Introduction

Home insurance is meant to protect your home, belongings, and finances. But many people misunderstand how it works. Small mistakes in choosing or managing a policy can lead to big problems later, especially during a claim.

Learning about common home insurance mistakes can help you avoid stress and unexpected costs. This article explains what these mistakes are, how they happen, and why they matter. You’ll also see a real-life example and get simple tips to make better decisions about your coverage.

What is common home insurance mistakes?

Table of Contents

Table of Contents

Common home insurance mistakes are errors people make when buying, using, or updating their homeowners insurance policy. These mistakes often happen because insurance terms can be confusing.

They may include:

- Choosing coverage that is too low

- Not understanding what the policy excludes

- Forgetting to update coverage after home changes

- Ignoring the deductible amount

These mistakes can leave homeowners underprotected when something goes wrong.

How does common home insurance mistakes work?

Home insurance mistakes usually happen step by step.

First, a homeowner buys a policy without fully understanding the details. They may focus only on the price and not the coverage limits.

Next, life changes happen. Maybe they renovate the kitchen or buy expensive electronics, but they do not update their policy.

Then, a disaster occurs, like a fire or major storm. When they file a claim, they learn their coverage is not enough or that certain damage is not covered. This leads to higher out-of-pocket costs than expected.

do you knbow what is mean by aob in home insuren ?

Real-life example

Imagine a homeowner insures their house for $200,000 because that was the purchase price. Over time, building costs rise, and the real cost to rebuild becomes $260,000.

A fire causes $180,000 in damage. Because the home was underinsured, the insurance payout may not fully cover the repairs after the deductible. The homeowner might have to pay tens of thousands of dollars themselves.

This situation often happens when people do not review and update their coverage.

Why is common home insurance mistakes important?

Avoiding home insurance mistakes can protect your savings and reduce stress during emergencies.

When your coverage matches your real needs, you are more likely to:

- Receive enough money to repair or rebuild your home

- Replace important belongings after a loss

- Avoid surprise costs during a claim

- Feel more confident about your financial protection

Understanding these mistakes helps you make smarter choices before problems happen.

Review Your Home Insurance Policy Every Year

Homeowners insurance is not something you should buy once and forget. Costs to rebuild homes often increase over time because of higher material and labor prices. If your coverage stays the same for years, it may no longer be enough.

Reviewing your policy once a year helps make sure your dwelling coverage, personal property limits, and liability protection still match your current needs.

Understand Natural Disaster Coverage Gaps

Not all disasters are covered by a standard homeowners insurance policy. This is one of the most common misunderstandings.

Typical policies usually do not cover:

- Flood damage

- Earthquakes

- Certain types of ground movement

If you live in a high-risk area, you may need separate policies or endorsements for full protection.

Check Coverage for Home-Based Businesses

Many people now work or run small businesses from home. Standard home insurance policies often have limits on business equipment and liability.

If you use your home for business, you may need extra coverage or a separate policy to stay fully protected.

Update Coverage After Home Improvements

Renovations and upgrades can increase the cost to rebuild your home. If you don’t update your policy, you could end up underinsured.

Be sure to tell your insurance company if you:

- Remodel a kitchen or bathroom

- Finish a basement

- Add a deck or room

Some upgrades, like a new roof or plumbing system, might even qualify you for discounts.

Pros and cons of common home insurance mistakes

Pros

- Can teach valuable lessons about coverage

- May encourage homeowners to review their policies more carefully

Cons

- Can lead to large out-of-pocket expenses

- May cause claim delays or partial payouts

- Can create financial stress after a disaster

- Might leave important items or risks uninsured

Common mistakes people make

- Underinsuring the home

Many people insure their home for market value instead of rebuilding cost. - Not reading the policy details

Skipping the fine print can lead to surprises about exclusions and limits. - Forgetting about high-value items

Jewelry, art, and collectibles may need extra coverage. - Choosing a deductible that is too high

A high deductible lowers premiums but can be hard to afford during a claim. - Not updating the policy after renovations

Home improvements often increase rebuilding costs and should be reported.

