Introduction

When a hurricane approaches, most people focus on protecting their families and homes. However, another major concern for many Americans is their vehicle. For many households, a car is one of the most expensive assets they own. Seeing news reports of flooded streets, fallen trees, and damaged vehicles during a hurricane can make anyone wonder what would happen if their own car were caught in the storm.

This leads to an important question: Does car insurance cover hurricane damage? The answer depends on the type of insurance coverage you have. While some policies can protect your vehicle from storm-related damage, others may not offer any protection at all.

In this guide, you will learn how car insurance works during hurricanes, what coverage you need, how the claims process works, and how to avoid common mistakes. Understanding these details can help you protect your vehicle and avoid expensive repair costs after a storm.

What Is Car Insurance for Hurricane Damage?

Table of Contents

Table of Contents

Many people believe there is a special type of car insurance specifically designed for hurricanes. In reality, there is no separate hurricane insurance policy for vehicles.

Instead, protection from hurricanes falls under a type of auto insurance called comprehensive coverage.

Comprehensive coverage protects your vehicle from events that are not related to collisions with another car. This includes damage caused by natural disasters, severe weather, and other unexpected events.

Hurricanes are considered acts of nature, so any damage caused by them is usually handled through comprehensive coverage.

Events Covered by Comprehensive Insurance

If you have comprehensive coverage, your insurance policy may help pay for damage caused by:

- Hurricane winds

- Flooding from storm surge or heavy rain

- Falling trees or branches

- Flying debris

- Hail damage

- Lightning strikes

- Fire caused by storms

- Vandalism or theft after the storm

For example, if strong winds knock a tree onto your parked vehicle, comprehensive insurance may help cover the repair costs.

What If You Only Have Liability Insurance?

Many drivers carry only the minimum insurance required by law, which is liability coverage.

Liability insurance only pays for damage you cause to other people or their property. It does not cover damage to your own vehicle.

This means if your car is damaged by a hurricane and you only have liability coverage, you will likely have to pay the entire repair cost yourself.

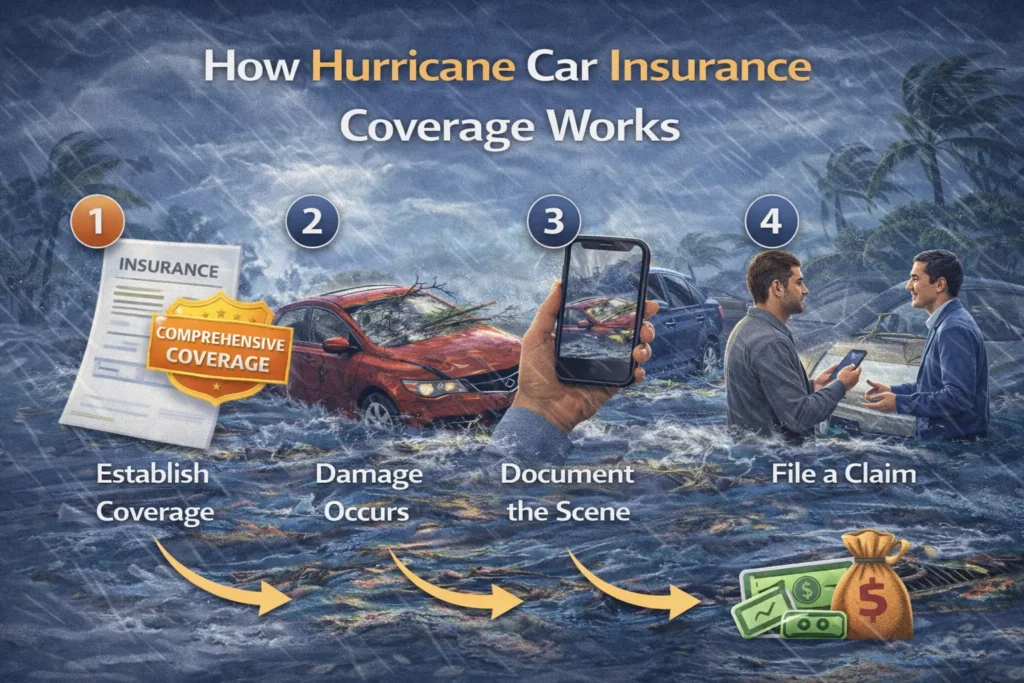

How Hurricane Car Insurance Coverage Works

Understanding how hurricane-related claims work can help drivers feel more prepared if a storm damages their vehicle.

