Introduction

Walking back to your car only to find a pile of shattered glass where your window used to be is a gut-wrenching experience. Beyond the mess and the initial shock, your mind immediately jumps to the cost of repairs. If someone broke into your vehicle to steal your bags, your GPS, or even just the loose change in your console, you are left with a bill that can easily reach hundreds of dollars.

The big question on every driver’s mind is: Will my insurance pay for this? The answer is usually yes, but it depends entirely on the specific type of policy you have. Not all car insurance is created equal when it comes to theft and vandalism. In this guide, we will break down exactly how glass coverage works, the steps you need to take to file a claim, and why your car insurance might not be the one to pay for your stolen laptop.

What is Theft-Related Glass Coverage?

Table of Contents

Table of Contents

In the world of insurance, a broken window from a break-in is classified as “vandalism” or “theft-related damage.” This is handled differently than a window that breaks during a car accident. Because the damage didn’t happen while you were driving, it falls under a specific part of your policy called Comprehensive Coverage.

Comprehensive insurance is an optional add-on in the United States. It is often nicknamed “Other Than Collision” coverage because it handles all the “acts of God” and random bad luck that can happen to a car while it’s parked.

Here is what this coverage typically handles:

- Smashed Windows: Side windows, windshields, and rear glass.

- Damaged Locks: If a thief tried to pry open your door handle or ruined the key cylinder.

- Internal Damage: If the thief scratched your leather seats with glass or broke the dashboard while ripping out a radio.

- Stolen Parts: If they took your catalytic converter or factory-installed speakers.

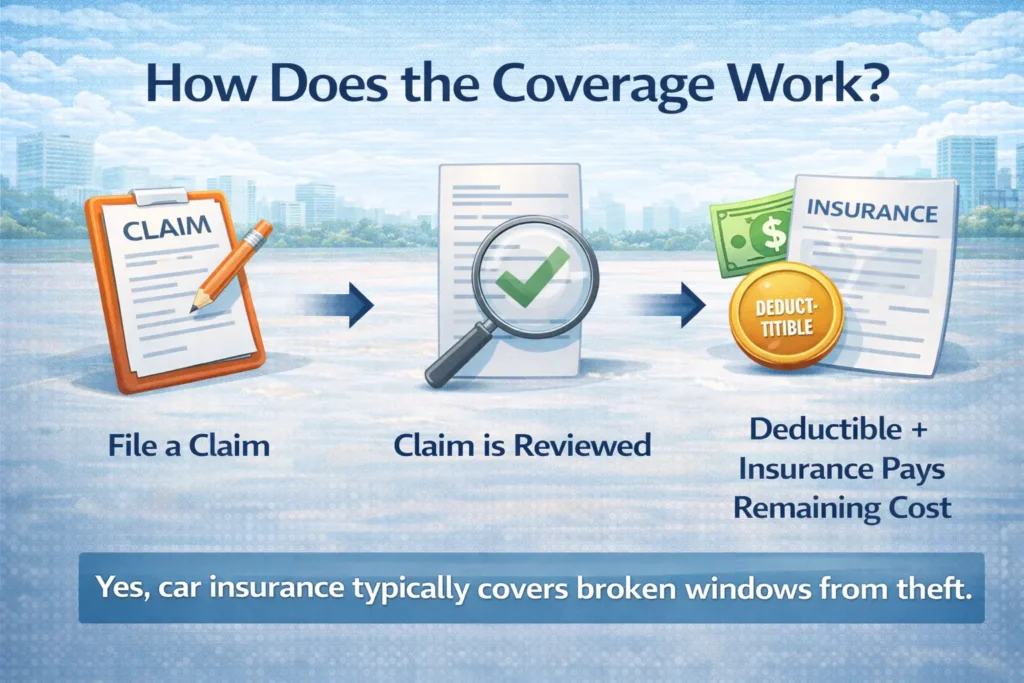

How Does the Coverage Work?

If you have comprehensive insurance, the process of getting your window fixed is fairly straightforward. However, you have to follow a specific “flow” to make sure your insurance company honors the claim.

- File a Police Report: Most insurance companies require an official police report for theft or vandalism. Even if the police don’t come to the scene, you can often file this report online or at the station.

- Document the Damage: Take clear photos of the broken glass and any other damage to the car before you clean it up.

- The Deductible Check: You will have to pay your “deductible” first. This is the amount of money you agreed to pay out of pocket (usually $250, $500, or $1,000) before the insurance kicks in.