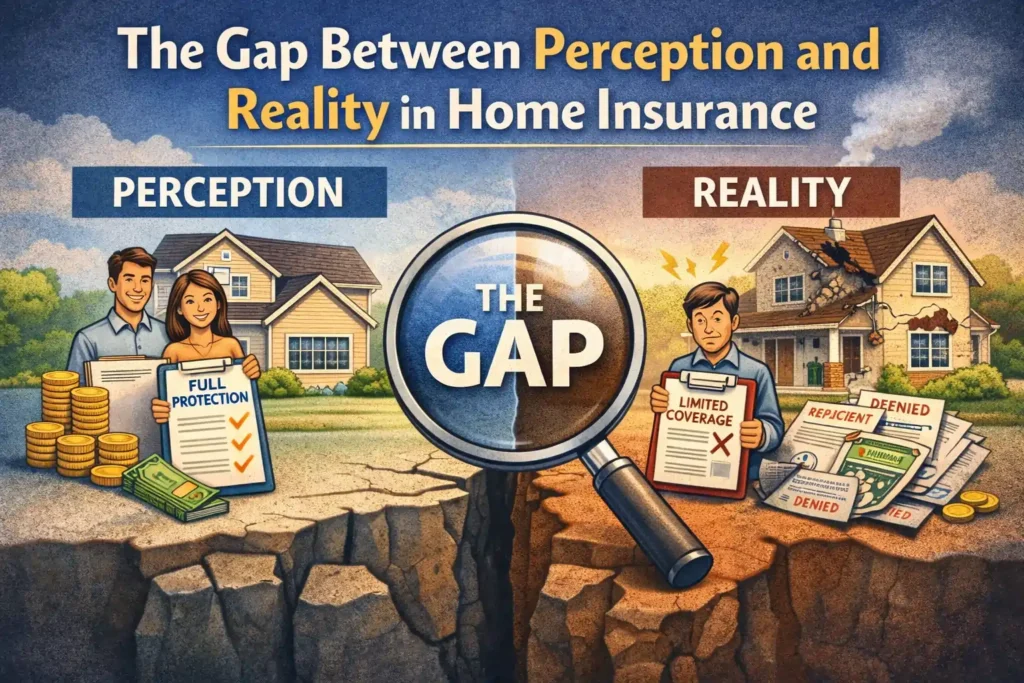

The Gap Between Perception and Reality in Home Insurance

Many homeowners believe that having any home insurance policy means they are fully protected. This belief is one of the most widespread and potentially costly misunderstandings in personal finance. The truth is that the level of protection you receive depends entirely on the specific details of your policy, the limits you selected, and how well your coverage matches your actual situation.

Home insurance mistakes rarely happen because people are careless. They happen because insurance policies use specialized language, because life changes gradually, and because the fine print matters more than most people realize. Understanding where others have stumbled gives you a roadmap to avoid the same pitfalls.

Mistake 1: Insuring Your Home for the Wrong Value

One of the most fundamental errors homeowners make is selecting a coverage limit based on their home’s market value or purchase price rather than its rebuild cost. These two numbers can be very different.

Market Value vs. Rebuild Cost Explained

| Factor | Market Value | Rebuild Cost |

|---|---|---|

| Includes land value? | Yes | No |

| Affected by local real estate trends? | Yes | No |

| Includes demolition and debris removal? | No | Yes |

| Reflects current construction material prices? | Sometimes | Yes |

| What insurance actually uses | ❌ No | ✅ Yes |

Market value includes the land your home sits on, which never needs rebuilding after a disaster. It also fluctuates with local real estate conditions that have nothing to do with construction costs. Rebuild cost focuses purely on what a contractor would charge to reconstruct your home exactly as it stands today, including labor, materials, permits, and professional fees.

How Underinsuring Happens

A homeowner buys a house for $250,000. Five years later, construction costs in their area have risen 30 percent due to material shortages and labor demand. Their home would now cost $325,000 to rebuild, but their policy still shows $250,000 in dwelling coverage. A total loss would leave them $75,000 short.

This scenario plays out constantly because insurance companies don’t automatically adjust coverage without permission, and many homeowners never request a coverage review.

The Solution: Professional Rebuild Estimates

Ask your insurance agent for a replacement cost estimate rather than guessing. Some insurers offer online calculators, but a professional evaluation that considers your home’s square footage, construction type, and local building costs provides the most accurate number. Update this estimate every few years or after major renovations.

Mistake 2: Overlooking Endorsement Opportunities

A standard home insurance policy provides solid baseline protection, but it deliberately excludes certain risks and limits coverage on specific item categories. Many homeowners discover these gaps only after suffering a loss.

