Introduction

When you wake up with a nagging earache or your child scrapes a knee that looks like it might need stitches, your first thought is usually, “Where can I go right now?” For many, the answer is an urgent care center. These clinics offer a middle ground between waiting days for a doctor’s appointment and the high-stress environment of an emergency room.

If you are one of the millions of Americans with Blue Cross Blue Shield (BCBS) insurance, you are likely wondering if your plan will cover the bill. Navigating health insurance can feel like learning a second language, but understanding your coverage is the key to getting care without a surprise financial headache. In this article, we will break down exactly how Blue Cross handles urgent care visits and what you need to know before you walk through the clinic doors.

What is Blue Cross Urgent Care Coverage?

In simple terms, Blue Cross Blue Shield (BCBS) insurance almost always includes coverage for urgent care services. Because BCBS is a federation of 34 independent companies, the specific name of your plan might be different—like Blue Shield of California or Anthem Blue Cross—but the general rules for urgent care are very similar across the board.

Urgent care coverage is designed for “non-life-threatening” medical issues that still need attention within 24 hours. Here is what this coverage generally includes:

- Common Illnesses: Treatment for the flu, strep throat, sinus infections, and fevers.

- Minor Injuries: Care for sprains, small cuts that need stitches, and minor bone fractures.

- Diagnostic Tests: Many plans cover on-site X-rays and basic lab work (like a rapid COVID or flu test).

- Preventive Care: Some centers also offer flu shots or physicals that are covered by your plan.

The most important part of this coverage is the Network. Blue Cross has one of the largest networks in the country. If you go to an “in-network” urgent care, the insurance company has a deal with that clinic to keep your costs low.

How Does Urgent Care Coverage Work?

Table of Contents

Table of Contents

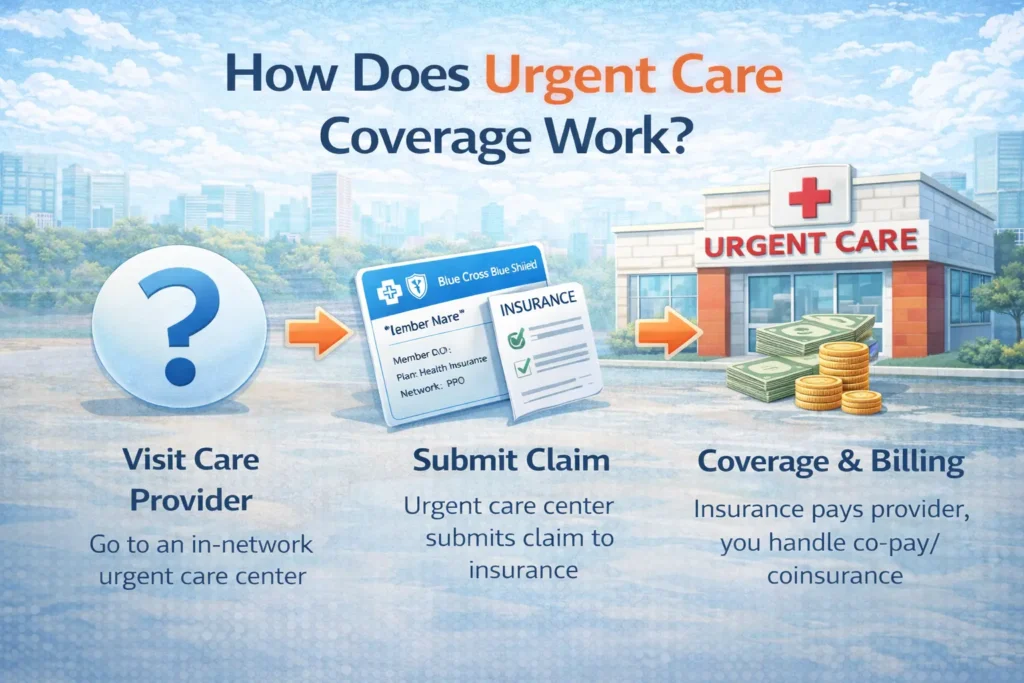

Using your Blue Cross insurance at an urgent care center follows a specific path. Understanding this flow can help you avoid long wait times and unexpected bills.

- Finding a Center: You can use the “Find Care” tool on the Blue Cross website or mobile app to locate an in-network urgent care near you.

- The Check-In: When you arrive, you show your BCBS member ID card. The front desk staff will verify that your specific plan is active and accepted at that location.

- The Copay: Most Blue Cross plans use a “copay” system for urgent care. This is a flat fee you pay at the time of your visit. For many people, this is between $30 and $75.

- The Deductible and Coinsurance: Depending on your plan, you might have to meet a deductible before the insurance pays the rest. After the deductible is met, you might pay “coinsurance,” which is a small percentage of the total bill.

