Introduction:

A burst pipe can flood your home in minutes, causing serious water damage to floors, walls, furniture, and electrical systems. The good news? Most homeowners insurance policies in the US cover sudden and accidental water damage. Knowing how to handle a burst pipe insurance claim the right way can help you get paid faster and avoid claim denial.

Step 1: Stop the Water Immediately

Your first priority is safety and damage control.

Turn off the main water supply to prevent further flooding. If water is near electrical outlets, switch off power to the affected area if it’s safe to do so. Insurance companies expect homeowners to take reasonable steps to reduce additional damage.

Table of Contents

Table of Contents

Step 2: Document All Damage

Before cleaning up too much, take clear photos and videos of:

- The burst pipe

- Standing water

- Damaged walls, floors, and ceilings

- Ruined furniture or belongings

This evidence is critical for your homeowners insurance claim. The more proof you have, the smoother the process.

do you know How to Write an Appeal Letter to an Insurance Company

Step 3: Contact Your Insurance Company Fast

Report the issue as soon as possible. Many insurers have 24/7 claim hotlines. When filing your burst pipe insurance claim, provide:

- Date and time of the incident

- Cause of the pipe burst (freezing, corrosion, etc.)

- List of damaged items

Delays in reporting can sometimes lead to reduced payouts.

Step 4: Understand What Insurance Covers

Most standard US homeowners policies cover sudden pipe bursts and resulting water damage. This usually includes:

✔ Water damage to walls and floors

✔ Mold prevention if addressed quickly

✔ Personal property damage

✔ Temporary living expenses if your home is unlivable

However, damage from long-term leaks or poor maintenance is often not covered. Insurance is for sudden accidents, not neglect.

Do you know How Long Does a Homeowners Insurance Claim Take?

Step 5: Keep All Receipts

Save receipts for:

- Emergency plumbing repairs

- Water removal services

- Hotel stays or meals if you must leave home

These costs may be reimbursed under your policy’s loss of use coverage.

Step 6: Work With the Adjuster

An insurance adjuster will inspect the damage. Be present if possible and show all affected areas. Share your photos and repair estimates. Clear communication helps avoid disputes and speeds up your payout.

Do you know What Does AOB Stand for in Insurance?

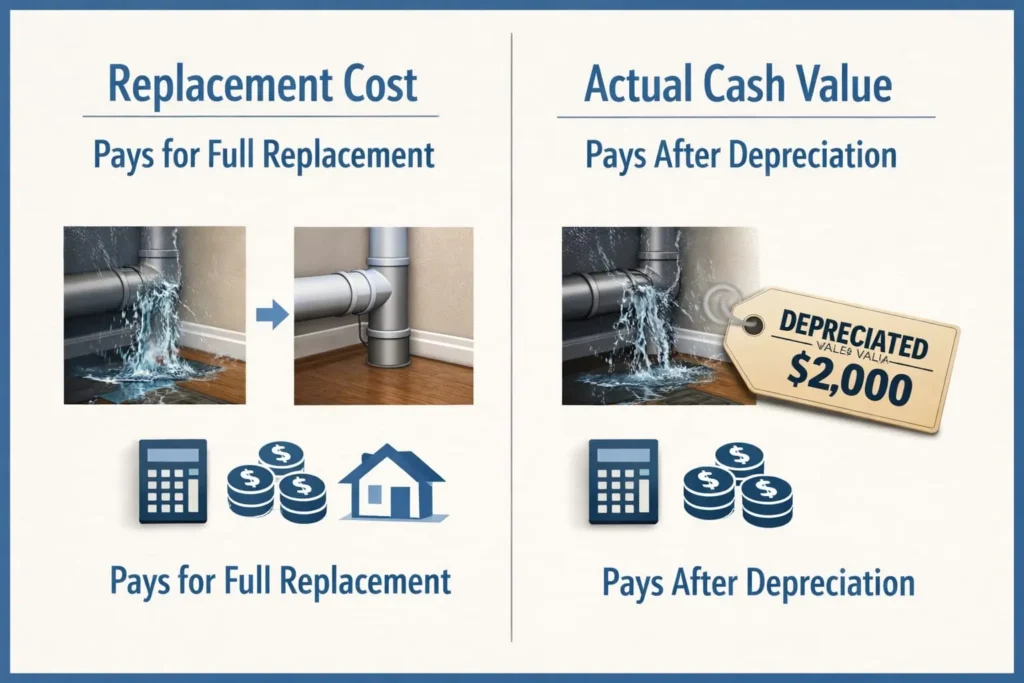

Replacement Cost vs. Actual Cash Value: Why It Matters

Your payout depends heavily on the type of coverage you have.