Common Coverage Gaps That Require Endorsements

Water Backup Protection

Standard policies exclude damage from sewer backups, sump pump failures, and drain overflows. A basement finished with $20,000 in materials and furnishings has no protection against this common scenario unless you add a water backup endorsement. The cost is modest, typically $50 to $100 per year for $10,000 to $20,000 in coverage.

Scheduled Personal Property

Jewelry, watches, furs, cameras, musical instruments, fine art, and collectibles face low sub-limits in standard policies. A typical limit might be $1,500 for all jewelry combined. An engagement ring worth $8,000 needs a scheduled personal property endorsement that lists it individually with its appraised value. This also broadens coverage to include accidental loss, which standard policies exclude.

Ordinance or Law Coverage

Building codes change constantly. A home built in 1990 may not meet today’s electrical, plumbing, or structural requirements. If a covered disaster triggers repairs, local laws may require bringing the entire home up to current code. Ordinance or law coverage pays the additional cost of complying with these updated regulations, preventing a financial shortfall that can reach tens of thousands of dollars.

Mistake 3: Misunderstanding Natural Disaster Exclusions

Home insurance policies clearly list what they exclude, but few homeowners read those lists until after a disaster strikes. The result is shock and financial strain when a flood or earthquake destroys their home and they learn they have no coverage.

Events Typically Excluded From Standard Policies

- Flooding from rising water, storm surge, or heavy rain

- Earthquakes and earth movement

- Mudslides and landslides

- Sinkholes (in most regions)

- Neglect or wear and tear

- Government action or war

The Importance of Risk Assessment

Every homeowner should honestly assess their natural disaster risk based on location. Federal emergency maps show flood zones. Geological surveys identify earthquake and landslide risks. Wildfire maps highlight areas with elevated danger.

If you live in a high-risk area for any excluded peril, purchasing separate coverage or a specialized endorsement protects against the one disaster most likely to affect your home. Waiting until after the event is too late.

Mistake 4: Forgetting About Home-Based Business Exposures

The rise of remote work and home-based businesses has created a widespread coverage gap. Standard home insurance policies provide very limited protection for business activities.

Business Equipment Limits

Most standard policies cap coverage for business property at $2,500, and that applies to equipment lost in your home. Equipment stolen from your car or a job site likely has no coverage at all. A laptop, printer, and specialized tools can easily exceed this limit.

Business Liability Gaps

If a client visits your home office and trips on a loose rug, your standard liability coverage might respond. But if your business activity causes injury elsewhere—like a catering business causing food poisoning—your home policy almost certainly excludes that claim.

The Right Solution

A home-based business endorsement adds coverage for equipment and liability. For larger businesses with inventory, employees, or significant client traffic, a separate business owners policy provides more comprehensive protection. Discuss your specific business activities with an agent to determine the right approach.

Mistake 5: Choosing Deductibles Without a Plan

The relationship between deductibles and premiums seems simple: higher deductible means lower premium. But choosing a deductible without considering your actual financial situation creates real risk.

The Deductible Trade-Off

| Deductible Amount | Approximate Annual Savings vs. $500 | Out-of-Pocket Risk |

|---|---|---|

| $500 | Baseline | Lowest |

| $1,000 | 15-25% lower | Moderate |

| $2,500 | 25-35% lower | Higher |

| $5,000 | 35-45% lower | Highest |

The Emergency Fund Test

Before selecting a deductible, ask yourself a simple question: Could I pay this amount from my emergency savings without borrowing money or causing financial strain? If the answer is no, the deductible is too high for your situation.

The premium savings from a higher deductible disappear if you cannot afford to pay it when disaster strikes. A $5,000 deductible saves money every year, but a single claim requiring that payment could force you into debt. Balance premium savings against realistic out-of-pocket ability.

Mistake 6: Filing Small Claims Without Thinking Long-Term

Every insurance claim goes into a database that insurers share. Too many claims, even small ones, can mark you as a higher risk and lead to premium increases or non-renewal.

The Claims Threshold Question

Ask yourself before filing: Can I afford to pay for this myself without significant hardship? If the answer is yes, consider handling it out of pocket.

A $2,000 claim with a $1,000 deductible nets you $1,000 from insurance. But that claim stays on your record for three to five years and could increase your premium by more than $1,000 over that period. The math sometimes favors self-payment.

