Introduction

Health insurance is one of the most important financial decisions you will make as a US resident. But life changes. You might get a new job, move to a different state, qualify for a government program, or simply find a plan that works better for your situation. When that happens, one of the first questions people ask is — can you cancel health insurance at any time?

The honest answer is: it depends on the type of insurance you have.

Some plans allow you to cancel whenever you want. Others have strict rules about when cancellation is allowed and what happens if you drop coverage outside of specific windows. Getting this wrong can leave you without coverage exactly when you need it most, or create tax and financial complications you were not expecting.

This guide covers everything you need to know about canceling health insurance in the United States — from marketplace plans and employer coverage to Medicaid, Medicare, and COBRA. By the end, you will know exactly what your options are, when you can cancel, and how to do it correctly.

Table of Contents

Table of Contents

What Does It Mean to Cancel Health Insurance?

Canceling health insurance means formally ending your coverage under a health plan. Once coverage ends, you are responsible for the full cost of any medical care you receive — doctor visits, prescriptions, lab work, emergency room visits, and hospital stays.

Cancellation is different from simply not paying your premium. If you stop paying without formally canceling, your insurer will typically give you a grace period — usually 30 days for marketplace plans — before terminating your coverage. However, any claims filed during that grace period may be denied if you do not pay the overdue premium by the end of it.

Properly canceling your plan, on the other hand, means your coverage ends on a specific date that you control, and your insurer records that termination officially.

The Short Answer: Can You Cancel Health Insurance at Any Time?

Here is the straightforward breakdown:

- Marketplace (ACA) plans: You can cancel at any time, but re-enrolling later is only allowed during Open Enrollment or a Special Enrollment Period.

- Employer-sponsored plans: You can typically only cancel during your employer’s open enrollment period or after a qualifying life event.

- Medicaid: You can disenroll at any time with no waiting period.

- Medicare: Cancellation rules depend on the specific part of Medicare you want to drop.

- Short-term health plans: Most allow cancellation at any time, usually with a written notice.

- COBRA coverage: You can cancel COBRA at any time.

The key thing to understand is that canceling is often easy — but getting new coverage after you cancel is where restrictions apply.

Types of Health Insurance and Their Cancellation Rules

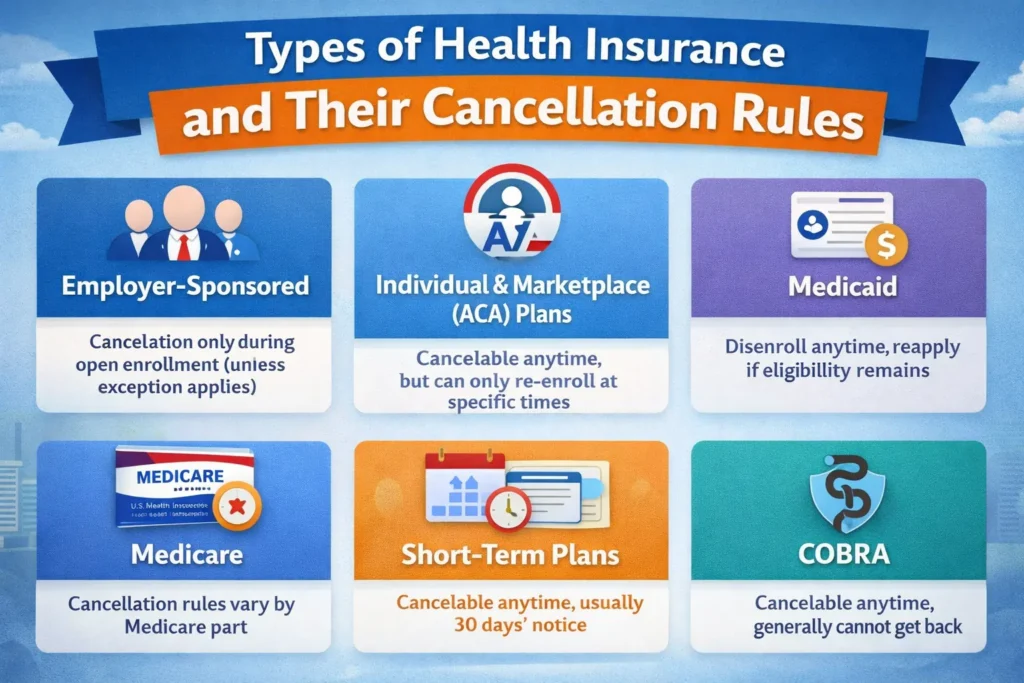

1. Employer-Sponsored Health Insurance

Employer-sponsored health insurance is the most common type of coverage in the US. According to the Kaiser Family Foundation, more than 160 million Americans get their health insurance through an employer.

