Introduction

If you’ve ever reviewed an insurance claim or worked with a contractor after property damage, you may have come across the term AOB and wondered what it means. Many homeowners and policyholders ask the same question: what does AOB stand for in insurance, and is it something you should agree to?

AOB is a common but often misunderstood insurance term in the United States. While it can simplify the claims process, it can also create serious problems if you don’t understand how it works. This guide explains AOB in plain English, including its meaning, how it works, pros and cons, legal concerns, and what US homeowners should know before signing an AOB agreement.

Table of Contents

Table of Contents

What Does AOB Stand for in Insurance?

AOB stands for Assignment of Benefits.

In insurance, an Assignment of Benefits is a legal agreement that allows a policyholder to transfer certain insurance rights to a third party, usually a contractor, restoration company, or medical provider.

When you sign an AOB, you give that company permission to:

- File an insurance claim on your behalf

- Communicate directly with your insurance company

- Receive claim payments directly from the insurer

This means you may no longer control parts of the claims process

Do you know What Is Loss of Use Coverage in Homeowners ?

How Assignment of Benefits (AOB) Works

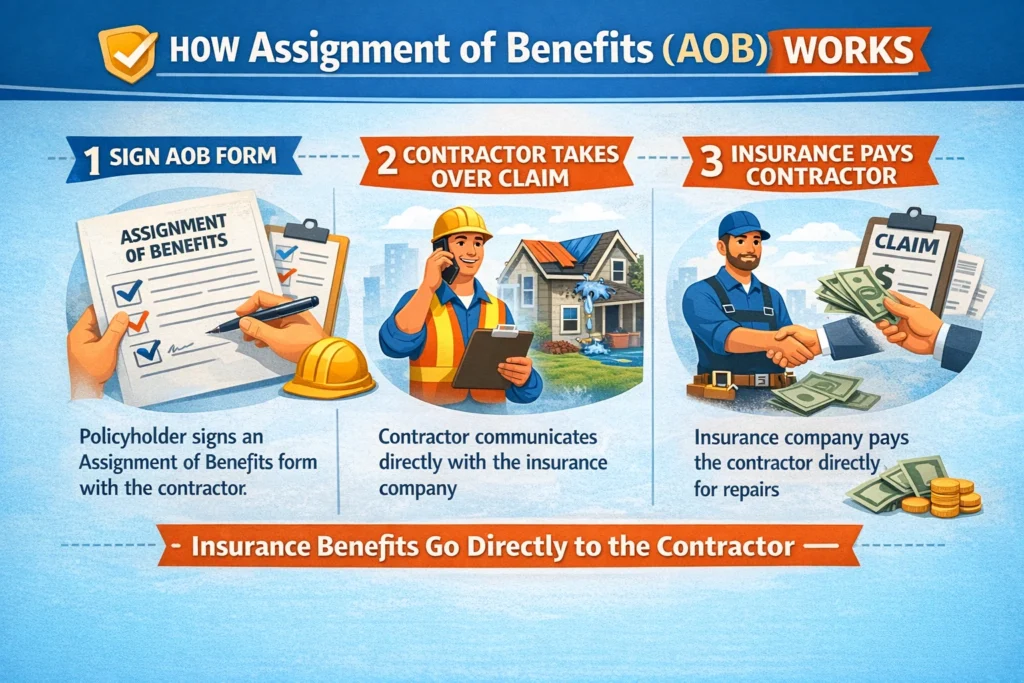

To better understand what AOB means in insurance, let’s look at a simple example.

Imagine your home suffers water damage from a burst pipe. A restoration company offers to start repairs immediately but asks you to sign an Assignment of Benefits form. Once signed:

- The contractor contacts your insurance company

- They submit invoices and documentation

- The insurer pays the contractor directly

This can seem convenient, but it also transfers important rights away from you as the policyholder.

Why AOB Is Common in the United States

Assignment of Benefits agreements are widely used in:

- Property damage claims

- Water and mold remediation

- Roofing repairs

- Auto and health insurance claims

They became popular because they allow faster repairs without the homeowner paying upfront costs. However, misuse of AOB agreements has caused significant issues in several US states.

Do you know home insurence cover mold ?

Pros of Assignment of Benefits

Understanding both sides helps answer the question: is AOB good or bad?

Advantages of AOB:

- Faster repairs without upfront payment

- Less paperwork for homeowners

- Contractors handle insurance communication

- Helpful during emergencies

For some policyholders, AOB can reduce stress during an already difficult situation.

Cons and Risks of AOB Agreements

Despite the benefits, AOB agreements come with serious risks.

Major disadvantages:

- Loss of control over the claim

- Contractors may inflate repair costs

- Insurance disputes without your involvement

- Potential lawsuits filed in your name

- Higher insurance premiums over time

Many homeowners don’t realize they’ve signed away rights until a problem occurs.

Is AOB Legal in the United States?

Yes, Assignment of Benefits is legal in many US states, but laws vary by state.

Some states, such as Florida, have implemented strict regulations due to widespread abuse. Other states allow AOB with fewer restrictions.

Always check your state insurance laws and read your policy carefully before signing any AOB document.

Why Insurance Companies Dislike AOB

Insurance companies often discourage AOB agreements because:

- They lose direct communication with policyholders

- Claims costs increase due to inflated invoices

- Fraud becomes harder to control

- Litigation risks rise

As a result, many insurers now include AOB restrictions or exclusions in homeowners insurance policies.

How AOB Affects Homeowners Insurance Policies

Some insurance policies now:

- Limit or prohibit Assignment of Benefits

- Require insurer approval before AOB is valid

- Reduce coverage if AOB is signed

- Offer discounts for policies without AOB rights

This is why it’s important to understand what AOB stands for in insurance before filing a claim.

When Should You Avoid Signing an AOB?

You should be cautious if:

- The contractor pressures you to sign quickly

- The document is unclear or incomplete

- You are not given a copy

- The contractor refuses to explain terms

- Your insurer advises against it

Never sign an AOB without reading it fully.

Safer Alternatives to Assignment of Benefits

Instead of signing a full AOB, consider:

- Limited authorization forms

- Direct payment authorization only

- Paying the contractor after insurance reimbursement

- Working with insurer-approved contractors

These options allow you to keep control while still completing repairs.

AOB vs Power of Attorney: Are They the Same?

No. While both involve granting authority, they are different.

- AOB transfers insurance payment rights

- Power of Attorney grants legal decision-making authority

An AOB is specific to insurance benefits, but it can still have serious consequences.

Common Misconceptions About AOB

Many people believe:

- AOB is required (❌ false)

- Insurance will deny claims without AOB (❌ false)

- AOB has no legal impact (❌ false)

Understanding the truth protects you from costly mistakes.

How to Protect Yourself as a Policyholder

To stay safe:

- Read your insurance policy carefully

- Ask your insurer before signing an AOB

- Get multiple repair estimates

- Avoid blank or rushed agreements

- Keep written records

Knowledge is your best protection.

Do you know what are Home Insurance Claim Adjuster Secret Tactics ?

FAQs About AOB in Insurance

What does AOB stand for in insurance?

AOB stands for Assignment of Benefits, a legal agreement that transfers insurance claim rights to a third party.

Is Assignment of Benefits bad?

Not always, but it carries risks and should only be signed after careful review.

Can I cancel an AOB agreement?

In some states, yes—but cancellation rules vary by state and contract.

Does AOB increase insurance premiums?

Widespread AOB abuse can contribute to higher premiums over time.