Introduction

Car accidents can be stressful, especially when you realize you may be at fault. Many drivers are unsure what happens next or how their car insurance will respond. Understanding how insurance works in this situation is important because it affects repair costs, medical bills, and even future premiums.

Knowing what to expect can help you stay calm and make better decisions after an accident. This article explains how car insurance works when you are at fault, what coverage applies, how claims are handled, and what financial effects you might see afterward.

What is how does car insurance work when you are at fault?

When you are “at fault,” it means you are considered responsible for causing an accident. In most cases, your car insurance helps pay for damages or injuries you caused to others, depending on your coverage.

Key types of coverage involved include:

- Liability coverage – Pays for damage to another person’s vehicle or property and their medical expenses.

- Collision coverage – Helps repair or replace your own vehicle.

- Medical payments or personal injury protection (PIP) – May cover medical costs for you or your passengers.

Fault is usually determined by insurance adjusters using accident reports, statements, and evidence.

Do you know what is How Do I Renew Car Insurance?

How does how does car insurance work when you are at fault work?

Here is the typical step-by-step process after an at-fault accident:

- Report the accident

You notify your insurance company as soon as possible. - Investigation begins

The insurer reviews police reports, photos, and driver statements to determine fault. - Coverage review

Your policy is checked to see which protections apply. - Damage payments

- Liability coverage pays for the other driver’s repairs or injuries.

- Collision coverage may pay for your own car repairs after your deductible.

- Claim settlement

Payments are issued to repair shops, medical providers, or affected drivers. - Policy update

Your premium may change at renewal depending on the claim and driving history.

The process is designed to handle financial responsibility through insurance rather than personal payment.

Do you know how to find out someone car is insured?

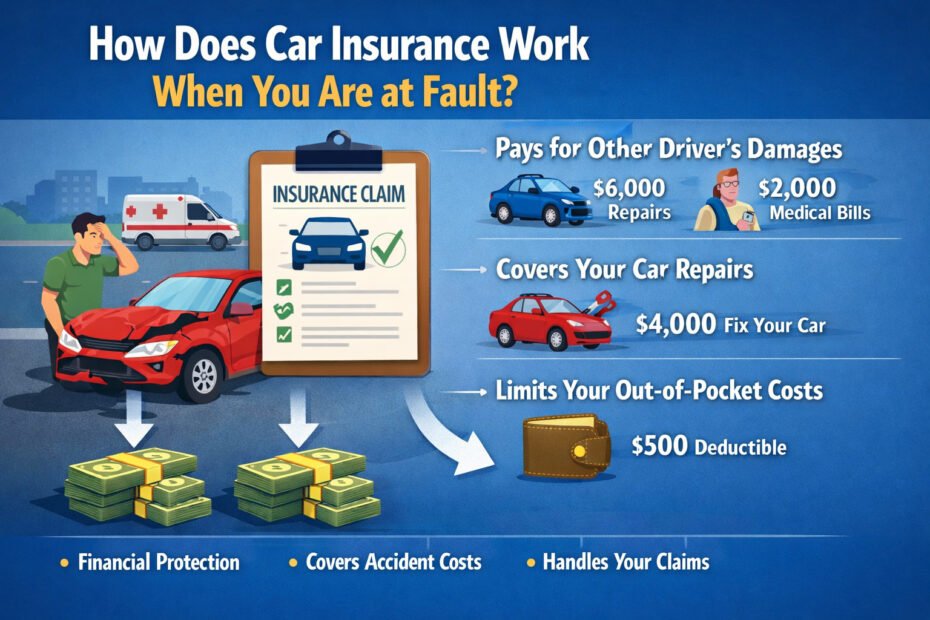

Real-life example

David accidentally runs a red light and hits another vehicle.

Damage costs include:

- Other driver’s repairs: $6,000

- Medical bills: $2,000

- David’s car repairs: $4,000

David’s policy includes liability and collision coverage with a $500 deductible.

- Liability insurance pays $8,000 for the other driver’s losses.

- Collision coverage pays $3,500 toward David’s repairs after his deductible.

David pays only the deductible instead of the full accident cost, showing how insurance protects drivers financially.