With employer plans, you generally cannot cancel your coverage whenever you feel like it. Most employers allow you to make changes — including dropping coverage — only during the annual open enrollment period, which typically happens once a year, often in the fall.

Exceptions that allow you to cancel outside of open enrollment include:

- Losing eligibility for the plan (for example, dropping below the minimum hours required for coverage)

- Getting coverage through a spouse or domestic partner’s employer plan

- Becoming eligible for Medicaid or Medicare

- Leaving the job — either by quitting, being laid off, or retiring

If none of these apply and you cancel outside of your employer’s open enrollment window, your employer may not be able to add you back until the next enrollment period. That is a serious risk.

How to cancel: Contact your HR department or benefits administrator. They will walk you through the official process and the date your coverage will end.

2. Individual and Marketplace (ACA) Plans

Plans purchased through HealthCare.gov or a state-based marketplace are governed by the Affordable Care Act. These plans offer strong consumer protections, including coverage for pre-existing conditions and essential health benefits.

You can cancel an ACA marketplace plan at any time. There is no rule preventing you from calling your insurer or logging into your marketplace account and requesting cancellation. Your coverage will typically end at the end of the month in which you cancel, or on a future date you choose.

However — and this is the critical part — once you cancel, you can only re-enroll during the Open Enrollment Period or if you qualify for a Special Enrollment Period (SEP).

The ACA Open Enrollment Period for 2026 marketplace plans runs from November 1 to January 15. Outside of that window, you need a qualifying life event to enroll.

If you cancel your marketplace plan without having replacement coverage lined up, you could be uninsured for months.

3. Medicaid

Medicaid is a government-funded health insurance program for low-income individuals and families. Eligibility is based on income and household size.

You can disenroll from Medicaid at any time. There are no penalties for leaving, and there are no restricted enrollment windows for getting back in — as long as you still meet the income eligibility requirements.

If your income goes up and you no longer qualify for Medicaid, you will be transitioned off the program through a process called “redetermination.” In that case, losing Medicaid qualifies you for a Special Enrollment Period to sign up for a marketplace plan.

4. Medicare

Medicare is federal health insurance primarily for Americans aged 65 and older, and for certain younger people with disabilities.

Medicare has several parts — Part A (hospital insurance), Part B (medical insurance), Part C (Medicare Advantage), and Part D (prescription drug coverage). Each part has its own enrollment and disenrollment rules.

- Part A: Most people do not pay a premium for Part A and rarely need to cancel it.

- Part B: You can drop Part B, but you must do so carefully. Dropping it without creditable coverage from an employer can result in a permanent late enrollment penalty when you want to rejoin.

- Medicare Advantage (Part C): You can switch or drop a Medicare Advantage plan during the Annual Enrollment Period (October 15 – December 7) or the Medicare Advantage Open Enrollment Period (January 1 – March 31).

- Part D: Prescription drug plans can be dropped during the Annual Enrollment Period.

Medicare rules are more complex than other types of insurance. Before making any changes, it is strongly recommended that you contact Medicare directly at 1-800-MEDICARE or speak with a licensed Medicare counselor.

5. Short-Term Health Insurance Plans

Short-term health insurance plans are designed to provide temporary coverage. They are not required to cover the same essential benefits as ACA marketplace plans and generally do not cover pre-existing conditions.

Most short-term plans allow you to cancel at any time, often with just 30 days’ written notice. Some plans even issue a prorated refund if you cancel before the plan period ends.

These plans are regulated at the state level, so the specific cancellation rules can vary depending on where you live. Always check your plan documents or contact your insurer directly for the exact terms.

