Dealing with an insurance claim denial or an unexpectedly low settlement can be frustrating, confusing, and stressful. Whether the claim involves homeowners insurance, auto insurance, or health insurance, many policyholders feel stuck after receiving a rejection letter. Fortunately, a denial does not always mean the end of the road. Understanding how to write an appeal letter to an insurance company can help you challenge the decision and potentially receive the coverage or payment you deserve.

An insurance appeal letter is more than just a complaint—it is a formal, structured request asking the insurer to reconsider its decision based on policy language, facts, and supporting evidence. When written correctly, an appeal letter can be a powerful tool.

This comprehensive guide explains everything you need to know about writing an effective insurance appeal letter. It walks you through the appeal process step by step, explains what insurance companies look for, highlights common mistakes to avoid, and provides a detailed appeal letter example you can customize for your situation.

Table of Contents

Table of Contents

What Is an Insurance Appeal Letter?

An insurance appeal letter is a written request submitted by a policyholder asking an insurance company to review and reconsider a claim decision. This could include:

- A complete denial of coverage

- Partial approval with limited payment

- Excluded damages you believe should be covered

- A reduced settlement amount

The purpose of the appeal letter is to clearly explain why the insurer’s decision is incorrect, using policy terms, factual evidence, and documentation.

Insurance appeal letters are commonly used for:

- Homeowners insurance claims

- Auto insurance claims

- Health insurance claims

- Property damage claims

- Disability and life insurance claims

Do you know How Long Does a Homeowners Insurance Claim Take?

Why Insurance Claims Get Denied or Underpaid

Before writing an appeal letter, it helps to understand why insurance companies deny or reduce claims in the first place. Common reasons include:

- Policy exclusions

- Missed deadlines

- Insufficient documentation

- Disputes over cause of damage

- Coverage limits or deductibles

- Errors in adjuster reports

- Incomplete claim information

Not all denials are justified. In many cases, claims are denied because of missing details or misunderstandings—not because coverage doesn’t exist.

When Should You Write an Appeal Letter to an Insurance Company?

You should write an appeal letter if:

- Your claim was denied and you believe coverage applies

- Your settlement amount does not reflect the true cost of damage

- The insurer misinterpreted policy language

- Important evidence was overlooked

- The adjuster’s estimate is inaccurate

Most insurance policies include a formal appeals process, and many state insurance laws require insurers to review appeals within a reasonable timeframe.

Understanding Insurance Appeal Deadlines

One of the most important aspects of the appeal process is timing. Insurance companies usually impose deadlines for filing an appeal, which may range from:

- 30 days

- 60 days

- 90 days

- Up to 180 days

Missing the appeal deadline can result in an automatic denial, regardless of how strong your case is. Always check your denial letter and policy documents for appeal timelines.

How to Write an Appeal Letter to an Insurance Company (Step-by-Step)

Writing an effective appeal letter requires preparation, clarity, and organization. Below is a detailed breakdown of each step.

Step 1: Review the Denial Letter Carefully

Your denial or settlement letter explains why the insurance company made its decision. Read it closely and look for:

- The stated reason for denial or reduced payment

- References to specific policy sections

- Deadlines for filing an appeal

- Instructions for submitting additional information

Understanding the insurer’s reasoning allows you to address it directly in your appeal.

Step 2: Read Your Insurance Policy Thoroughly

Your policy is the foundation of your appeal. Look for:

- Covered perils

- Definitions of damage or loss

- Exclusions and limitations

- Endorsements or riders

- Duties after loss

Highlight sections that support your claim. Your appeal should reference specific policy language, not assumptions.

Do you know What Does AOB Stand for in Insurance?

Step 3: Gather Supporting Documentation

Documentation is often the deciding factor in an insurance appeal. Include copies of relevant materials such as:

- The original denial letter

- Photos or videos of damage

- Repair estimates or contractor invoices

- Inspection reports

- Adjuster reports

- Police or fire reports

- Medical records or professional opinions

- Receipts for temporary repairs or expenses

Organize your documents and reference them clearly in your letter.

Step 4: Keep the Tone Professional and Objective

While it’s normal to feel upset, emotional language can weaken your appeal. Insurance appeals are evaluated based on facts, not frustration.

A strong appeal letter should be:

- Professional

- Clear and factual

- Respectful

- Well-structured

Avoid accusations, threats, or hostile language.