- The Claim: The clinic sends a bill to Blue Cross. Blue Cross pays their portion, and if there is any remaining balance, you will receive an “Explanation of Benefits” (EOB) in the mail followed by a bill from the clinic.

Real-Life Example

Let’s look at a typical situation to see how the money works. Imagine you have a Blue Cross PPO plan. You wake up on a Saturday with a high fever and a painful sore throat. Your regular doctor’s office is closed.

You find an in-network urgent care center. Your insurance card says “Urgent Care: $50.”

- At the Clinic: You pay your $50 copay at the front desk.

- The Visit: The doctor examines you and performs a rapid strep test.

- The Cost: The total “negotiated rate” for the visit and the test is $150.

- The Payout: Since you already paid $50, Blue Cross pays the remaining $100 directly to the clinic.

If you had gone to the Emergency Room for the same sore throat, your copay might have been $350 or more, and the total bill could have reached $1,500. By choosing urgent care, you saved yourself $300 and a much longer wait.

Do You Know What Is Does a Rebuilt Title Affect Car Insurance?

Why is Urgent Care Coverage Important?

Having urgent care coverage is vital because it protects both your health and your bank account. Medical issues don’t always happen between 9:00 AM and 5:00 PM on weekdays. Urgent care centers often have evening and weekend hours, making them a “safety valve” for the healthcare system.

The benefits of using this coverage include:

- Cost Savings: It is significantly cheaper than an ER visit for minor issues.

- Time Savings: Most urgent care visits are completed in under an hour, whereas ER waits can last all night.

- Accessibility: There are nearly 10,000 urgent care centers in the U.S., meaning there is likely one very close to your home or work.

Knowing that Blue Cross covers these visits allows you to seek help early. Treating a minor infection at an urgent care on a Saturday prevents it from becoming a major emergency by Monday.

Pros and Cons of Using Urgent Care with Blue Cross

While urgent care is a great resource, it is important to know its limits.

Pros:

- Predictable Costs: Most plans have a set copay so you know what you’ll pay upfront.

- No Appointment Needed: You can walk in whenever you need help.

- Large Network: Blue Cross is accepted by the vast majority of urgent care chains like Quest or MedExpress.

- Quality Care: These centers are staffed by licensed doctors and nurse practitioners.

Cons:

- Limited Scope: They cannot handle major trauma, chest pain, or severe breathing problems.

- In-Network Rules: If you accidentally go to an out-of-network clinic, your costs could be much higher.

- Follow-up Needed: They provide “episodic” care, meaning they don’t know your full medical history like your primary doctor does.

Common Mistakes People Make

Even with good insurance, it is easy to make a mistake that leads to a higher bill. Here are the most common ones to watch out for:

- Confusing “Free-Standing ERs” with Urgent Care: This is a big one. Some buildings look like urgent care centers but are actually “emergency rooms.” They charge ER prices (sometimes $1,000+). Always look for the words “Urgent Care” specifically.

- Not Checking the Network: Just because a clinic says they “take Blue Cross” doesn’t mean they are “in-network.” Always verify through the Blue Cross app to ensure you get the lowest rate.

- Going for Life-Threatening Emergencies: If you have chest pain or a serious head injury, do not go to urgent care. They will just call an ambulance to take you to the ER, and you will end up paying for both the urgent care visit and the ER visit.

- Forgetting Your ID Card: While some clinics can look you up by your Social Security number, it is much slower and increases the chance of a billing error. Always keep a digital copy of your card on your phone.

Frequently Asked Questions (FAQs)

Does Blue Cross cover urgent care if I’m out of state? Yes. Most BCBS plans have “BlueCard” coverage, which allows you to use in-network providers across the United States. Look for the small suitcase icon on your member ID card.

Is a copay the only thing I have to pay? Usually, yes, for the visit itself. However, if the doctor performs extra procedures like an X-ray or a complex blood test, those might be subject to your deductible or coinsurance depending on your specific plan.

Do I need a referral to go to urgent care? No. Blue Cross Blue Shield plans typically do not require a referral from your primary doctor to visit an urgent care center.

What if the urgent care is closed? If it’s not an emergency, Blue Cross often provides 24/7 “Nurse Lines” or “Telehealth” services (like BlueCare Anywhere) where you can talk to a doctor over video for an even lower cost than urgent care.

Conclusion

The bottom line is that Blue Cross insurance is designed to work for you when you need quick, non-emergency care. By using an in-network urgent care center, you can get the treatment you need for a fraction of the cost of a hospital visit.

My practical advice? Take five minutes today to find the two closest in-network urgent care centers to your house using the Blue Cross website. Save their addresses in your phone now. That way, the next time you are feeling under the weather, you won’t have to stress about where to go or how much it will cost.