6. COBRA Coverage

When you lose employer-sponsored health insurance — due to job loss, reduced work hours, or other qualifying events — you may be eligible for COBRA continuation coverage. COBRA allows you to keep your previous employer’s group health plan for a limited time, but you pay the full premium yourself, which can be quite expensive.

You can cancel COBRA coverage at any time. There is no penalty for dropping it. However, once you voluntarily cancel COBRA, you generally cannot get it back unless you are still within your election period.

If you cancel COBRA before the continuation period ends, losing COBRA counts as losing minimum essential coverage, which qualifies you for a Special Enrollment Period on the marketplace.

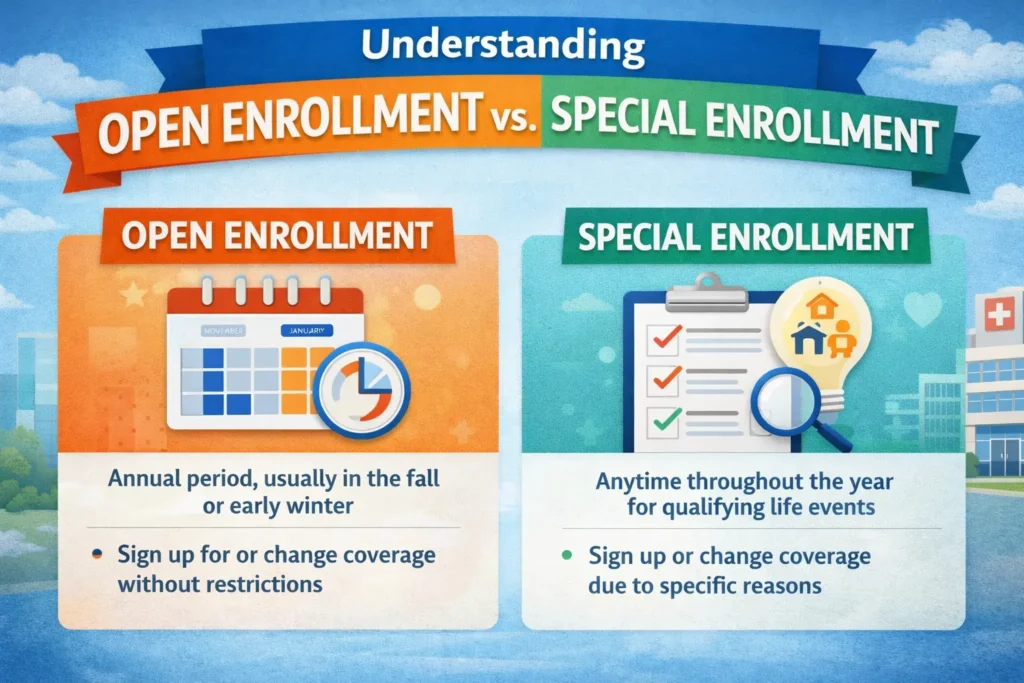

Understanding Open Enrollment vs. Special Enrollment

Open Enrollment Period (OEP)

The Open Enrollment Period is the annual window during which you can enroll in, switch, or cancel a marketplace health plan. For most states using HealthCare.gov, OEP runs from November 1 through January 15 each year.

During OEP, you do not need a reason to make a change. You can freely enroll, upgrade, downgrade, or cancel your plan. This is the safest time to make any coverage changes.

Special Enrollment Period (SEP)

Outside of Open Enrollment, you can only enroll in or switch a marketplace plan if you experience a qualifying life event that triggers a Special Enrollment Period. You typically have 60 days from the qualifying event to enroll.

Common qualifying life events include:

- Losing health coverage (job loss, aging off a parent’s plan, losing Medicaid eligibility)

- Getting married or divorced

- Having a baby or adopting a child

- Moving to a new ZIP code or county

- A significant income change that affects your eligibility for subsidies

- Gaining citizenship or lawful presence in the US

- Leaving incarceration

If you cancel your health insurance outside of OEP without having a qualifying SEP event, you may not be able to get new marketplace coverage until the next Open Enrollment Period.