While every insurance company has its own process, the basic steps are usually similar.

Step 1: Having Comprehensive Coverage Before the Storm

The most important requirement is having comprehensive coverage before the hurricane forms or becomes a threat.

Insurance companies often place binding restrictions when a hurricane is expected. This means they temporarily stop allowing customers to add new coverage or change their policies until the storm passes.

Because of this rule, you cannot wait until a hurricane is already approaching to add protection.

The best time to review your policy is before hurricane season begins, which typically runs from June through November in the United States.

Step 2: Hurricane Damage Occurs

During a hurricane, vehicles may be damaged in several ways.

Common hurricane-related car damage includes:

- Water entering the engine

- Interior damage from flooding

- Broken windows from debris

- Roof damage from fallen trees

- Body dents from strong winds

Many vehicles are damaged while parked outside, especially if they are located near trees or in low-lying areas that flood easily.

Step 3: Inspecting and Documenting the Damage

After the storm has passed and local authorities confirm it is safe to go outside, the next step is checking your vehicle.

At this point, it is important to document the damage carefully.

Helpful steps include:

- Taking clear photos from multiple angles

- Recording videos of the damage

- Writing down the time and location of the incident

- Saving any official storm warnings or reports

This documentation helps insurance companies verify that the damage was caused by the hurricane.

One important safety tip is never attempt to start a flooded vehicle. Water inside the engine can cause severe internal damage.

Step 4: Filing an Insurance Claim

Once you have documented the damage, you should contact your insurance company to begin the claims process.

Most insurers allow claims to be filed through:

- Mobile apps

- Online portals

- Phone calls

- Insurance agents

Because hurricanes affect large areas, insurance companies often activate special catastrophe response teams to help process claims quickly.

You may need to provide:

- Your policy number

- Photos of the damage

- A description of what happened

- The location of the vehicle during the storm

Step 5: Damage Assessment by an Adjuster

After the claim is submitted, an insurance adjuster reviews the situation.

The adjuster may:

- Inspect the vehicle in person

- Review photos and videos

- Estimate repair costs

- Determine whether the car can be repaired or must be replaced

If the repair cost is close to or higher than the vehicle’s market value, the car may be declared a total loss.

Step 6: Paying the Deductible

Most comprehensive policies include a deductible, which is the amount you must pay out of pocket before insurance covers the rest.

For example:

- Repair cost: $4,000

- Deductible: $500

- Insurance payment: $3,500

Choosing a higher deductible usually lowers monthly insurance premiums, but it increases the amount you must pay if you file a claim.

Step 7: Repairs or Vehicle Replacement

If the car can be repaired, the insurance company typically pays the repair shop directly or reimburses you.

If the vehicle is totaled, the insurer pays the current market value of the car, not the price you originally paid for it.

This payment is known as the actual cash value (ACV).

Real-Life Example

To better understand how hurricane coverage works, consider this example.

Marcus lives in Florida, a state that experiences hurricanes frequently. He owns a 2021 SUV worth about $27,000.

Marcus has an auto insurance policy that includes comprehensive coverage with a $500 deductible.

During a major hurricane, strong winds knock down a large tree in Marcus’s yard. The tree falls directly onto the roof of his SUV.

The vehicle suffers:

- A crushed roof

- A shattered windshield

- Broken side mirrors

Marcus contacts his insurance company and files a claim.

An adjuster inspects the damage and estimates the repair cost at $8,200.

Financial Breakdown

- Total repair cost: $8,200

- Marcus’s deductible: $500

- Insurance payment: $7,700

Because Marcus had comprehensive coverage, he only pays $500, and the insurance company covers the remaining repair cost.