Which Claims to Always File

Major losses like house fires, significant storm damage, or liability claims where someone is injured require filing a claim. These situations exceed what most homeowners can afford and justify the long-term consequences. The key is distinguishing between major disasters and minor incidents.

Mistake 7: Letting Your Policy Become Outdated

Life changes, but policies often stay the same. This mismatch creates coverage gaps that only appear when you need protection most.

Events That Should Trigger a Policy Review

- Major renovations or additions

- Purchase of expensive jewelry, art, or equipment

- Marriage or divorce

- Starting a home business

- Retirement (which may qualify for discounts)

- Installation of security systems or safety features

Annual Review Habit

Set a calendar reminder to review your policy every year, ideally around renewal time. Walk through your home, note any changes, and discuss them with your agent. This simple habit prevents the slow drift toward being underinsured that catches so many homeowners by surprise.

Do you know how much dose home insurence cost per month ?

Comparison Table: Common Home Insurance Mistakes and How to Avoid Them

| Mistake | Typical Consequence | Prevention Strategy |

|---|---|---|

| Insuring for market value | Out-of-pocket rebuild costs | Request professional rebuild estimate |

| Skipping endorsements | No coverage for valuable items or specific risks | Review policy limits and add endorsements for high-value items |

| Ignoring natural disaster exclusions | No coverage after flood or earthquake | Assess location risks and buy separate policies if needed |

| Overlooking home business exposure | Uncovered equipment and liability | Add business endorsement or separate policy |

| Choosing unaffordable deductible | Cannot pay out-of-pocket when claim occurs | Match deductible to emergency fund capacity |

| Filing small claims | Premium increases, possible non-renewal | Pay small losses out of pocket |

| Never updating policy | Coverage gaps as home and life change | Annual policy review with agent |

The Financial Impact of Home Insurance Mistakes

Understanding the dollar value of these mistakes puts them in perspective. A homeowner who underinsures by $50,000 faces that entire gap out of pocket after a total loss. Someone who skips flood coverage in a moderate-risk area might pay $30,000 for basement cleanup and repairs after a heavy rain event. A home business owner without proper liability coverage could face a lawsuit that exceeds their policy limits.

These numbers represent real financial setbacks that affect savings, retirement plans, and financial stability. Avoiding the mistakes costs nothing more than time and attention.

Building Better Insurance Habits

Protecting your home and finances through insurance doesn’t require becoming an expert. It requires developing a few simple habits that keep your coverage aligned with your actual needs.

Questions to Ask Your Agent Annually

- Is my dwelling coverage still enough to rebuild my home at today’s costs?

- Have any new exclusions or limitations been added to my policy?

- Do I qualify for any new discounts?

- Should I consider any endorsements based on changes in my life?

- How does my deductible compare to my emergency savings?

Documentation Practices That Help

Keep digital records of your home inventory, including photos and videos of each room. Store receipts for major purchases. Save copies of your policy declarations page where you can access them easily. These practices make claims smoother and reviews more productive.

Do you know what are the top rated home insurece provider?

Final Thoughts on Avoiding Home Insurance Mistakes

Home insurance exists to provide peace of mind and financial protection, but it only works when the policy matches your actual situation. The common mistakes outlined here happen to thoughtful people who simply didn’t know what they didn’t know.

Taking time now to review your coverage, understand your policy’s limits and exclusions, and build relationships with your agent transforms insurance from a mysterious expense into a reliable safety net. The small effort required pays dividends exactly when you need them most—

Frequently asked questions (FAQs)

Do home insurance mistakes affect my claim?

Yes, mistakes like low coverage limits or missed endorsements can reduce how much you receive.

How often should I review my home insurance policy?

It’s a good idea to review it at least once a year and after major home changes.

Can I fix coverage mistakes later?

Yes, you can update your policy, but changes usually apply only to future claims.

Is the cheapest policy the best choice?

Not always. Lower prices can mean less coverage or higher deductibles.

Conclusion

Common home insurance mistakes can be costly, but they are also avoidable. By understanding your policy, choosing the right coverage limits, and reviewing your insurance regularly, you can reduce the risk of unpleasant surprises.

Take time to ask questions, compare options, and update your policy when your home or lifestyle changes. A little attention now can make a big difference when you need your insurance the most.