Filing a homeowners insurance claim can feel overwhelming—especially when you’re dealing with property damage, repairs, and uncertainty about when you’ll receive your payout. One of the most common questions homeowners ask is: how long does a homeowners insurance claim take?

The answer isn’t always straightforward. While some claims are resolved in just a few days, others can take weeks or even months depending on the type of damage, the complexity of the claim, and how quickly information is provided.

In this comprehensive guide, we’ll break down the entire homeowners insurance claim timeline, explain what factors affect processing time, and share practical tips to help speed up your claim. This article is tailored specifically for U.S. homeowners and follows best practices for accuracy, clarity, and SEO—without spammy tactics.

Table of Contents

Table of Contents

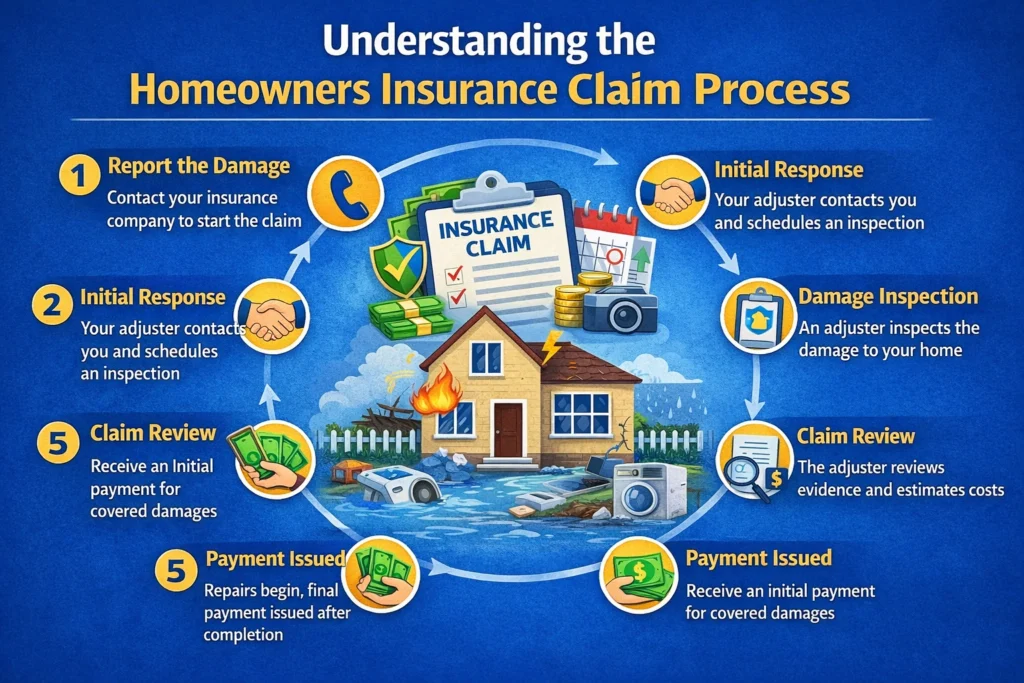

Understanding the Homeowners Insurance Claim Process

Before answering how long a homeowners insurance claim takes, it’s important to understand the steps involved. Most insurance companies follow a similar process:

- Damage occurs

- Claim is reported

- Claim is reviewed

- Adjuster inspection

- Claim decision

- Payment or repair settlement

Each stage can influence the overall timeline.

Average Homeowners Insurance Claim Timeline

How Long Does a Homeowners Insurance Claim Take on Average?

For most standard claims in the U.S., the timeline looks like this:

- Simple claims: 7–14 days

- Moderate claims: 2–4 weeks

- Complex or disputed claims: 1–6 months (or longer)

The actual length depends on the type of claim and how smoothly the process goes.

Step-by-Step Breakdown of the Claim Timeline

1. Filing the Claim (Same Day to 48 Hours)

Once damage occurs, you should contact your insurance company as soon as possible. Most insurers allow you to file a claim:

- Online

- Through a mobile app

- By phone

- Through your insurance agent

Tip: Filing your claim promptly helps avoid delays and strengthens your case.

⏱ Time required: Same day to 2 days

Do you What Is Loss of Use Coverage?

2. Claim Review and Initial Processing (1–5 Days)

After submission, the insurer assigns a claim number and reviews your policy to confirm coverage. They may request:

- Photos or videos of damage

- A description of what happened

- Police or fire reports (if applicable)

⏱ Time required: 1–5 business days

3. Adjuster Assignment and Inspection (3–10 Days)

An insurance adjuster is usually assigned to inspect the damage. This inspection can be:

- In-person

- Virtual (photos/video calls)

- Hybrid

For minor claims, inspections may be skipped entirely.

