Introduction

Water damage from appliances is a common worry for homeowners in the United States. A leaking washing machine, broken dishwasher, or faulty water heater can cause serious damage in a short time. Many people assume their homeowners insurance will cover all water-related problems, but that is not always true. Coverage depends on how the damage happened and what your policy includes. This article explains when homeowners insurance does and does not cover water damage from appliances, how coverage works, common mistakes to avoid, and what you should know before a problem happens.

Table of Contents

What is homeowners insurance coverage for water damage from appliances?

Homeowners insurance is designed to protect your home from sudden and unexpected damage. When it comes to water damage from appliances, coverage usually depends on the cause.

In simple terms, insurance may cover:

- Sudden leaks or bursts from appliances.

- Accidental water damage that happens quickly.

It usually does not cover:

- Slow leaks that happen over time

- Damage caused by poor maintenance.

- Flooding from outside the home.

The key idea is whether the damage was sudden and accidental.

What Counts as Water Damage Under a Standard Home Insurance Policy?

Most standard homeowners insurance policies (HO-3 policies) cover water damage that is sudden and accidental. This means the damage had to happen quickly and without warning — not as a result of a long-term problem you could have fixed.

When an appliance fails out of nowhere and water spreads across your floors, there’s a good chance your policy will help cover the costs. But when a slow, hidden leak has been dripping inside a cabinet for weeks or months, insurers typically consider that a maintenance issue — and that usually means a denied claim.

The distinction seems simple, but in practice it causes a lot of confusion for homeowners. Understanding exactly where that line is drawn can save you thousands of dollars.

Do you know what is mean by ho-3 in home Insurence?

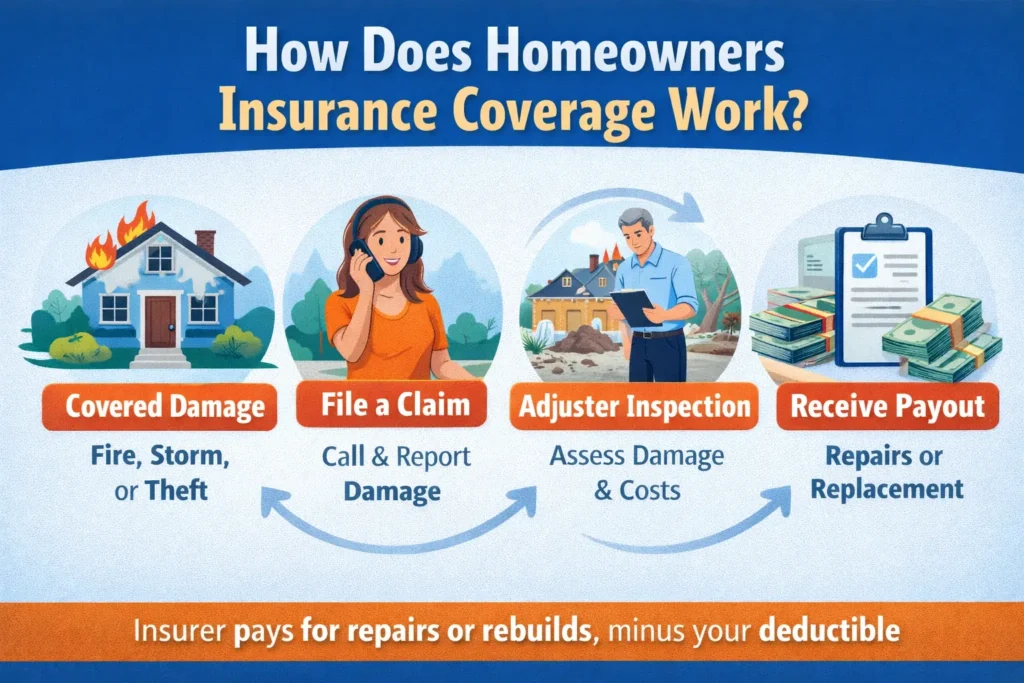

How does homeowners insurance coverage work?

Here is a simple step-by-step explanation:

- An appliance fails suddenly

For example, a washing machine hose bursts without warning. - Water causes damage

Water damages floors, walls, or nearby furniture. - You file a claim

You contact your insurance company and report the damage. - The insurer investigates

They check the cause of the leak and your policy details. - Coverage decision is made

If the damage meets policy rules, repairs may be covered minus your deductible.