What Happens When You Cancel Health Insurance?

You Lose All Coverage Immediately (or at Month’s End)

Once your cancellation takes effect, you are uninsured. Any medical bills you incur after that date are entirely your responsibility. Even a single emergency room visit without insurance can cost thousands of dollars.

Your Prescriptions Are No Longer Covered

If you take regular medications, losing insurance means paying full retail price unless you use discount programs like GoodRx. For people who take expensive medications, this can be a serious financial strain.

Pre-Existing Conditions Are No Longer Protected

Under the ACA, marketplace plans are required to cover pre-existing conditions without charging you more. However, that protection only applies while you are enrolled. Short-term plans and certain other non-ACA-compliant plans can deny coverage based on health history if you try to enroll in them after canceling your ACA plan.

Possible Tax Implications

The federal individual mandate penalty was reduced to $0 in 2019, meaning there is currently no federal tax penalty for being uninsured. However, several states have their own individual mandates with real financial penalties:

- Massachusetts

- New Jersey

- California

- Rhode Island

- Vermont

- Washington, DC

If you live in one of these states and go without qualifying health coverage for part of the year, you may face a state tax penalty when you file your return.

Do you know what are the top rated home insurence in usa?

Step-by-Step Guide: How to Cancel Your Health Insurance

Step 1: Decide on Your End Date

Before canceling, decide when you want coverage to end. Ideally, your new coverage should begin the day after your old coverage ends, so there is no gap.

Step 2: Contact Your Insurance Provider or Marketplace

- For marketplace plans: Log in to HealthCare.gov (or your state marketplace) and select the option to cancel your plan. You can also call the marketplace directly.

- For employer plans: Contact your HR department or benefits administrator.

- For Medicaid: Contact your state Medicaid office.

- For COBRA: Contact the COBRA administrator listed on your coverage documents.

- For private/short-term plans: Contact your insurer directly by phone or in writing.

Step 3: Request Written Confirmation

Always ask for written confirmation that your plan has been canceled. This protects you in case of billing errors or disputes later.

Step 4: Return Any Insurance Cards

Some insurers ask you to return or destroy your insurance cards. Follow the instructions provided.

Step 5: Confirm No Further Premiums Are Charged

Check your bank account or credit card statements in the following month to confirm that premiums are no longer being deducted.

What to Do Before You Cancel

Before you pull the trigger on canceling your health insurance, go through this checklist:

- Do you have new coverage lined up? Make sure the start date of your new plan overlaps with or immediately follows the end of your current plan.

- Are you in the middle of treatment? If you are receiving ongoing treatment — chemotherapy, physical therapy, mental health care — canceling coverage mid-treatment could interrupt care or leave you with large bills.

- Have you used up your deductible? If you are close to meeting your deductible for the year, it may make financial sense to wait until January 1 to switch plans.

- Are you taking ongoing prescriptions? Fill any prescriptions before your coverage ends to give yourself a buffer.

- Do you live in a state with an individual mandate? Make sure you understand the tax consequences of a coverage gap in your state.

Alternatives to Canceling Health Insurance

If cost is the main reason you are considering cancellation, it is worth exploring these alternatives before making a final decision.

Downgrade to a Lower-Cost Plan

During Open Enrollment or after a qualifying event, you can switch to a lower-tier plan with a higher deductible and lower monthly premium. A Bronze or Catastrophic plan might provide significant savings while keeping you protected from major medical expenses.

Check If You Qualify for Medicaid

If your income has dropped, you may now qualify for Medicaid, which provides free or very low-cost coverage. You can check your eligibility at HealthCare.gov at any time of year.

Apply for ACA Subsidies (Premium Tax Credits)

Many Americans do not realize they qualify for subsidies that significantly reduce their marketplace plan premium. Under current rules, subsidy eligibility extends to people earning up to 400% of the federal poverty level, and in some cases beyond that. Check your eligibility before canceling.

Join a Spouse’s or Parent’s Plan

If your spouse or domestic partner has employer coverage, you may be able to join their plan. Losing your own coverage is typically a qualifying life event that allows your spouse’s employer to add you mid-year.