⏱ Time required: 3–10 days (may be longer after major disasters)

4. Damage Evaluation and Estimate (5–15 Days)

The adjuster evaluates repair or replacement costs and prepares an estimate. This includes:

- Structural damage

- Personal property losses

- Additional living expenses (ALE), if applicable

⏱ Time required: 5–15 days

5. Claim Decision and Approval (7–30 Days)

Once evaluation is complete, the insurance company decides whether to:

- Approve the claim

- Partially approve it

- Deny it

In many U.S. states, insurers are legally required to respond within a specific timeframe.

⏱ Time required: 1–4 weeks

6. Payment Issuance (5–10 Days After Approval)

If approved, payment is issued by:

- Check

- Direct deposit

- Joint payment to you and your mortgage lender

Large claims may involve multiple payments.

⏱ Time required: 5–10 business days

Total Time: How Long Does a Homeowners Insurance Claim Take?

Putting it all together:

- Minor claim: 1–2 weeks

- Typical claim: 2–4 weeks

- Major claim: 1–3+ months

Factors That Affect How Long a Homeowners Insurance Claim Takes

1. Type of Claim

Some claims are processed faster than others.

| Claim Type | Average Time |

|---|---|

| Water damage | 1–3 weeks |

| Roof damage | 2–4 weeks |

| Fire damage | 1–6 months |

| Theft | 2–4 weeks |

| Natural disasters | 2–6+ months |

2. Severity of Damage

The more extensive the damage, the longer the investigation and approval process.

3. Documentation Quality

Missing or unclear documentation is one of the biggest causes of delays.

4. Insurance Company Workload

After hurricanes, wildfires, or floods, insurers may handle thousands of claims at once.

5. Disputes or Negotiations

If you disagree with the adjuster’s estimate, negotiations or additional inspections may extend the timeline.

6. State Regulations

Each U.S. state has different insurance laws that impact claim deadlines and response times.

How to Speed Up a Homeowners Insurance Claim

Filing a homeowners insurance claim can feel overwhelming, especially when you are already dealing with property damage and stress. While you cannot control every part of the insurance process, there are several smart steps you can take to avoid unnecessary delays and move your claim forward faster.

If you want to receive your settlement quickly and reduce back-and-forth communication, preparation and organization are key. Below is a detailed guide to help U.S. homeowners speed up a homeowners insurance claim efficiently and responsibly.

1. File Your Claim Immediately After Damage Occurs

One of the biggest mistakes homeowners make is waiting too long to report damage. Insurance companies expect claims to be filed “promptly” after a covered event occurs.

Why filing quickly matters:

- It prevents questions about when the damage happened

- It reduces suspicion about secondary damage

- It helps secure faster adjuster scheduling

- It protects your rights under your policy

Even if you are unsure whether the damage is fully covered, it is better to notify your insurer right away. Most companies allow you to file:

- Online through a claims portal

- Through a mobile app

- By calling a 24/7 claims hotline

Delaying the claim could lead to complications, especially if additional damage occurs.

2. Document Everything in Detail

Thorough documentation is one of the most powerful tools for speeding up a homeowners insurance claim.

Before cleaning or making temporary repairs, take:

- Clear, high-resolution photos

- Wide-angle images of affected areas

- Close-up photos of damaged items

- Video walkthroughs with narration

If possible, capture:

- Serial numbers of appliances

- Brand names

- Model numbers

- Receipts for valuable items

Pro Tip:

Create a simple damage inventory list that includes:

- Item name

- Approximate purchase date

- Estimated replacement cost

- Current condition

The more evidence you provide upfront, the fewer follow-up requests your insurer will need to make.

3. Prevent Further Damage (But Don’t Over-Repair)

Most homeowners insurance policies require you to take reasonable steps to prevent additional damage.

For example:

- Cover broken windows with plastic

- Place tarps over roof damage

- Shut off water if pipes burst

- Remove standing water safely

However, avoid making permanent repairs until the adjuster inspects the property (unless emergency repairs are necessary).

Keep all receipts for:

- Temporary repair materials

- Emergency contractor services

- Hotel stays (if applicable)

Insurance companies typically reimburse reasonable emergency expenses under loss of use or mitigation coverage.

4. Be Responsive and Organized

Communication delays are one of the most common reasons homeowners insurance claims slow down.

To keep things moving:

- Return calls and emails promptly

- Provide requested documents quickly

- Keep a claim communication log

- Save all emails and letters

Maintain a simple folder (digital or physical) with:

- Claim number

- Adjuster contact information

- Repair estimates

- Photos

- Policy documents

Being organized shows the insurance company that you are proactive and serious about resolving the claim.

5. Get Independent Repair Estimates

While the insurance company may send its own adjuster or contractor, it is wise to get independent repair estimates from licensed local contractors.