Most standard policies cover water damage only if it is sudden, accidental, and comes from inside the home.

Do you know what is mean by Dewlling coverage in home insurence?

Which Appliances Are Most Likely to Cause Water Damage?

Before diving into coverage details, it helps to know which appliances are responsible for the most water damage claims in American homes.

Washing Machines are among the top culprits. Supply hoses — especially rubber ones — can crack, loosen, or burst over time. A single burst hose can release hundreds of gallons of water before you even notice. Most insurance experts recommend replacing rubber washing machine hoses with braided steel ones every five years.

Dishwashers can leak from the door seal, the drain hose, or the water inlet valve. A dishwasher running while you sleep can silently flood your kitchen floor and seep under cabinets before morning.

Water Heaters hold anywhere from 40 to 80 gallons of water. When the tank corrodes or the pressure relief valve fails, the resulting flood can damage floors, walls, and even the structural framing of your home.

Refrigerators with Ice Makers are a frequently overlooked source of leaks. The thin plastic supply line running to the ice maker can crack, especially in older models, leading to slow leaks behind or beneath the appliance.

HVAC Systems and Dehumidifiers can overflow their drip pans or have blocked condensate drain lines, causing water to pool and eventually damage ceilings, walls, and flooring.

Coverage is most likely when the damage meets three basic conditions:

1. The damage was sudden. There was no gradual buildup — the appliance failed quickly and water spread rapidly as a result.

2. The damage was accidental. You didn’t cause it on purpose, and it wasn’t the result of ignoring a known problem.

3. The source was internal. The water came from inside your home — not from a storm, flood, or sewer backup outside.

When these three conditions are met, your policy’s dwelling coverage typically pays to repair structural damage like flooring, drywall, cabinets, and ceilings. Your personal property coverage may also kick in to replace damaged furniture, rugs, and belongings.

Do you know how much home insurence cost in usa?

Real-life example

ImSay your dishwasher supply line suddenly fails on a Tuesday afternoon. Water floods your kitchen and soaks into the hardwood floor and the drywall beneath your cabinets. Here’s a rough breakdown of what that might look like financially:

- Hardwood floor replacement: $3,500

- Cabinet base repair: $1,800

- Drywall and paint: $900

- Total repair cost: $6,200

- Your deductible: $1,000

- Insurance pays: $5,200

That’s a significant amount of money that stays in your pocket — as long as you filed the claim correctly and the cause was genuinely sudden.

When Does Homeowners Insurance NOT Cover Appliance Water Damage?

This is where many homeowners run into trouble. Insurance companies have adjusters trained to identify signs that damage happened gradually over time — and they will look closely before approving any claim.

Slow Leaks and Gradual Damage are almost always excluded. If a washing machine hose has been dripping for months and caused mold or rotted subfloor, your insurer will likely deny the claim. The reasoning is that you had an opportunity to notice and fix the problem before it became serious.

Poor Maintenance is another common reason for denial. If your water heater was 20 years old and clearly overdue for replacement, an insurer may argue that the failure was foreseeable and therefore not covered.

Flooding From External Sources is excluded from standard policies entirely. If heavy rain causes water to back up into your home through drains or flood through the foundation, that’s a flood event — and you’d need a separate flood insurance policy through the NFIP or a private insurer.

Sewer and Drain Backup is also typically excluded unless you’ve added a specific endorsement (also called a rider) to your policy.

Mold Resulting from a Covered Leak can be tricky. Some policies cover mold remediation if it results from a covered water event, while others exclude it entirely. Always check your policy language carefully.

Do you know How dose deductibe work in home insurence?

How Do Insurance Companies Investigate Water Damage Claims?

When you file a water damage claim, the insurer sends an adjuster to assess the damage. They’re not just looking at what broke — they’re looking for clues about when and why it broke.

An adjuster will examine:

- Water stains and discoloration — older stains suggest a long-term leak

- Mold growth — mold typically takes 24–48 hours to begin forming, so heavy mold suggests prolonged moisture

- Warping or rot — structural damage that took time to develop

- The condition of the appliance — signs of rust, corrosion, or obvious wear and tear

- Maintenance records — in some cases, they may ask if the appliance was recently serviced

If there’s clear evidence of gradual damage, expect your claim to be denied or significantly reduced.