If you are under 26, you can remain on a parent’s health insurance plan regardless of whether you are a student, married, or living away from home.

Keep COBRA Temporarily

If you just left a job, COBRA can keep you covered while you shop for a better option. It is expensive, but it buys you time to find a marketplace plan or enroll through a new employer without a coverage gap.

Common Reasons People Cancel Health Insurance

Understanding why people cancel — and whether those reasons hold up under scrutiny — can help you make a clearer-headed decision.

“It’s too expensive.” This is the most common reason. But before canceling, check whether you qualify for subsidies or Medicaid. Many people are surprised to find they qualify for significant financial help.

“I never use it.” Health insurance is not just for people who get sick regularly. It protects you from the financial devastation of an unexpected accident, surgery, or serious illness. A single hospitalization without insurance can result in tens of thousands of dollars in medical bills.

“I have a new job that provides coverage.” This is a completely valid reason to cancel your marketplace or individual plan. Just make sure your new employer coverage starts before or immediately after your old coverage ends.

“I’m moving to another country.” If you are leaving the US permanently, canceling your US health insurance makes sense. However, make sure you have international health coverage in place before you go.

“I’m switching to my spouse’s plan.” Another perfectly valid reason. Just confirm the enrollment dates so you do not end up with a gap.

Do you know what is loss of coverage in home insurence?

Mistakes to Avoid When Canceling Health Insurance

Canceling before your new coverage starts. Even a single day without coverage can expose you to enormous financial risk. Always confirm the start date of your new plan before canceling your old one.

Forgetting to cancel after switching. If you enroll in a new plan but forget to cancel the old one, you could be paying two premiums simultaneously. Check your bank statements carefully after any coverage change.

Assuming cancellation stops automatic payments. In some cases, automatic premium payments may continue for a billing cycle after you request cancellation. Follow up with your insurer and monitor your accounts.

Not getting written confirmation. Without written proof of cancellation, you could face billing disputes or gaps in your coverage records. Always request a cancellation confirmation in writing.

Missing the SEP window after a qualifying event. If you lose coverage and do not enroll in new insurance within 60 days, you may have to wait until the next Open Enrollment Period. Act quickly after any qualifying life event.

Frequently Asked Questions

Can I cancel my health insurance and get a refund? It depends on your plan. If you cancel before the end of the month and your premium was paid in advance, some insurers will issue a prorated refund. Short-term plans are more likely to offer refunds than ACA marketplace plans.

Will canceling health insurance affect my credit score? Canceling health insurance itself does not affect your credit score. However, if you go uninsured and accumulate unpaid medical bills that go to collections, that can negatively impact your credit.

Can I cancel health insurance on behalf of a family member? If you are the primary policyholder, you can typically add or remove covered family members. However, some plans have restrictions on removing dependents outside of open enrollment. Check with your insurer or HR department.

What is the earliest I can cancel an ACA plan? You can request cancellation at any time for a future date. The coverage typically ends at the end of the month in which you cancel, though some marketplace plans may allow a specific future end date.

Does canceling health insurance impact future enrollment? At the federal level, canceling a marketplace plan does not disqualify you from re-enrolling during the next Open Enrollment Period. However, if you live in a state with an individual mandate, having a gap in coverage may result in a state tax penalty.

Final Thoughts

So — can you cancel health insurance at any time? Technically, yes. Most health insurance plans allow you to request cancellation whenever you choose. But the real question is not whether you can cancel. It is whether you should, and what happens next.

Losing health coverage without a replacement plan in place is a serious financial risk. Medical costs in the United States are among the highest in the world. Without insurance, a broken arm, an unexpected illness, or a routine surgery can cost you thousands — sometimes tens of thousands — of dollars.

Before you cancel, take the time to understand your options. Check whether you qualify for Medicaid or ACA subsidies. Look into your spouse’s plan or your employer’s coverage. If switching plans makes sense, line up your new coverage before dropping the old one.

Health insurance is not just a monthly bill — it is a financial safety net. Make sure you have a plan before you let it go.

This article is for informational purposes only and does not constitute legal or financial advice. Health insurance rules and programs can change. Always verify current information directly with your insurer, your state marketplace, or the official HealthCare.gov website.