Without this coverage, Marcus would have had to pay the entire $8,200 out of his own pocket.

Do You Know What Is Does Car Insurance Cover Drunk Driving Accidents?

Why Hurricane Coverage Is Important

Hurricanes can cause serious financial damage in addition to physical damage. Having the right insurance protection can make a big difference when recovering from a storm.

Protection Against Natural Disasters

Hurricanes bring powerful winds, heavy rain, and flooding.

These conditions can easily damage parked vehicles, especially in coastal areas or regions with poor drainage.

Insurance coverage helps protect drivers from sudden repair costs.

High Cost of Vehicle Repairs

Modern vehicles contain advanced technology and expensive parts.

Even moderate storm damage can cost thousands of dollars to repair.

Common hurricane-related repairs include:

- Electrical system replacement

- Engine repair after flooding

- Windshield replacement

- Bodywork and paint restoration

Without insurance, these costs can create a serious financial burden.

Faster Recovery After a Disaster

After a hurricane, many people need their vehicles to:

- Travel to work

- Buy groceries

- Visit doctors

- Help family members

Insurance coverage helps drivers repair or replace their vehicles faster so they can return to normal life.

Lender Requirements

If you finance or lease a vehicle, your lender usually requires comprehensive coverage.

This requirement protects the lender’s investment until the vehicle is fully paid off.

Pros and Cons of Hurricane Coverage

Like any insurance decision, comprehensive coverage has advantages and disadvantages.

Pros

- Covers damage from hurricanes and natural disasters

- Protects against falling trees and flying debris

- Helps pay for expensive repairs

- Often required for financed vehicles

- Provides peace of mind during hurricane season

Cons

- Increases monthly insurance premiums

- Requires paying a deductible when filing a claim

- Only pays the car’s current market value

- Does not usually cover personal belongings inside the car

For many drivers, the protection provided by comprehensive coverage outweighs the additional cost.

Common Mistakes People Make

Many drivers misunderstand how hurricane coverage works. Avoiding these mistakes can help prevent problems later.

Waiting Until a Storm Is Approaching

Insurance companies often stop allowing policy changes when a hurricane is expected.

If you wait too long, it may be impossible to add coverage before the storm arrives.

Assuming “Full Coverage” Is Automatic

Many drivers believe they have full coverage without checking their policy details.

In reality, you must specifically confirm that comprehensive coverage is included.

Attempting to Start a Flooded Vehicle

Starting a flooded car can damage the engine permanently.

If your vehicle has been underwater, it should be inspected by a professional mechanic.

Forgetting About Deductibles

Some drivers forget they must pay a deductible before insurance covers repairs.

Understanding your deductible helps you plan financially.

Leaving Valuable Items in the Car

Car insurance usually covers the vehicle itself but not personal items left inside.

Items like laptops, phones, or expensive bags may be covered under homeowners or renters insurance instead.

Frequently Asked Questions (FAQs)

Does car insurance cover flooding from a hurricane?

Yes, but only if you have comprehensive coverage. Flood damage caused by storms is typically included in this type of policy.

Will my insurance rates increase after a hurricane claim?

In many cases, rates do not increase for natural disaster claims because they are considered events outside the driver’s control. However, policies can vary by insurer and state.

Can insurance replace my car if it is destroyed by a hurricane?

Yes. If the repair cost exceeds the vehicle’s value, the insurer may declare it a total loss and pay the current market value of the car.

Does car insurance cover rental vehicles after hurricane damage?

Only if you have rental reimbursement coverage. This optional add-on helps pay for a rental car while your vehicle is being repaired.

Conclusion

Hurricanes can cause serious damage to vehicles through flooding, falling trees, and powerful winds. Because of this risk, understanding how your car insurance works is essential.

In most cases, comprehensive coverage is the only type of auto insurance that protects vehicles from hurricane damage. Without it, drivers may have to pay for costly repairs or vehicle replacement themselves.

Reviewing your insurance policy before hurricane season begins can help ensure your vehicle is properly protected. Taking this simple step can provide peace of mind and financial security if a storm strikes.