Step 5: Structure Your Appeal Letter Properly

A well-written appeal letter should include the following sections:

- Header with your contact information

- Insurance company details

- Policy and claim information

- Clear statement of appeal

- Explanation of why the decision is incorrect

- Supporting evidence references

- Specific request for reconsideration

- Professional closing

Sample Insurance Appeal Letter (Customizable Example)

Below is a general example that can be adapted for homeowners, auto, or health insurance claims.

[Your Full Name]

[Your Address]

[City, State, ZIP Code]

[Phone Number]

[Email Address]

[Date]

[Insurance Company Name]

[Claims Department Address]

Re: Insurance Claim Appeal

Policy Number: [Policy Number]

Claim Number: [Claim Number]

Dear Claims Reviewer,

I am writing to formally appeal the decision dated [date] regarding the above-referenced insurance claim. After carefully reviewing the denial letter and my insurance policy, I believe the decision does not accurately reflect the coverage provided under my policy.

The denial states that the damage was excluded due to [reason given]. However, Section [X] of my policy indicates that damage caused by [specific cause] is a covered peril. The loss occurred on [date], and the damage directly resulted from this event.

Enclosed with this letter are supporting documents, including photographs of the damage, repair estimates, and the adjuster’s report. These materials demonstrate that the loss falls within the scope of coverage outlined in my policy.

Based on this information, I respectfully request that my claim be reviewed again and adjusted accordingly. Please let me know if any additional documentation is required to complete this review.

Thank you for your time and consideration.

Sincerely,

[Your Name]

Mastering the Insurance Appeal Process: A Practical Guide

Receiving an insurance claim denial is stressful, but it is often just the first step in a long negotiation. A strategic, well-documented appeal letter can turn a “no” into a paid claim. Here is how to navigate the process effectively.