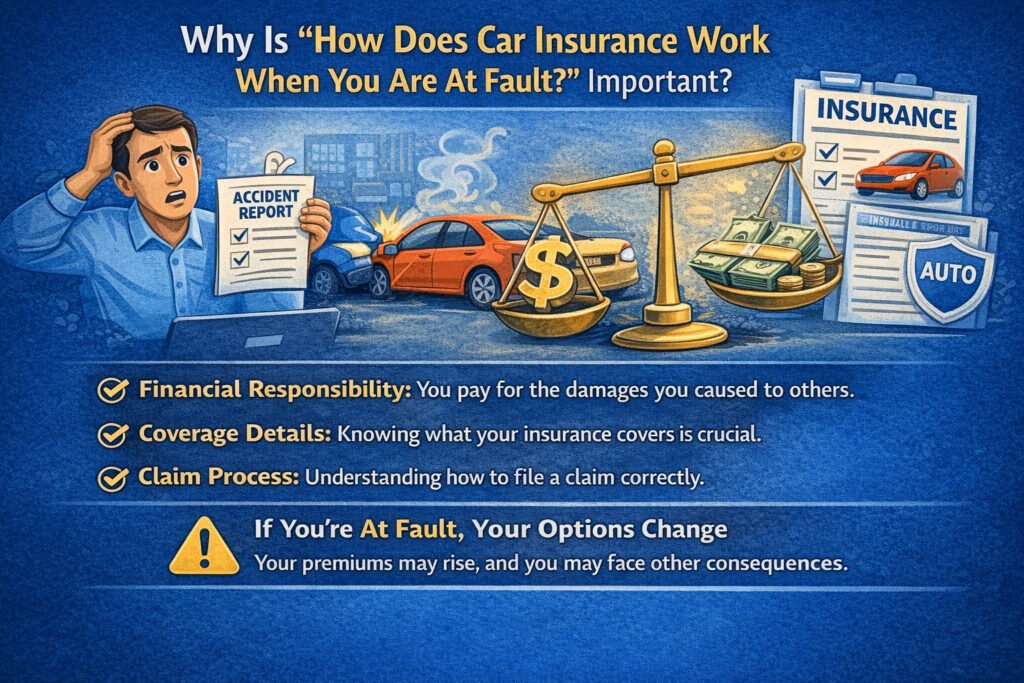

Why is how does car insurance work when you are at fault important?

Table of Contents

Table of Contents

Understanding fault coverage helps drivers prepare for unexpected situations.

Important benefits include:

- Protects savings from large accident expenses

- Helps victims receive compensation quickly

- Reduces financial stress after accidents

- Encourages responsible driving behavior

Without insurance, a driver at fault could face significant out-of-pocket costs.

Do you know How to sell car insurence?

Pros and cons of how does car insurance work when you are at fault

Pros

- Covers damages you cause to others

- Limits personal financial risk

- Provides structured claim handling

- Offers repair support and guidance

Cons

- Premiums may increase after a claim

- Deductibles must be paid

- Coverage limits may apply

- Claims process can take time

Knowing these points helps set realistic expectations.

Common mistakes people make

Drivers often misunderstand what happens after being at fault.

- Assuming insurance covers everything

Deductibles and coverage limits still apply. - Not reporting the accident quickly

Delays can complicate claims. - Admitting fault immediately at the scene

Fault decisions are made after investigation. - Not understanding coverage types

Liability and collision serve different purposes. - Skipping documentation

Photos and details help support claims.

Staying calm and organized helps avoid unnecessary problems.

Frequently asked questions (FAQs)

Will my insurance always go up if I am at fault?

Not always, but premiums may increase depending on the insurer and accident history.

Does liability coverage fix my car?

No. Liability covers damage to others. Collision coverage handles your vehicle.

What if both drivers share fault?

Some states reduce payments based on each driver’s percentage of responsibility.

Do I still pay a deductible if I am at fault?

Yes, usually for repairs to your own vehicle under collision coverage.

Conclusion

Being at fault in an accident can feel overwhelming, but car insurance is designed to manage the financial impact. Liability coverage helps pay for damages you cause to others, while optional coverages can protect your own vehicle and medical expenses.