What Is Loss of Use Coverage and How Does It Apply?

If water damage from an appliance makes your home temporarily uninhabitable — say, your kitchen is being torn out and rebuilt — your homeowners policy’s loss of use coverage (also called Coverage D) may help pay for hotel stays and restaurant meals while repairs are underway.

This coverage is typically a percentage of your dwelling coverage limit, often around 20 to 30 percent. Keep all receipts for food, lodging, and other reasonable living expenses. Your insurer will want documentation before reimbursing these costs.

Why is this coverage important?

Water damage repairs can be expensive. Floors, drywall, cabinets, and electrical systems are costly to fix.

This type of coverage helps:

- Protect your savings from large repair bills

- Reduce stress after an unexpected accident

- Keep your home safe and livable

- Without proper coverage, homeowners may have to pay thousands of dollars out of pocket.

How to File a Water Damage Claim the Right Way

Filing your claim correctly from the start can make a significant difference in how it’s resolved.

Act immediately. As soon as you discover water damage, stop the source if possible (turn off the water supply valve) and document everything before cleanup begins.

Take photos and video. Photograph the damaged appliance, the water spread, and all affected surfaces. This evidence is critical. Capture the extent of the damage from multiple angles.

Call your insurer quickly. Most policies require you to report claims “promptly.” Waiting too long can give the insurer grounds to argue the damage worsened due to delay.

Keep damaged materials. Don’t throw away sections of flooring, drywall, or the failed appliance until the adjuster has seen them. Physical evidence supports your claim.

Get contractor estimates in writing. Having two or three repair estimates helps you understand the true cost and gives you leverage if the insurer’s payout seems low.

Review the settlement offer carefully. You have the right to dispute a claim decision. If you believe you’ve been underpaid or wrongly denied, you can request a re-inspection, hire a public adjuster, or consult an attorney who specializes in insurance claims.

How to Reduce Your Risk of Appliance Water Damage

Prevention is always less expensive than a claim — and it keeps your insurance record clean, which helps avoid premium increases.

Inspect hoses regularly. Check washing machine, dishwasher, and refrigerator supply lines every six months for cracks, bulges, or moisture at the connections.

Replace rubber hoses. Upgrade to reinforced braided stainless steel hoses, which are far more durable.

Install water leak detectors. Inexpensive smart sensors placed near appliances can alert you on your phone the moment moisture is detected. Some systems can automatically shut off the water supply.

Know where your main water shutoff is. In an emergency, being able to cut the water supply in seconds can dramatically reduce the damage.

Service your water heater annually. Flushing sediment and checking the anode rod each year extends the life of your tank and reduces the chance of failure.

Don’t run appliances when you’re not home. Running a dishwasher or washing machine while you’re out — or asleep — means a leak can go undetected for hours.

Do you how to write an appeal letter to insurence company ?

Pros and cons of homeowners insurance water damage coverage

Pros:

- Covers sudden and accidental appliance leaks

- Helps pay for costly repairs

- Provides peace of mind

Cons:

- Does not cover slow or ignored leaks

- Flood damage is usually excluded

- Deductibles still apply

- Understanding these pros and cons helps set realistic expectations.

- Common mistakes people make

Many homeowners misunderstand water damage coverage. Common mistakes include:

- Assuming all water damage is covered

- Ignoring small leaks until they get worse

- Not reading policy exclusions carefully

- Confusing flood damage with appliance leaks

- Forgetting to maintain appliances regularly

Avoiding these mistakes can help prevent claim denials.

Frequently asked questions (FAQs)

Does homeowners insurance cover water damage from a washing machine?

Yes, if the damage is sudden and accidental, such as a burst hose.

Are slow leaks from appliances covered?

Usually no. Insurance companies often deny claims for damage caused over time.

Is water heater damage covered by insurance?

Damage caused by a sudden water heater failure may be covered, but the cost to replace the old unit often is not.

Do I need extra coverage for water damage?

Some homeowners choose add-ons for sewer backup or extra water protection, depending on risk.

Conclusion:

Homeowners insurance can cover water damage from appliances, but only in certain situations. Sudden and accidental leaks are usually covered, while slow leaks, poor maintenance, and flooding are not. The best approach is to understand your policy, maintain appliances, and act quickly when leaks happen. Knowing these basics can help you avoid surprises and protect your home and budget when water damage occurs.