Replacement Cost Coverage

This pays to replace damaged items with new ones of similar quality, without subtracting depreciation (after repairs are completed).

Actual Cash Value (ACV)

This subtracts depreciation based on age and condition.

For example:

If your 10-year-old hardwood floor is damaged:

- Replacement cost might be $8,000

- ACV payout could be $4,500

Knowing your policy type determines how much you truly recover.

Hidden Damage: What Adjusters Look For

Insurance companies often inspect for:

- Moisture behind drywall

- Damage under baseboards

- Water trapped in subflooring

- Compromised structural beams

- Electrical corrosion

If these are not documented early, you may need to file a supplemental claim later.

To protect yourself:

- Request a moisture meter reading

- Ask for thermal imaging inspection

- Get a licensed water remediation contractor assessment

This ensures nothing is overlooked.

How Insurance Companies Investigate Burst Pipe Claims

In 2026, insurers use a more data-driven approach.

They evaluate:

- Weather reports (Was there freezing?)

- Utility usage history

- Maintenance records

- Prior claims

- Home inspection history

If your claim involves frozen pipes, insurers may verify whether you:

- Maintained adequate heat

- Shut off water when away

- Properly insulated pipes

Understanding this helps you prepare documentation in advance.

Supplemental Claims: Increasing Your Payout After Initial Estimate

Many homeowners do not realize they can request additional payment if new damage is discovered.

You can file a supplemental claim if:

- Mold appears later

- Flooring damage spreads

- Drywall removal reveals more moisture

- Repair costs exceed initial estimate

Contractors often discover hidden damage during demolition. If so:

- Document new findings

- Request written contractor explanation

- Submit updated estimate

- Notify insurer immediately

This process can add thousands to your settlement.

Water Mitigation and Why It Impacts Your Claim

Insurance companies expect you to hire professional water mitigation quickly.

Professional drying services typically include:

- Industrial dehumidifiers

- Air movers

- Moisture monitoring

- Antimicrobial treatment

- Daily drying logs

Failure to dry properly can:

- Increase damage

- Trigger mold exclusions

- Lead to claim denial

Quick action strengthens your case.

Temporary Housing and Loss of Use Strategy

If your home becomes unlivable due to burst pipe damage, your policy may include Additional Living Expenses (ALE).

Covered expenses may include:

- Hotel stays

- Short-term rentals

- Increased food costs

- Laundry services

- Pet boarding

However, insurers reimburse only the “extra” amount above your normal living expenses.

Keep detailed records of:

- Rental agreements

- Meal receipts

- Utility comparisons

- Travel mileage

Proper tracking ensures full reimbursement.

Do you know what are the common people mistakes While Choosing Home Insurence?

When Mold Becomes a Separate Claim Issue

Water damage often leads to mold growth within 24–48 hours.

Some policies limit mold coverage to:

- $5,000

- $10,000

- Or specific sublimits

If mold remediation exceeds limits, you may face out-of-pocket costs.

To reduce risk:

- Start drying immediately

- Document remediation steps

- Keep contractor certifications

- Follow all adjuster instructions

Early action protects both health and finances.

Burst Pipes in Rental Properties: Landlord vs Tenant Responsibility

If you are a landlord:

Your homeowners policy (or landlord policy) may cover structural damage.

If you are a tenant:

Your renters insurance covers personal property only — not the building.

Responsibility may depend on:

- Lease terms

- Negligence

- Maintenance records

Understanding your role avoids legal complications.

Seasonal Burst Pipe Risks in the U.S.

Certain regions face higher pipe burst risk:

- Midwest (extreme winter freezes)

- Northeast (aging infrastructure)

- Southern states during rare freezes

- Mountain states with elevation-related freezing

Insurance companies assess regional risks differently.

Some may require:

- Insulation proof

- Winterization documentation

- Smart leak detection systems

Installing preventative technology may even reduce premiums.

Smart Home Technology and Insurance Discounts

In 2026, many insurers offer discounts for:

- Automatic water shut-off systems

- Leak detection sensors

- Temperature monitoring systems

- Smart plumbing monitoring

These devices:

- Detect leaks early

- Shut off water automatically

- Send phone alerts

They not only prevent major damage but strengthen your credibility during claims.

