longer be enough.

Frequently asked questions (FAQs)

Is dwelling coverage the same as homeowners insurance?

No. Homeowners insurance includes several coverages. Dwelling coverage is just one part that protects the structure of the home.

Does dwelling coverage include my furniture?

No. Furniture and personal belongings are covered under personal property coverage, not dwelling coverage.

How do I know how much dwelling coverage I need?

You should estimate the cost to rebuild your home at current construction prices. An insurance agent or replacement cost calculator can help.

Does dwelling coverage pay for hotel stays?

No. Temporary living expenses are usually covered under “loss of use” or “additional living expenses,” which is a different part of your policy.

Conclusion

Dwelling coverage is one of the most important parts of your homeowners insurance policy. It protects the physical structure of your home and helps pay for repairs or rebuilding after covered damage. Without it, even a single serious event could create major financial hardship.

To stay protected, make sure your coverage limit reflects the real cost to rebuild your home, review it regularly, and understand what is and isn’t covered. A little knowledge about dwelling coverage today can save you from huge stress and expenses in the future.

Pingback: What Is Loss of Use Coverage? (Simple Definition) - Insurence policy tips

Pingback: Does Home Insurance Cover Water Damage From Appliances in 2026 ? - Insurence policy tips

Comments are closed.