Why this helps:

- Prevents undervaluation of damage

- Speeds up negotiation

- Provides realistic market pricing

- Strengthens your position

Make sure contractors provide:

- Written, itemized estimates

- Labor and material breakdowns

- Clear scope of work

Providing estimates early can reduce disputes and prevent extended review periods.

6. Understand Your Coverage Before Problems Arise

Many claim delays happen because homeowners misunderstand their coverage.

Before or during your claim, review:

- Your deductible amount

- Coverage limits

- Exclusions

- Replacement cost vs. actual cash value

- Loss of use coverage

Knowing what your policy actually covers helps you:

- Set realistic expectations

- Avoid filing unnecessary disputes

- Respond confidently to adjuster decisions

If something is unclear, ask your insurance representative to explain it in writing

7. Prepare for the Adjuster Visit

The insurance adjuster plays a critical role in determining your payout. Preparing properly for their inspection can significantly speed up the claim process.

Before the visit:

- Have your damage list ready

- Provide copies of receipts

- Share repair estimates

- Point out all damaged areas

Walk through the property with the adjuster if possible. This ensures nothing is overlooked.

Clear communication during inspection reduces the chances of delays or supplemental claims later.

8. Follow Up Professionally (Without Being Aggressive)

If your claim seems stalled, follow up respectfully.

You can:

- Send a polite email requesting an update

- Ask if additional documents are needed

- Confirm estimated decision timelines

Most states have regulations requiring insurers to respond within a reasonable time frame. However, courteous follow-up is usually more effective than confrontation.

9. Avoid Common Claim Delays

Here are mistakes that often slow down homeowners insurance claims:

- Waiting too long to file

- Incomplete documentation

- Ignoring adjuster calls

- Failing to provide receipts

- Overstating damage

- Hiring unlicensed contractors

Accuracy and honesty are critical. Misrepresenting damage can delay your claim or even result in denial.

10. Consider Hiring a Public Adjuster (For Large Claims)

If your claim involves significant property damage or a large payout, you may consider hiring a licensed public adjuster.

A public adjuster:

- Works on your behalf (not the insurance company)

- Reviews your policy

- Assesses damage independently

- Negotiates settlement terms

They typically charge a percentage of the settlement amount.

This option may help if:

- Your claim is denied

- The settlement offer is too low

- Damage is complex

For smaller claims, this step may not be necessary.

11. Keep Track of State Claim Deadlines

Each state has regulations governing insurance claim timelines. Many states require insurers to:

- Acknowledge claims within a specific period

- Begin investigation promptly

- Issue payment within a defined timeframe after approval

Understanding your state’s rules can give you peace of mind and protect your rights.

12. Stay Calm and Patient

While everyone wants a fast settlement, complex claims naturally take longer. Severe weather events, regional disasters, or high claim volumes can extend timelines.

Staying organized and cooperative helps prevent unnecessary stress and keeps the process moving efficiently.

Do you know What Does AOB Stand for in Insurance?

Common Reasons for Homeowners Insurance Claim Delays

- Incomplete paperwork

- Coverage disputes

- Multiple inspections

- Contractor shortages

- Mortgage lender involvement

- Fraud investigations

What If Your Homeowners Insurance Claim Is Taking Too Long?

If your claim seems unreasonably delayed:

- Contact your adjuster for a status update

- Request a supervisor review

- File a complaint with your state’s Department of Insurance

- Seek legal or professional advice

FAQs: How Long Does a Homeowners Insurance Claim Take?

How long does a homeowners insurance claim take for water damage?

Most water damage claims take 1–3 weeks, unless mold or structural issues are involved.

How long does a homeowners insurance claim take after a fire?

Fire claims are complex and typically take 1–6 months, depending on severity.

Can an insurance company delay a homeowners claim?

Insurance companies must follow state regulations. Unreasonable delays may violate insurance laws.

How long does it take to get paid after a claim is approved?

Payment is usually issued within 5–10 business days after approval.

Why is my homeowners insurance claim under investigation?

Claims may be investigated for coverage verification, damage cause, or fraud prevention.

Can I start repairs before my claim is approved?

Yes, you can make temporary repairs to prevent further damage, but avoid permanent repairs without approval.

What is the fastest homeowners insurance claim?

Minor theft or small water damage claims can be resolved in under a week.

Does filing a homeowners insurance claim increase premiums?

It can, especially for multiple claims or high-value losses.

Final Thoughts: How Long Does a Homeowners Insurance Claim Take?

So, how long does a homeowners insurance claim take?

For most U.S. homeowners, the process takes two to four weeks, but larger or more complex claims can extend much longer.

The key to a faster, smoother claim is prompt filing, strong documentation, and clear communication with your insurance company. Understanding the process empowers you to avoid unnecessary delays and ensures you receive the compensation you deserve.

If you’re facing a complicated or delayed claim, don’t hesitate to seek professional help or escalate the issue. Your home is one of your most valuable assets—and protecting it matters.