What Happens If Your Claim Is Denied?

Common denial reasons include:

- Long-term leak evidence

- Poor maintenance

- Pipe corrosion due to neglect

- Failure to heat home

- Policy exclusions

If denied, you can:

- Request written explanation

- Review policy language

- Gather additional documentation

- Submit formal appeal

- Hire a public adjuster

- File complaint with state insurance department

Denial does not always mean the end of the process.

Negotiating a Higher Settlement

If your settlement offer seems low:

- Compare with contractor estimates

- Review depreciation calculations

- Check labor pricing accuracy

- Ask for line-item breakdown

Insurance estimates sometimes use outdated pricing databases.

Negotiation is common and acceptable when supported by evidence.

Understanding Deductibles and Out-of-Pocket Costs

Your deductible directly impacts payout.

Example:

If damage totals $15,000

Deductible = $2,500

Insurance pays $12,500

Higher deductibles mean lower premiums but more risk.

Before filing small claims, calculate whether it is worth it.

Do you know how dose deductibles work in home insurence?

Filing Multiple Claims: Will It Raise Premiums?

Yes, multiple water damage claims can:

- Increase premiums

- Trigger non-renewal

- Affect claim history reports

Insurance companies track claims through shared databases.

If damage is minor and below deductible, consider paying out-of-pocket.

Long-Term Financial Planning After a Burst Pipe

Even after payout, homeowners should:

- Upgrade plumbing

- Replace aging pipes

- Improve insulation

- Install smart detection systems

- Schedule annual plumbing inspections

Preventing future claims protects both your home and insurability.

Emotional and Financial Stress Management

Water damage can disrupt daily life significantly.

Common challenges include:

- Displacement stress

- Contractor coordination

- Financial anxiety

- Family inconvenience

Being organized reduces emotional strain.

Create a simple claim binder:

- Policy documents

- Communication log

- Receipts

- Estimates

- Inspection reports

Control reduces chaos.

Insurance Industry Trends in 2026

The insurance industry is changing due to:

- Climate volatility

- Increased water damage claims

- Rising construction costs

- Stricter underwriting

Some insurers now:

- Require plumbing inspections for older homes

- Limit water damage payouts

- Introduce water damage sublimits

Review your policy annually to stay protected.

How Long Does a Burst Pipe Claim Typically Take?

General timeline:

- Minor water damage: 2–4 weeks

- Moderate structural repairs: 1–3 months

- Major rebuild projects: 6+ months

Catastrophe events may extend timelines significantly.

Prompt communication shortens delays.

Tax Considerations After Insurance Payout

Insurance payouts for property damage are generally not taxable if they restore you to pre-loss condition.

However, if:

- You receive more than your adjusted basis

- You claim casualty loss deductions

Consult a tax professional for guidance.

Contractor Fraud Warning

After large freeze events, contractor scams increase.

Warning signs:

- Door-to-door pressure

- Large upfront cash requests

- No license or insurance

- Vague contracts

Always verify:

- State license

- Insurance certificates

- Written contract terms

Insurance fraud can void your claim.

Final Expert Advice for U.S. Homeowners

To truly maximize your burst pipe insurance payout in 2026:

- Act fast

- Document thoroughly

- Understand your coverage

- Monitor adjuster calculations

- Keep communication professional

- Protect against future incidents

Water damage is stressful — but informed homeowners consistently receive stronger settlements.

Insurance is designed to restore your financial position, but preparation determines how smooth the process becomes.

Common Mistakes to Avoid

❌ Throwing away damaged items before documentation

❌ Waiting too long to report the claim

❌ Starting major repairs before adjuster approval

❌ Ignoring small leaks that later become big problems

FAQs About Burst Pipe Insurance Claims

Q1: Does homeowners insurance cover burst pipes in winter?

Yes, if the pipe burst is sudden and you maintained reasonable heat in the home.

Q2: Will insurance pay to replace the pipe?

Usually, insurance covers the water damage but not always the pipe repair itself, unless specified.

Q3: How long do I have to file a claim?

Most insurers require prompt reporting, so file as soon as possible after the damage occurs.

Q4: Does insurance cover mold after a burst pipe?

It may be covered if you act quickly to dry the area and prevent mold growth.