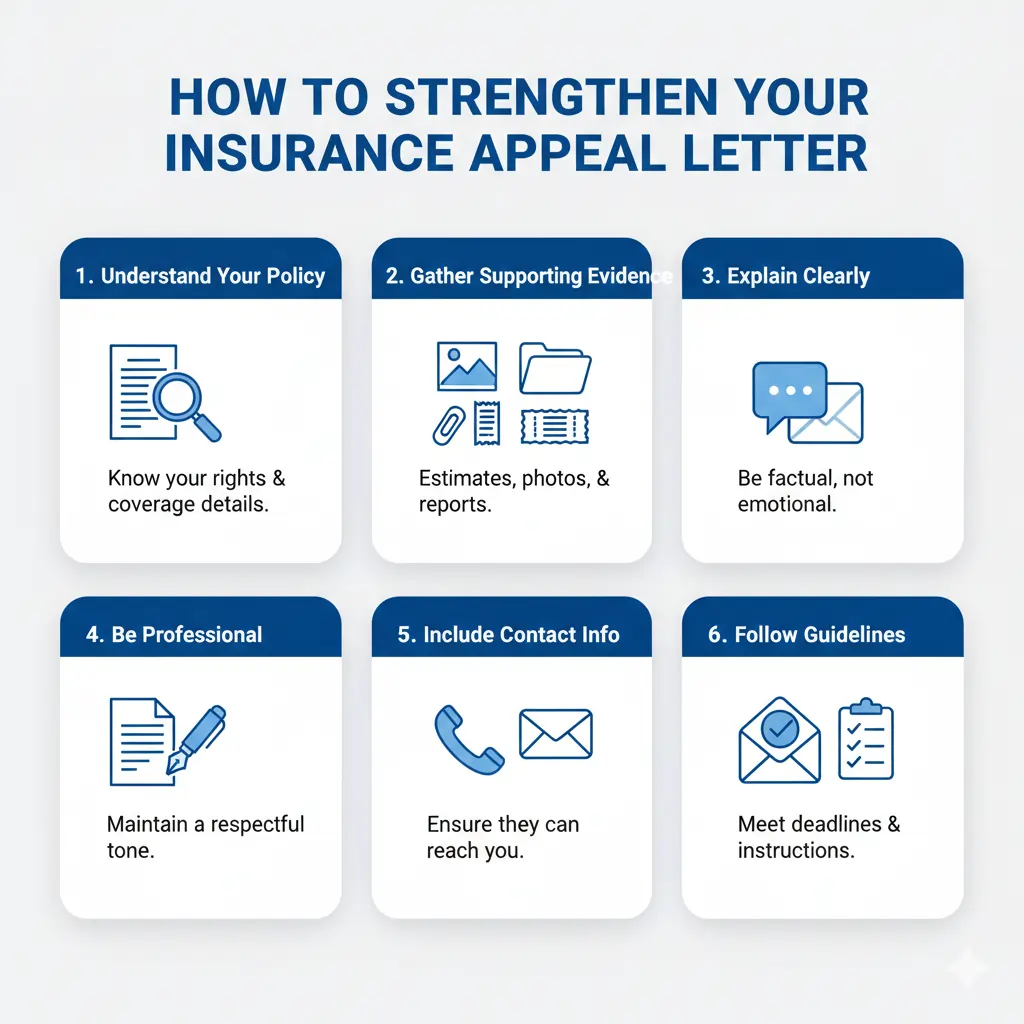

How to Strengthen Your Insurance Appeal Letter

An effective appeal relies on facts and evidence, not emotion. To maximize your chances of success, you must build an undeniable case.

Speak Their Language

Don’t just claim you have coverage; prove it. Reference policy language directly. Quote the specific sections or definitions in your policy contract that support your claim. This demonstrates you understand your coverage and forces the insurer to address the actual contract terms.

The Power of Independent Evidence

Insurance adjusters sometimes undervalue damages. Include independent estimates from third-party contractors, mechanics, or professionals. An itemized quote from an unbiased expert carries far more weight than a simple disagreement with the insurer’s valuation.

Stay Organized

Organization is crucial. Keep copies of everything—every email, letter, and document sent or received. In your appeal package, label your documents clearly (e.g., “Exhibit A: Contractor Estimate”) so the reviewer can easily follow your argument.

Common Mistakes to Avoid

Many valid appeals fail due to preventable errors. Avoid these pitfalls to keep your claim alive.

| Mistake | Why It Hurts Your Case |

| Missing Deadlines | This often leads to an automatic denial, regardless of the claim’s merit. |

| Emotional Writing | Aggressive language damages your credibility. Stick strictly to the facts. |

| Incomplete Docs | Failing to provide requested proof gives them an easy reason to deny again. |

What Happens After Submission?

Once your appeal is submitted via certified mail or portal, the waiting game begins. The insurance company typically follows these steps:

- A new reviewer or senior adjuster is assigned to the file.

- They review your new evidence against the policy.

- They may request further information or a re-inspection.

- A final written decision is issued (this can take weeks or months).

What If Your Appeal Is Denied Again?

A second denial is disheartening, but not the end of the road. You still have options:

- Request an external, independent review (common in health insurance).

- File a formal complaint with your state’s Department of Insurance.

- Consult a Public Adjuster or insurance attorney.

Special Considerations for Homeowners

Homeowners insurance appeals often involve complex technical disputes. Success frequently depends on expert opinions regarding:

Valuation Disputes: Arguing for Replacement Cost versus the lower Actual Cash Value.

Roof Damage: Distinguishing storm damage from normal wear and tear.

Water Damage: Pinpointing the exact source and timing of the leak.

FAQs: How to Write an Appeal Letter to an Insurance Compan

How long do I have to appeal an insurance claim?

Deadlines vary by policy and state, but typically range from 30 to 180 days.

Can I appeal an insurance claim more than once?

Some insurers allow multiple levels of appeal, while others limit you to one formal appeal.

Should I hire a professional to help with my appeal?

For large or complex claims, a public adjuster or attorney may be helpful.

Does writing an appeal letter guarantee approval?

No, but a well-written appeal significantly increases your chances.

Can I email my insurance appeal letter?

Some insurers allow email appeals, but many require mailed or uploaded documentation. Always confirm submission requirements.

Final Thoughts: How to Write an Appeal Letter to an Insurance Company

Learning how to write an appeal letter to an insurance company gives policyholders a powerful way to challenge unfair or incorrect claim decisions. A strong appeal focuses on facts, policy language, and documentation—not emotion.

By staying organized, meeting deadlines, and presenting a clear argument, you can improve your chances of receiving the coverage or compensation you are entitled to under your policy.

Insurance appeals require patience, but they are often worth the effort—especially when significant money or repairs are involved.