- The Repair: Your insurer will usually send you to a preferred glass shop. If the window is totally smashed, it will be replaced with new glass.

- The Payout: If the repair costs $700 and your deductible is $250, you pay the shop $250, and the insurance company pays the remaining $450.

Real-Life Example

Let’s look at a realistic scenario using 2026 pricing. Imagine you park your car downtown for a concert. When you return, your passenger-side window is shattered.

You call a local glass shop and find out that a new window, specialized tinting, and labor will cost $450. You check your insurance policy and see that you have a $500 comprehensive deductible.

- In this case: Because the repair cost ($450) is lower than your deductible ($500), your insurance company will not pay anything. You would be responsible for the full $450 out of pocket.

- However: If the thief had smashed two windows and the total bill was $900, you would pay your $500, and the insurance would cover the other $400.

Why is This Coverage Important?

Having comprehensive insurance is vital because car windows are becoming more expensive every year. Modern cars often have “acoustic glass” to keep the cabin quiet or built-in sensors for rain and safety alerts.

Without this coverage, a single night of bad luck could cost you over $1,000 in repairs. Furthermore, if your car is stolen and never found, comprehensive coverage is the only thing that will pay you the market value of the car so you can buy a replacement. It provides a financial safety net that ensures a crime doesn’t ruin your budget for months to come.

Do You Know What Is Does Blue Cross Insurance Cover Urgent Care?

Pros and Cons of Filing a Claim

Deciding whether to use your insurance for a broken window requires weighing the benefits against the long-term impact.

Pros:

- Saves Money on Major Damage: If multiple windows are broken or the door frame is bent, insurance can save you thousands.

- Expert Repairs: Most insurers partner with national glass companies, ensuring the work is done correctly and warrantied.

- Potential $0 Cost: Some states (like Florida or South Carolina) have laws that make glass replacement free if you have comprehensive coverage.

Cons:

- The Deductible Barrier: If your deductible is high, you might get no financial help for a single window.

- Claims History: Even if you aren’t at fault, having too many “comprehensive” claims on your record could potentially cause your rates to rise when you renew.

- Doesn’t Cover Your Stuff: Car insurance generally does not cover the personal items stolen from the car (like your gym bag or phone).

Common Mistakes People Make

Understanding the fine print can save you from a lot of frustration. Here are a few things most people get wrong:

- Assuming Car Insurance Covers Your Stolen Items: This is a huge surprise for most victims. Car insurance covers the car. If your laptop is stolen from your backseat, you actually have to file a claim through your Homeowners or Renters insurance.

- Not Checking for “Full Glass” Coverage: Many drivers don’t realize they can buy a small add-on called “Full Glass Coverage.” This often has a $0 deductible, meaning you pay nothing to fix a window, even if your main deductible is $1,000.

- Waiting Too Long to Fix It: If you leave a broken window open to the rain, water can ruin your car’s electronics or upholstery. Insurance might deny a claim for water damage if they feel you didn’t act quickly to cover the window.

- Skipping the Police Report: Without a police case number, many insurers will simply deny a theft claim because they have no official proof that a crime occurred.

Frequently Asked Questions (FAQs)

Will my insurance rates go up if I claim a broken window?

Usually, no. Comprehensive claims are considered “non-at-fault” incidents. Most insurers won’t raise your rates for a single glass claim, although a high number of claims in a short time could be seen as a risk.

What if I only have Liability insurance?

If you have the basic “Liability Only” insurance required by your state, you are not covered for theft or broken windows. You must add Comprehensive coverage to your policy to be protected from these events.

Can I use any glass shop I want?

Most of the time, yes. However, your insurance company might only pay the “market rate” for the repair. If your chosen shop is much more expensive than the national average, you might have to pay the difference.

Does insurance cover “Title Washing” or scams?

No. Theft coverage is for physical theft or vandalism of the vehicle, not for financial scams or issues with a car’s title history.

Conclusion

The bottom line is that a broken window from theft is covered by your car insurance—but only if you have comprehensive coverage. If the cost to fix the glass is higher than your deductible, your insurance company will step in to help pay the bill.

My best advice? Check your policy today. Look at your comprehensive deductible. If it is $1,000, ask your agent how much it would cost to lower it or add “Full Glass” protection. For just a few extra dollars a month, you can ensure that the next time you see broken glass, you won’t have to see a broken bank account too.